Macro Strategy

View:

May 17, 2024

May 16, 2024

France and Japan: Debt Fuelled Growth Problem

May 16, 2024 10:30 AM UTC

Most of the surge in debt/GDP in Japan and 40% in France is due to higher government debt and this should not be a binding constraint provided that large scale QT is avoided – we see the ECB slowing QT in 2025 and are skeptical about BOJ QT in the next few years. The adverse impact of higher deb

May 15, 2024

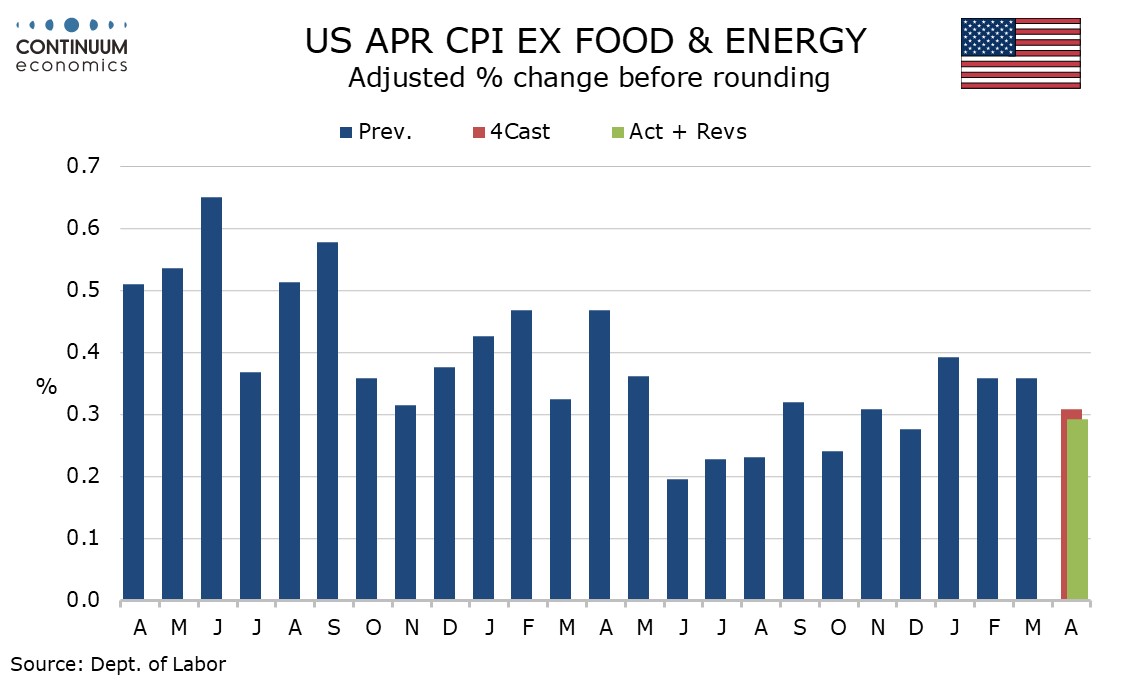

U.S. CPI and Retail Sales Show Some Loss of Momentum in April

May 15, 2024 1:14 PM UTC

April CPI has provided some relief by coming in lower than expected at 0.3% on the headline and while the 0.3% core is on consensus, it is on the soft side at 0.292% before rounding. Retail sales have also lost some momentum in April, unchanged overall, up 0.2% ex autos but down 0.1% ex autos and ga

China: Too Much Debt In Some Sectors

May 15, 2024 9:55 AM UTC

While part of corporate debt is quasi government (SOE and LGFV’s) and China creditors can be pursued to rollover by the authorities for larger borrowers, households and part of the private sector are focused on the previous buildup of debt. With China authorities reluctant to aggressive ease fis

May 14, 2024

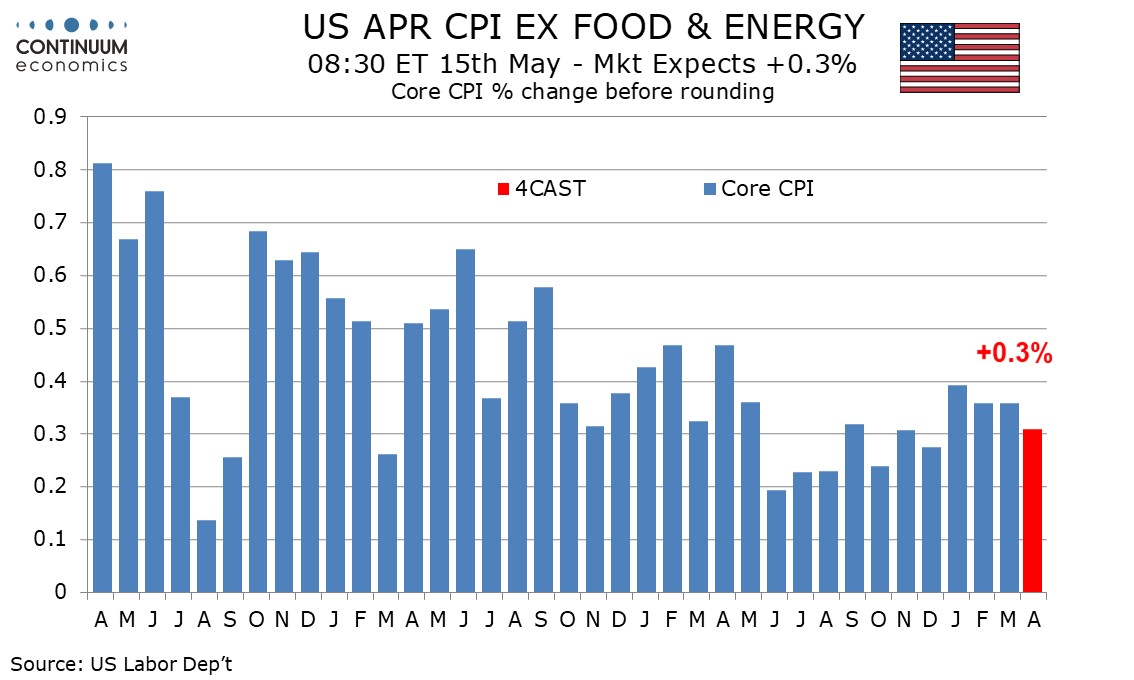

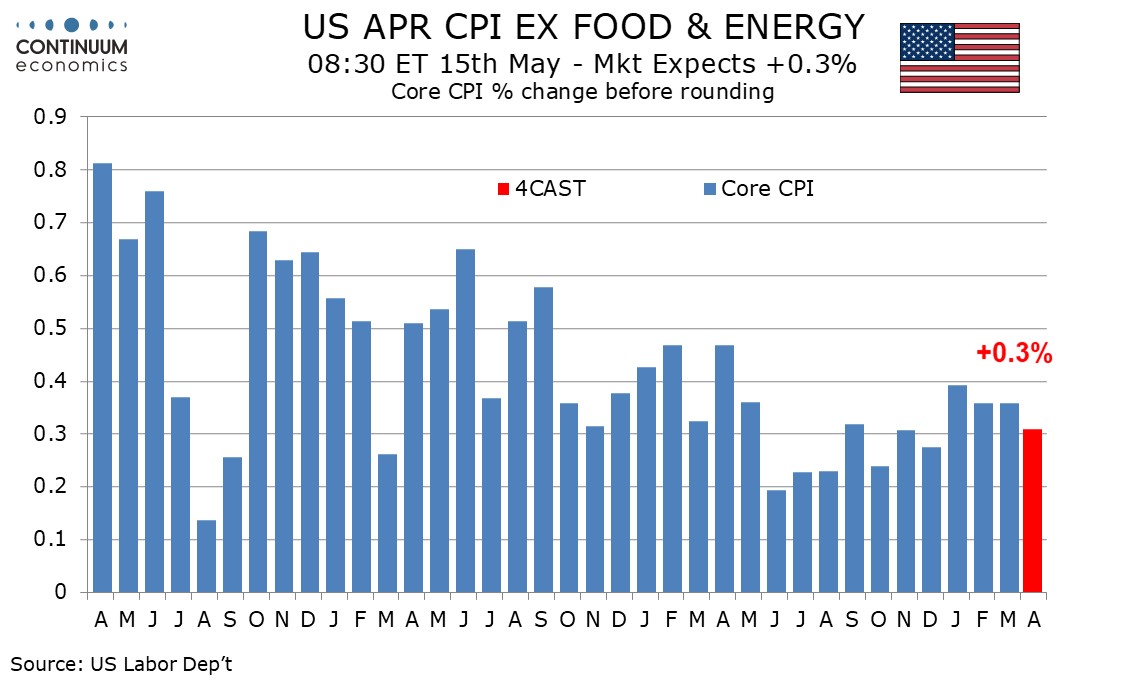

Preview: Due May 15 - U.S. April CPI - Core rate not quite as strong as the preceding three months

May 14, 2024 1:48 PM UTC

We expect April CPI to rise by 0.4% overall for a third straight month but with the ex food and energy pace slowing to 0.3% after three straight months at 0.4%. We expect the strong start to the year to fade as the year progresses, though April PPI strength was disappointing and inflationary pressur

May 13, 2024

China RRR and Rate Cuts

May 13, 2024 7:54 AM UTC

The latest China money supply and lending figures show that private household and business lending is very subdued. More need to be done to boost credit demand as well as credit supply. However, the authorities desires to avoid too much Yuan weakness will likely mean that the next move is a 25bp

Watts at Stake: India's Looming Power Shortage

May 13, 2024 6:58 AM UTC

India's power sector faces rising demand and power shortages, sparking fears of the most significant power shortfall in a decade. With coal imports continuing to rise and hydropower generation declining, India's aim to become a manufacturing hub could become challenging. Energy transition is likely

May 10, 2024

Asset Allocation 2024: Tricky Seven Months Remaining

May 10, 2024 1:06 PM UTC

Fed easing expectations for 2025 and 2026 can shift from a terminal 4% Fed Funds rate towards 3%, as the U.S. economy slows due to lagged tightening effects. Combined with Fed easing starting in September this should mean a consistent decline in 2yr yields. However, 10yr U.S. Treasury yields wil

May 08, 2024

China Equities: A Tactical Play

May 8, 2024 2:20 PM UTC

China equities can see a tactical bounce of 5-10% in the coming months. Cheap valuations and underweight global fund positions means that the scale of pessimism only has to get less bad on the economy and China authorities attitude towards businesses. While we see a tactical opportunity, we do

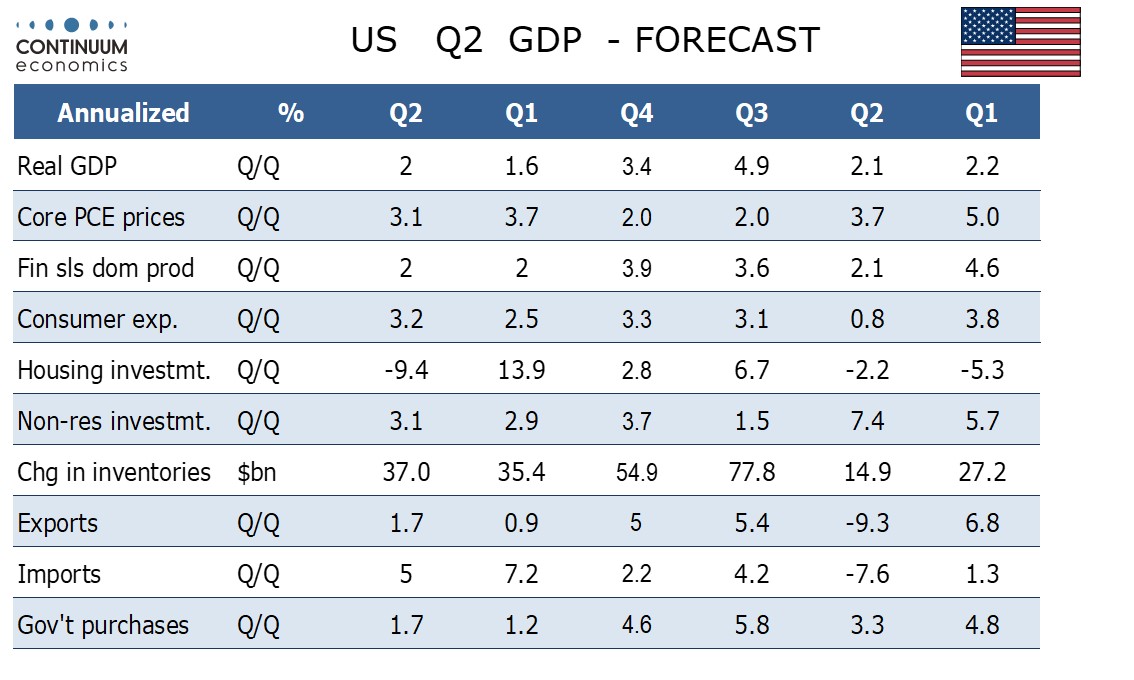

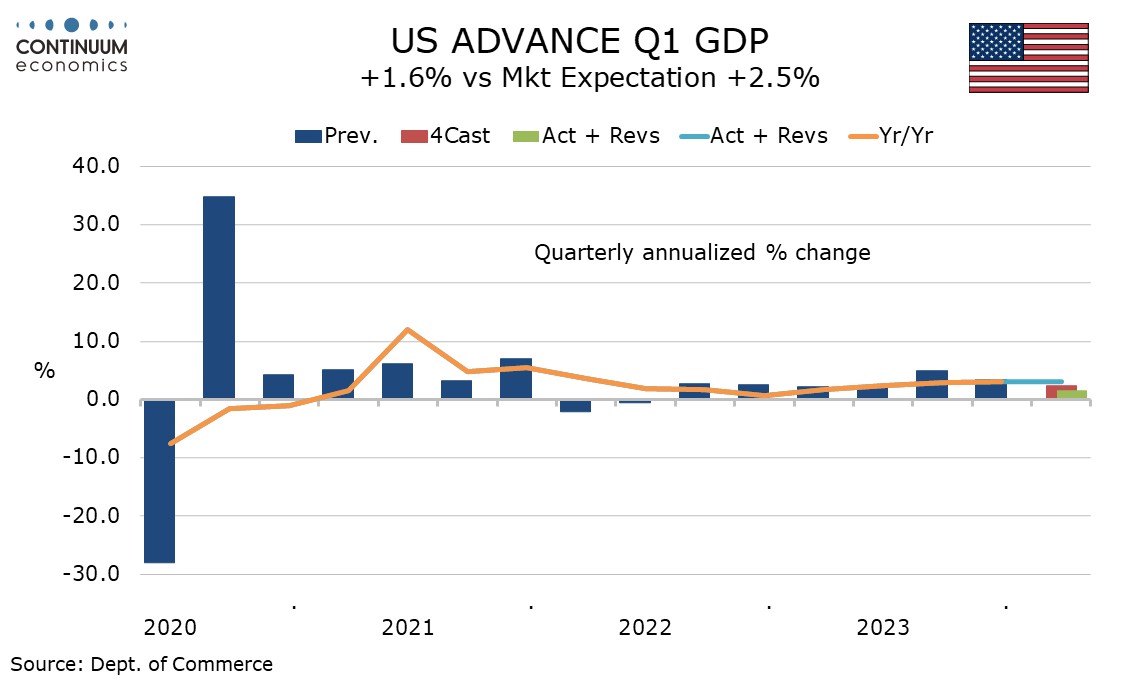

U.S. Q2 GDP to Increase by 2.0% Annualized Before Slowing In the Second Half

May 8, 2024 1:36 PM UTC

In our quarterly outlook on March 22 we looked for Q1 US GDP to rise by 2.4% annualized followed by growth of near 1.0% in the remaining three quarters. While Q1 at 1.6% came in weaker than expected details were constructive for Q2 for which we now expect a 2.0% annualized gain. We continue to expec

May 07, 2024

Indonesia Q4 GDP Review: Robust Start to 2024

May 7, 2024 1:22 PM UTC

Bottom line: Indonesia's Q1 GDP — released on May 6 — saw growth rebound to 5.1% yr/yr from 4.90% yr/yr in Q4 2023. While private consumption continued its ascent, government expenditure emerged as the key driver of Indonesia's growth narrative. Private consumption was supported by festive deman

U.S. Fiscal Problems: 2025 More Than 2024

May 7, 2024 1:10 PM UTC

Current real yields in the U.S. government bond market already large reflect the large government deficit trajectory. Even so, H1 2025 could see some extra fiscal tensions that add 30-40bps to 10yr U.S. Treasury yields as the post president election environment will either see a reelected Joe Bide

May 03, 2024

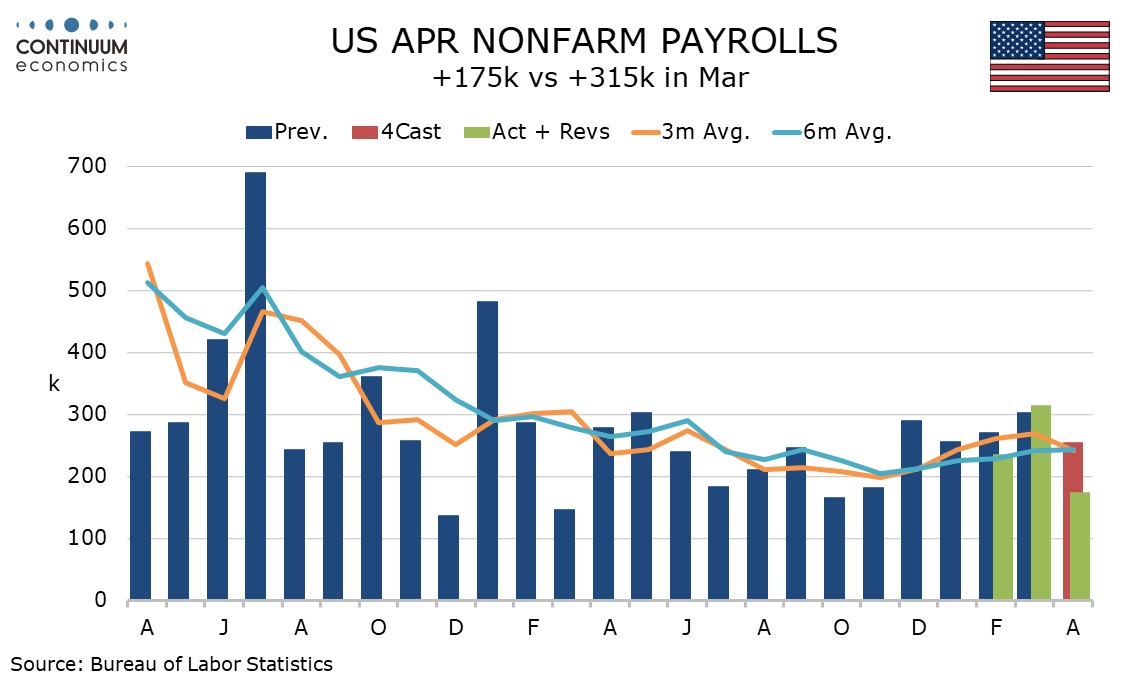

U.S. April Employment - On the weak side in all key details, following strength in March

May 3, 2024 1:18 PM UTC

April’s non-farm payroll is on the low side of consensus across the board, with a 175k increase (though the 167k private sector rise is only modestly below consensus), with a 0.2% rise in average hourly earnings, a fall in the workweek and a rise in unemployment to 3.9% from 3.8%. The data should

EMFX: Diverging On Domestic Forces Not Less Fed Easing Hopes

May 3, 2024 10:45 AM UTC

While U.S. economic developments, plus Fed policy prospects, will be important in terms of EM currency developments, domestic politics and fundamentals will also be decisive. These can keep the South Africa Rand volatile in the remainder of 2024, given the risk of a coalition government and African

May 02, 2024

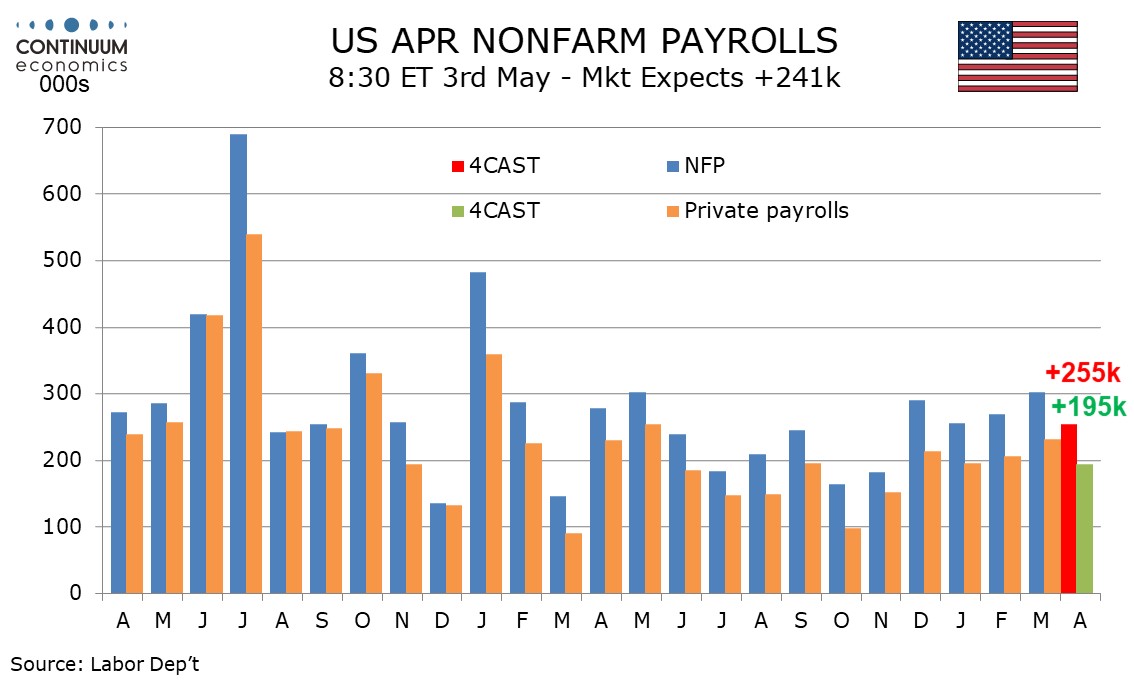

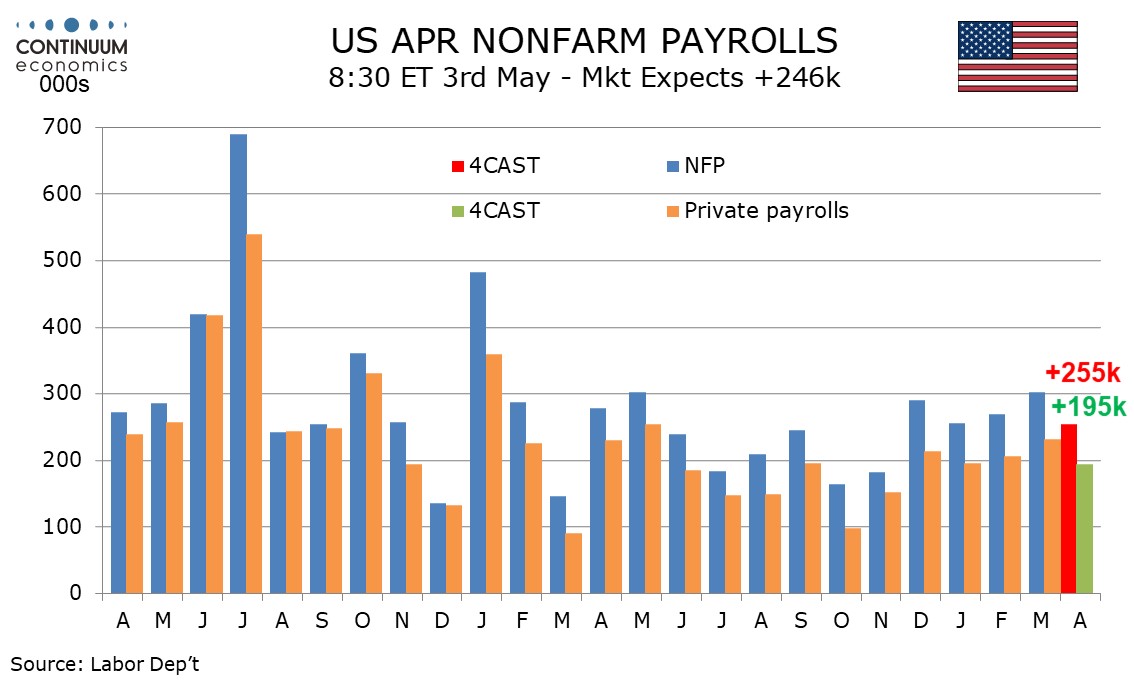

Preview: Due May 3 - U.S. April Employment (Non-Farm Payrolls) - Still strong if a little less so, earnings may be above trend

May 2, 2024 2:03 PM UTC

We expect a 255k increase in April’s non-farm payroll, still strong if the slowest since November, with a 195k increase in the private sector. We expect an unchanged unemployment rate of 3.8% and a slightly above trend 0.4% increase in average hourly earnings, lifted by a minimum wage hike in Cali

China Politburo: Help for Housing, But No Game changers

May 2, 2024 10:50 AM UTC

Politburo statement in late April suggests extra support for residential property. However, we see this as being incremental rather than any game changers and we still see residential investment remaining a negative drag on 2024 GDP growth.

April 30, 2024

Preview: Due May 15 - U.S. April CPI - Core rate not quite as strong as the preceding three months

April 30, 2024 5:15 PM UTC

We expect April CPI to rise by 0.4% overall for a third straight month but with the ex food and energy pace slowing to 0.3% after three straight months at 0.4%. We expect the strong start to the year to fade as the year progresses, though inflationary pressures will still look quite significant in A

April 29, 2024

China: Depreciation Rather Than Devaluation

April 29, 2024 1:00 PM UTC

We feel that a devaluation of the Yuan is unlikely in 2024, both to avoid potentially politically destabilizing capital outflows but also to avoid upsetting the next U.S. president. Policy is geared more towards controlled depreciation to help competiveness but reduce other risks. The Yuan has a

April 26, 2024

Headwinds To Long-term Global Growth

April 26, 2024 9:30 AM UTC

Bottom line: While much focus is on the cyclical economic position to determine 2024 monetary policy prospects, the 2025-28 structural growth trajectory differs to the pre 2020 GDP trajectory for major economies. While global fragmentation has a role to play, aging populations are already having a

April 25, 2024

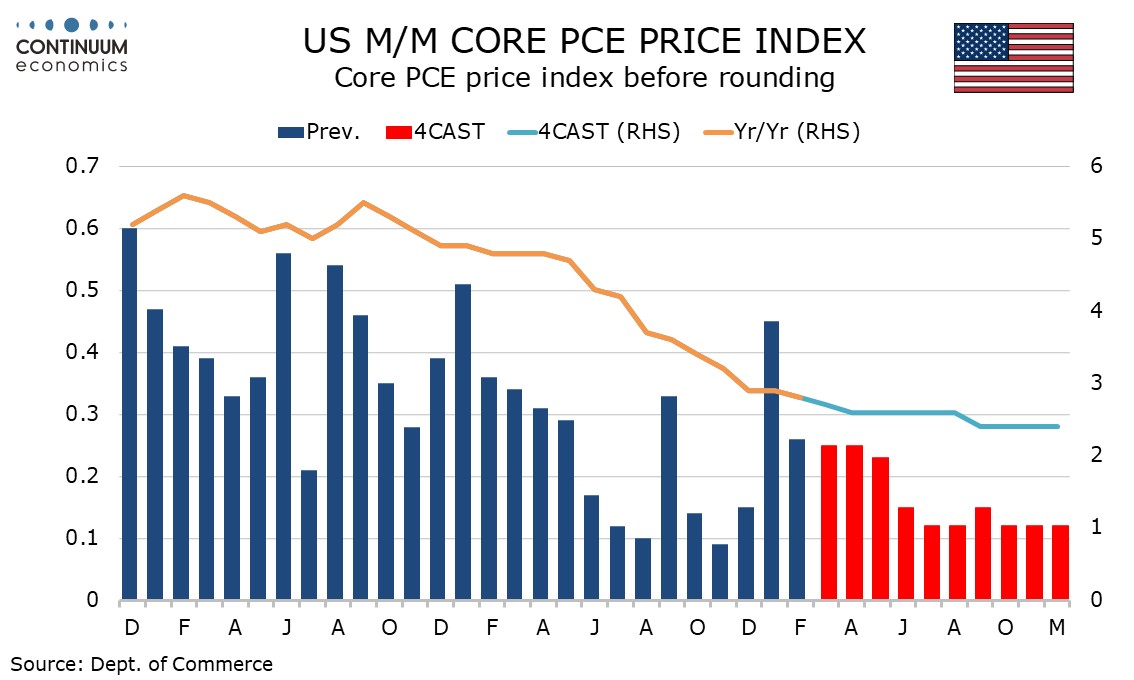

Q1 U.S. GDP Slows on Imports and Inventories, Core PCE Prices Stronger on the Quarter

April 25, 2024 1:14 PM UTC

Q4 GDP has come in weaker than expected at 1.6% annualized but with a stronger than expected 3.7% annualized increase in the core PCE price index. Weaker inventories and stronger imports are the main reason for the GDP slowing so the data is not a clear signal of underlying weakness. Lower initial (

April 24, 2024

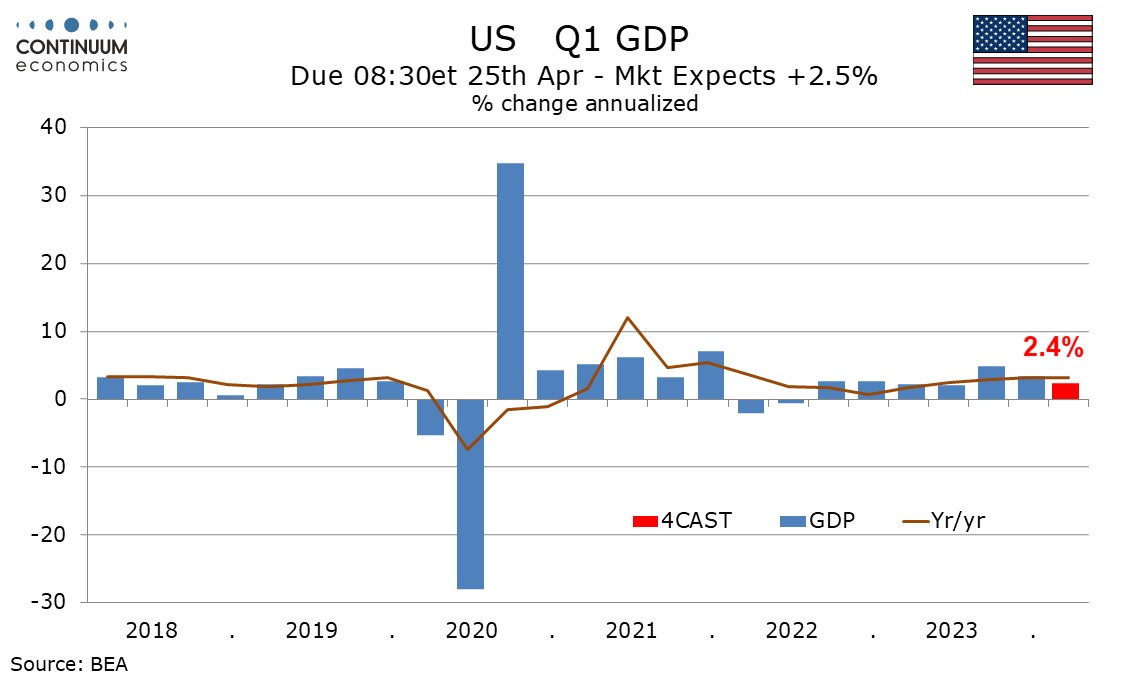

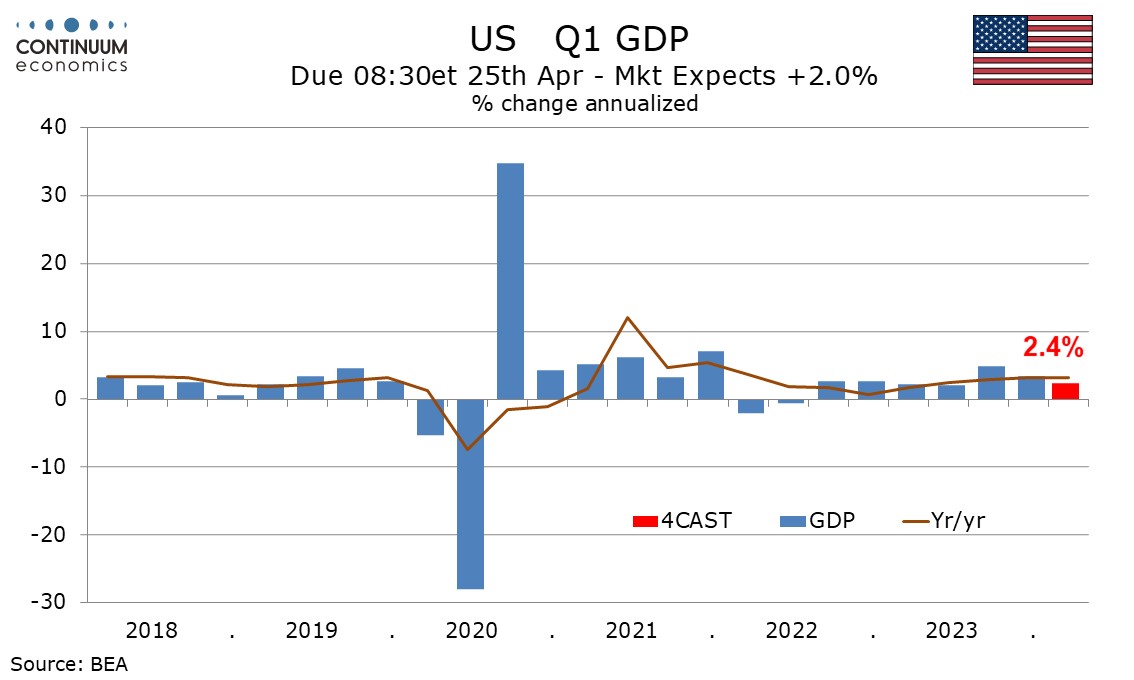

Preview: Due April 25 - U.S. Q1 GDP - Slower but Still Healthy With Stronger Core PCE Prices

April 24, 2024 1:54 PM UTC

We expect a 2.4% annualized increase in Q1 GDP, significantly slower than the second half of 2023 but slightly stronger than the first half and still a heathy pace of growth. We expect a pick up in the core PCE price index to 3.4% annualized after two straight quarters at 2.0%.

China: Surging Government Debt and Does It Matter?

April 24, 2024 9:30 AM UTC

Total non-financial sector debt, plus the IMF estimates of government debt/GDP, do seem to matter for the action of China authorities, as fiscal policy stimulus is targeted rather aggressive as in 2009 or 2015. The overall debt picture also matters for the growth outlook, as the excess debt/GDP le

April 22, 2024

Preview: Due May 3 - U.S. April Employment (Non-Farm Payrolls) - Still strong if a little less so, earnings may be above trend

April 22, 2024 4:44 PM UTC

We expect a 255k increase in April’s non-farm payroll, still strong if the slowest since November, with a 195k increase in the private sector. We expect an unchanged unemployment rate of 3.8% and a slightly above trend 0.4% increase in average hourly earnings, lifted by a minimum wage hike in Cali

Indonesian Court Delivers Verdict: Prabowo prevails

April 22, 2024 3:18 PM UTC

The Constitutional Court dismissed cases against Vice President Gibran Rakabuming Raka and President Joko Widodo. In Gibran's case, the court didn't disqualify him from running for president but sanctioned the election committee for not amending regulations following a previous ruling. This ruling l

Short-end European Government Bonds Following U.S. But June Decoupling

April 22, 2024 1:15 PM UTC

The Fed’s shift to higher for longer has spilled over to drag European government bond yields higher through April. This now looks overdone as a June ECB rate cut is not fully discounted and ECB officials/data clearly point towards a 25bps cut. UK money markets are more out of line, with a Jun

The Pulse of the Nation: Insights into India's 2024 Election

April 22, 2024 7:54 AM UTC

As India braces itself for the upcoming elections, the political landscape is rife with anticipation, strategy, and uncertainty. With the ruling Bharatiya Janata Party (BJP) seeking to consolidate its power and a diverse coalition of opposition forces vying for a chance to unseat them, the stage is

April 18, 2024

China and the South China Sea

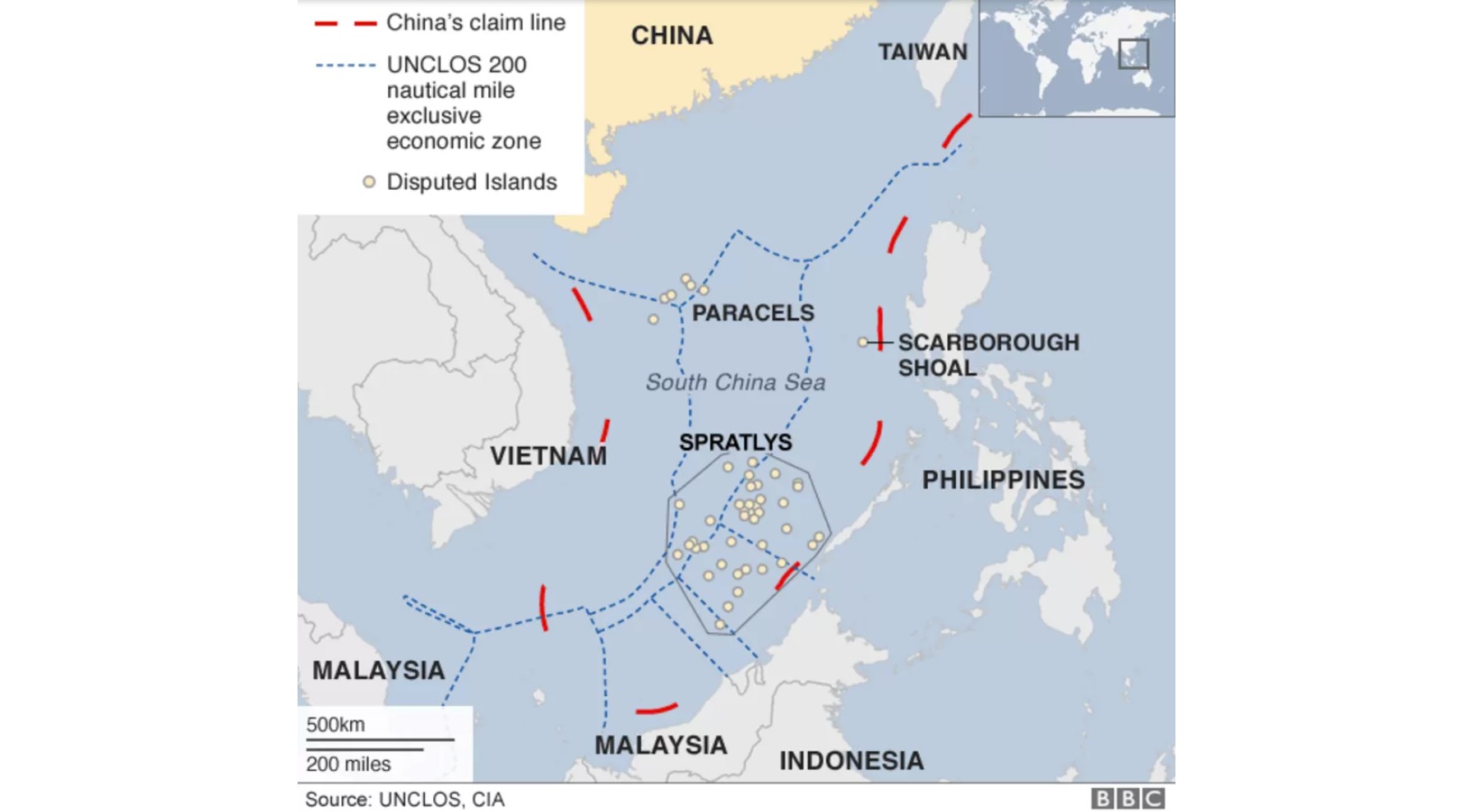

April 18, 2024 2:00 PM UTC

Bottom Line: A China coastguard vessel blocked two Philippines government vessels over the weekend in the Second Thomas shoal area near the Philippines, which has raised questions over whether the South China Sea will be another geopolitical flashpoint. We would say not in 2024, both given China

April 17, 2024

Preview: Due April 25 - U.S. Q1 GDP - Slower but Still Healthy With Stronger Core PCE Prices

April 17, 2024 3:06 PM UTC

We expect a 2.4% annualized increase in Q1 GDP, significantly slower than the second half of 2023 but slightly stronger than the first half and still a heathy pace of growth. We expect a pick up in the core PCE price index to 3.4% annualized after two straight quarters at 2.0%.

Markets: Fed Rather Than Middle East Worries

April 17, 2024 12:34 PM UTC

Global markets are being driven by a scale back in Fed easing expectations and we see a 5-10% U.S. equity market correction being underway. However, with the market now only discounting one 25bps Fed cut in 2024, any downside surprises on U.S. growth or better controlled monthly inflation numbers

April 16, 2024

China: Q1 Upside Surprise, but March Disappoints

April 16, 2024 8:33 AM UTC

Q1 GDP upside surprise was driven mainly by public sector investment. With the government still to implement the Yuan 1trn of special sovereign bonds for infrastructure spending, public investment will likely remain a key driving force. However, the breakdown of the March data show that retail s

April 12, 2024

U.S. PCE Prices, Residual Seasonality and the Fed Outlook

April 12, 2024 6:22 PM UTC

Strength in Q1 inflation data contrasts the encouraging subdued data seen in the second half of 2023, and it looks likely there is some residual seasonality in the data even after seasonal adjustments. The underlying picture is still probably in a gradual downtrend, which should become clear later t

April 10, 2024

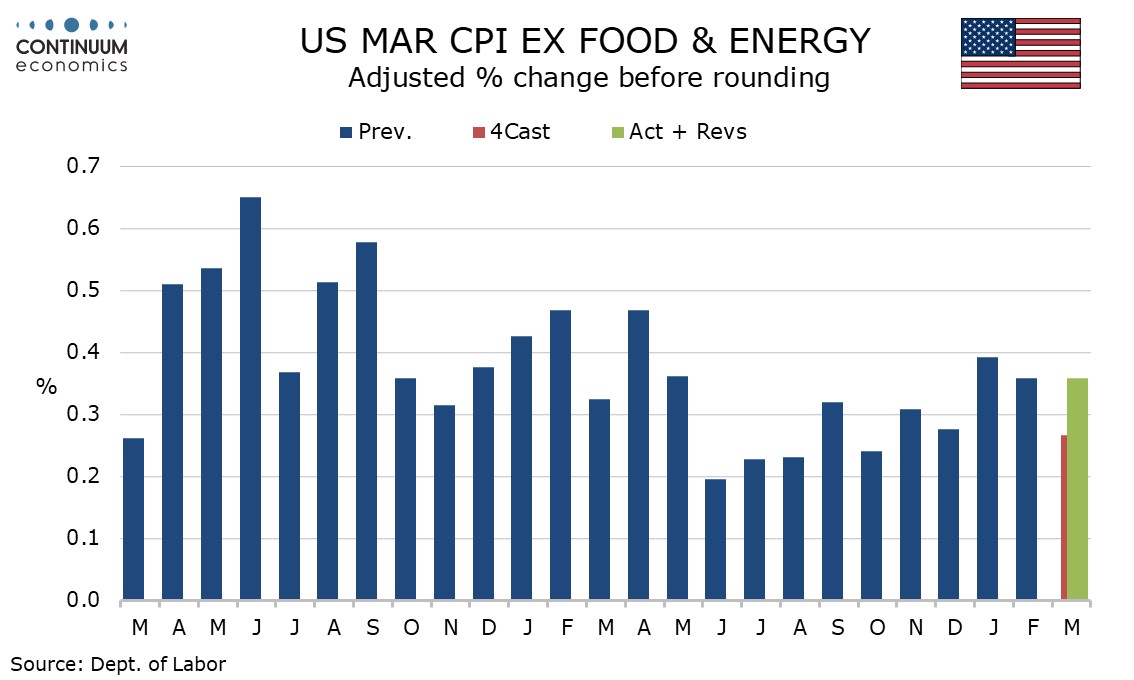

U.S. March CPI - Surprise not dramatic but picture is clearly too high

April 10, 2024 12:55 PM UTC

March CPI has shown a third straight disappointing month at 0.4% overall and ex food and energy, and this suggests that with the economy’s strength persisting, inflation has not yet been defeated, despite the encouraging data seen through the second half of 2023. Still, the market surprise was not

April 09, 2024

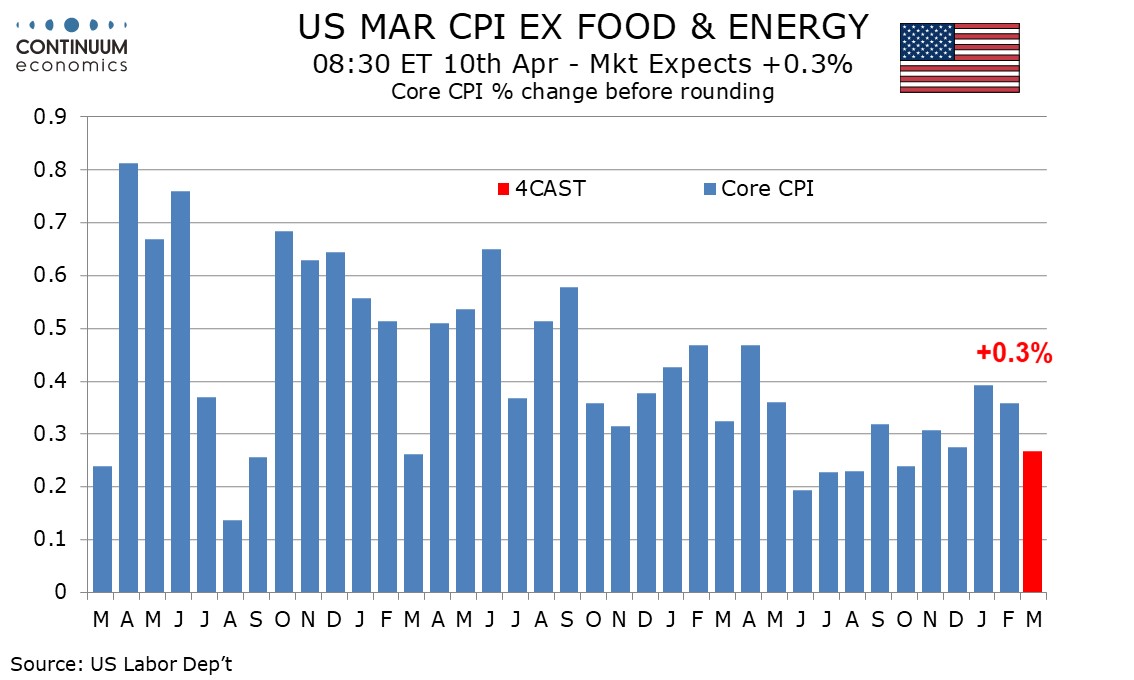

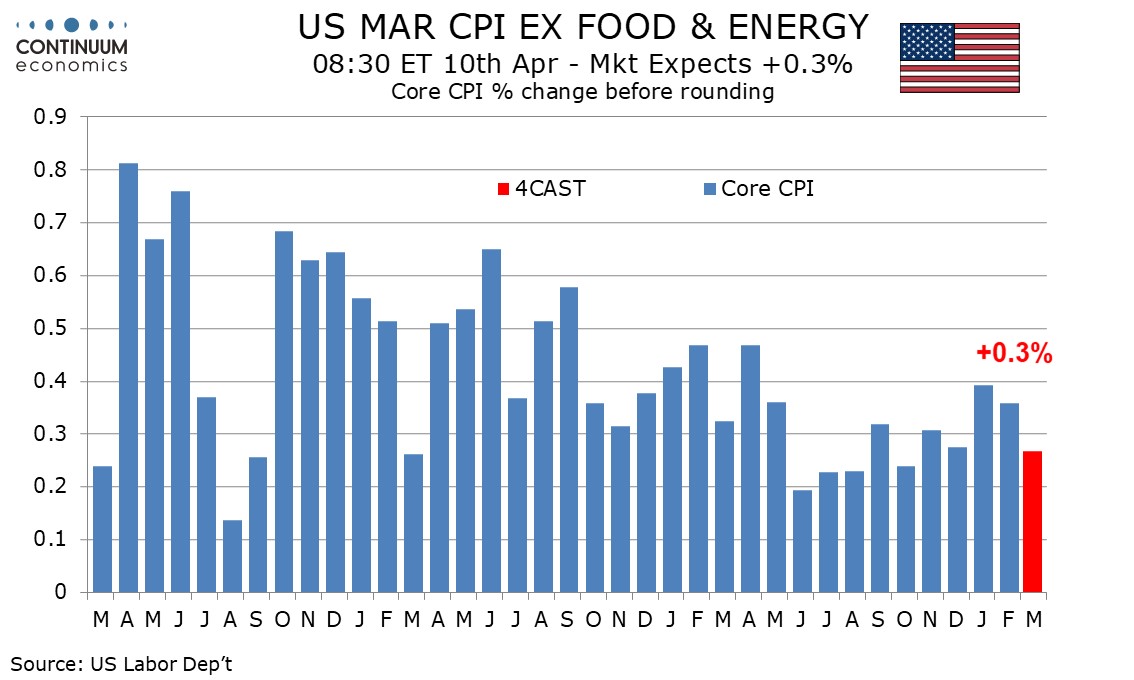

Preview: Due April 10 - U.S. March CPI - Core rate back to trend after two strong months

April 9, 2024 12:27 PM UTC

We expect March CPI to rise by 0.3% both overall and ex food and energy, though before rounding we expect the headline at 0.31% to exceed the core rate at 0.27%, the latter a return to trend after two straight disappointing 0.4% gains seen in January and February.

April 05, 2024

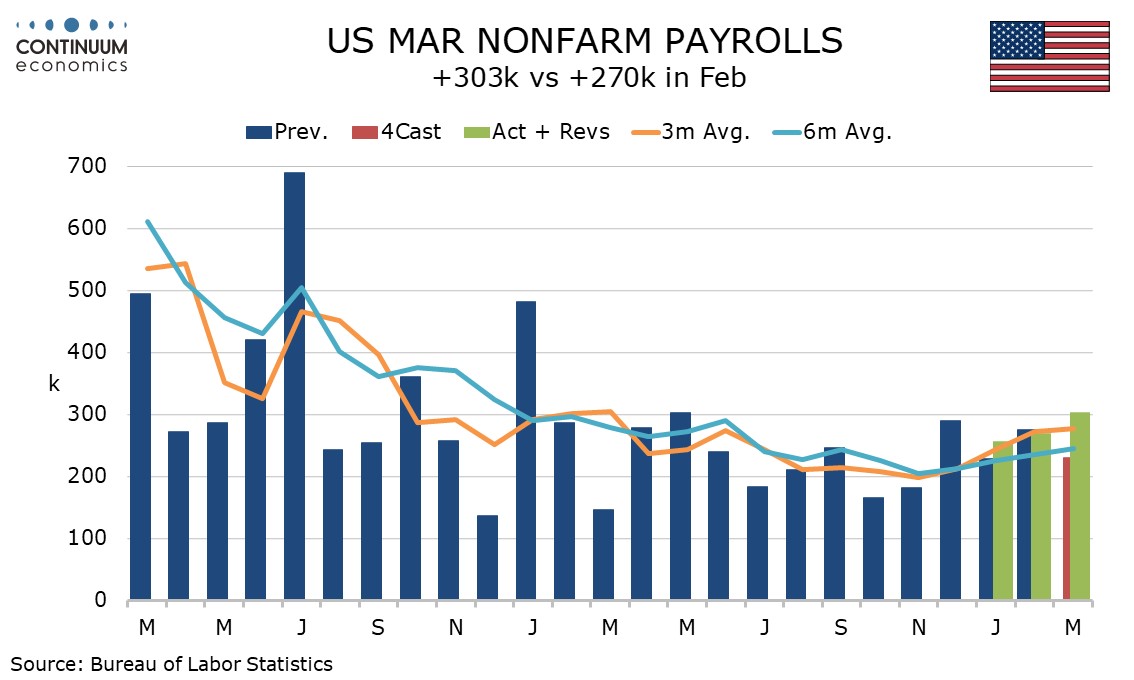

U.S. March Employment - On the strong side in all key details

April 5, 2024 1:08 PM UTC

March’s non-farm payroll increase of 303k is clearly above expectations and maintains a strong pace though the private sector gain of 232k, while above consensus, is not quite as impressive. A rise in the workweek to 34.4 from 34.3 hours adds to a picture of positive activity while unemployment co

April 02, 2024

Asset Allocation: Pausing for Breath

April 2, 2024 9:00 AM UTC

Into Q2, data and policy (actual and perceived) will dominate DM markets. The ECB will likely take the spotlight with a 25bps cut on June 7, as the Fed face a better growth/more fiscal policy expansion and a tighter labor market than the EZ but also with a better productivity backdrop and outlook to

April 01, 2024

Preview: Due April 10 - U.S. March CPI - Core rate back to trend after two strong months

April 1, 2024 5:54 PM UTC

We expect March CPI to rise by 0.3% both overall and ex food and energy, though before rounding we expect the headline at 0.31% to exceed the core rate at 0.27%, the latter a return to trend after two straight disappointing 0.4% gains seen in January and February.

March 27, 2024

Japan: 10yr JGB Yields To Exceed 1% in 2024?

March 27, 2024 10:00 AM UTC

Though BOJ soothed markets with last Tuesday’s rate hike and scrapping of yield curve control, we see scope for 10yr JGB yields to rise through 1% by summer/autumn. The current pace of net JGB purchases is a lot lower than H1 2023, while Ueda noted that this pace could be slowed in the future.

March 26, 2024

EM FX Outlook: Domestic Drivers Key

March 26, 2024 9:01 AM UTC

In terms of spot EM FX projections domestic drivers remain critical, with a desire to avoid appreciation versus the USD for some countries. Fed easing in H2 2024 should however help EMFX more broadly and allow some recovery in spot rates (e.g. Indonesian Rupiah (IDR), South African Rand (ZAR)

March 25, 2024

DM FX Outlook: JPY weakness to reverse

March 25, 2024 12:21 PM UTC

· Bottom Line: Q1 has seen a generally seen a rangebound USD against riskier currencies, but JPY weakness has resumed in spite of a BoJ rate hike and narrowing yield spreads. This reflects continued positive risk sentiment in developed market equities, but we still expect JPY strength t

Equities Outlook: Cyclical Recovery Versus Structural Headwinds

March 25, 2024 9:00 AM UTC

· In the U.S., a tug of war between momentum and U.S. exceptionalism on the one side versus valuations and any deviations from the U.S. goldilocks scenario now means volatility and a risk of a correction. We feel that the U.S. equity market recovery can push onto 5250 for the S&P5

March 22, 2024

Asia/Pacific (ex-China/Japan) Outlook: Election Spending to Drive Growth

March 22, 2024 12:18 PM UTC

· In 2024, growth trends across emerging Asia will exhibit a mixed pattern. Encouragingly, there will be a resurgence in demand for global electronics following a period of stagnation in 2022‑23, which will provide a boost to regional trade. Moreover, the initiation of monetary policy

U.S. Outlook: Fed to Ease as Economy Gradually Slows

March 22, 2024 10:00 AM UTC

• The U.S. economy has continued to see growth surprising to the upside supported in particular by consumer spending. While the momentum of the second half of 2023 will be difficult to sustain the economy now looks poised for a soft landing, with risk that continued resilience in the econom

March 18, 2024

China: Unbalanced Growth

March 18, 2024 8:28 AM UTC

The February monthly data shows unbalanced growth. Industrial production and public investment picked up, but retail sales slowed and residential property remains a negative drag on GDP. While H1 GDP growth will be ok, it will likely slow in H2 and we still stick to a forecast of 4.4% for 2024 a

March 15, 2024

China: No PBOC MTF Cut and Protesting Low Government Bond Yields

March 15, 2024 8:51 AM UTC

Bottom Line: The PBOC decided not to cut the Medium-Term Facility (MTF) rate, but surprised by also withdrawing liquidity in what looks like a protest at the recent decline in government bond yields. A 10bps MTF cut should still arrive in Q2, but later rather than sooner.

March 12, 2024

Japanese Equities: Yen Headwind Rather than Tailwind

March 12, 2024 11:23 AM UTC

Bottom Line: Japanese equities tailwind from a weak JPY boosting corporate earnings will likely go into reverse, as the extreme JPY undervaluation ebbs with small BOJ rate hikes and Fed easing. We also forecast less nominal GDP growth in 2024 and 2025 than the market consensus. As this come thro

March 11, 2024

China: Lunar New Year Boosts CPI, But Disinflation Still In Place

March 11, 2024 8:29 AM UTC

Bottom Line: February China CPI surged to +0.7% v -0.8% Yr/Yr due to three factors. The late lunar New Year boosted CPI seasonally, while the good lunar New Year also boosted pork/food prices and travel prices. The bounce is unlikely to be sustained and we see a fall back to 0.3-0.4% Yr/Yr in Ma

March 08, 2024

India's Q3 GDP: Strong But Uneven Growth

March 8, 2024 2:30 PM UTC

India's economic landscape witnessed a remarkable upswing in Q3-FY24, with a real GDP growth rate of 8.4%, surpassing both street estimates and the Reserve Bank of India's (RBI) projections. This surge not only solidifies India's position as the fastest-growing major economy globally but also unde