View:

August 07, 2026

FX Weekly Strategy: Asia, Aug 10-14

August 7, 2026 3:55 PM UTC

Outside of Iran, focus turns to key US CPI. Trend has been for very few core upside surprises

UK sees GDP, heatwave risks downside surprise, GBP kneejerk

Japan eyes BoJ comments from last meeting, to read the appetite for a Sep hike

Gold and silver still attempting to breakout higher from base

Preview: Due August 18 - U.S. July Industrial Production - Modest manufacturing gain, stronger overall

August 7, 2026 3:45 PM UTC

We expect a 0.4% increase in July industrial production to follow two straight gains of 0.1%. For manufacturing we expect an increase of 0.2%, also improved from a flat June and a 0.1% increase in May.

Preview: Due August 18 - U.S. July Housing Starts and Permits - Modest declines, consistent with trend

August 7, 2026 3:07 PM UTC

We expect July housing starts to fall by 4.7% to 1360k while permits fall by 0.3% to 1370k. Trends in the housing sector appear to be showing a modest loss of momentum entering Q3.

Canada July Employment - Labor market slack being reduced

August 7, 2026 1:50 PM UTC

Canada’s July employment report comes as quite a contrast to the US one, with a strong employment gain of 75.1k and a fall in unemployment to 6.4% from 6.5% coming despite a 60.5k bounce in the labor force. Wages were however weak in the Canadian report, falling to 3.0% yr/yr from 3.7%. Canada’s

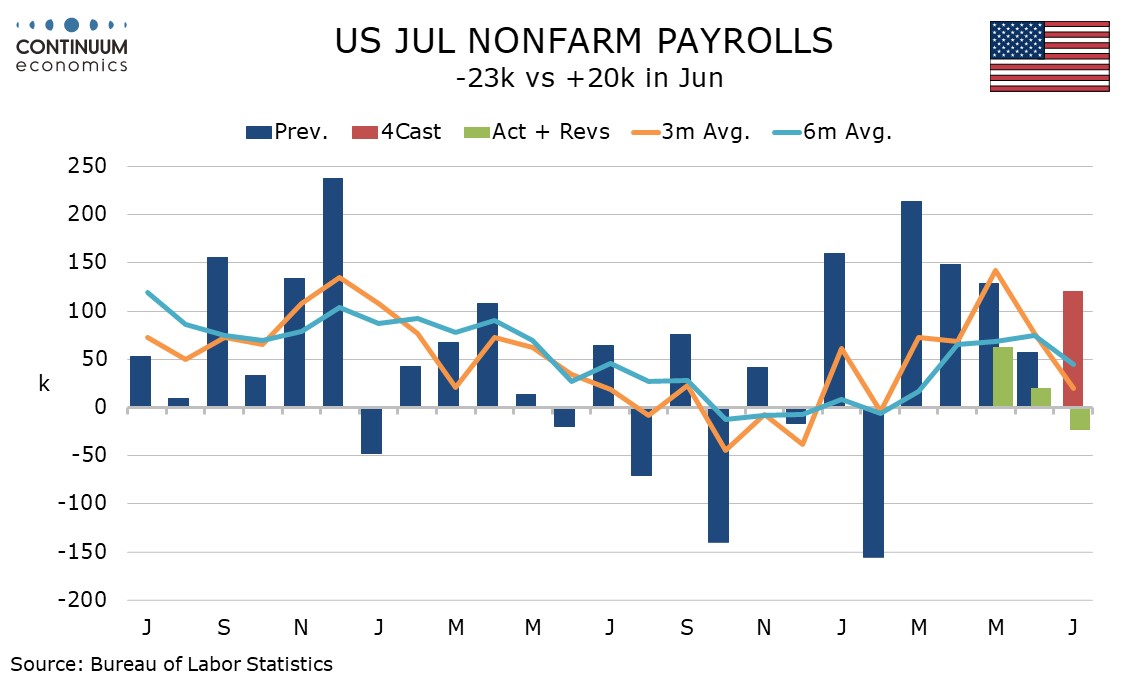

U.S. July Employment - Softer payroll and falling unemployment hint at labor shortages, but no lift to earnings

August 7, 2026 1:21 PM UTC

July’s non-farm payroll at -23k with negative back month revisions is weaker than expected but largely because of negatives in government led by local government education and leisure and hospitality, which may reflect labor shortages. A declining labor force saw the unemployment rate fall, to 4.1

U.S. July Employment - Softer payroll and falling unemployment hint at labor shortages, but no lift to earnings

August 7, 2026 1:20 PM UTC

July’s non-farm payroll at -23k with negative back month revisions is weaker than expected but largely because of negatives in government led by local government education and leisure and hospitality, which may reflect labor shortages. A declining labor force saw the unemployment rate fall, to 4.1

EUR/USD, USD/JPY Flows: Payrolls pressures $ longs, even with unemployment rate proviso

August 7, 2026 12:43 PM UTC

Downside payrolls surprises with revisions - although note that zero or less is now trend...

Unemployment rate dip one counterpoint, though soft earnings the deciding factor

Focus turns to inflation data, but long $ positioning hit again, USD/JPY retains downside skew