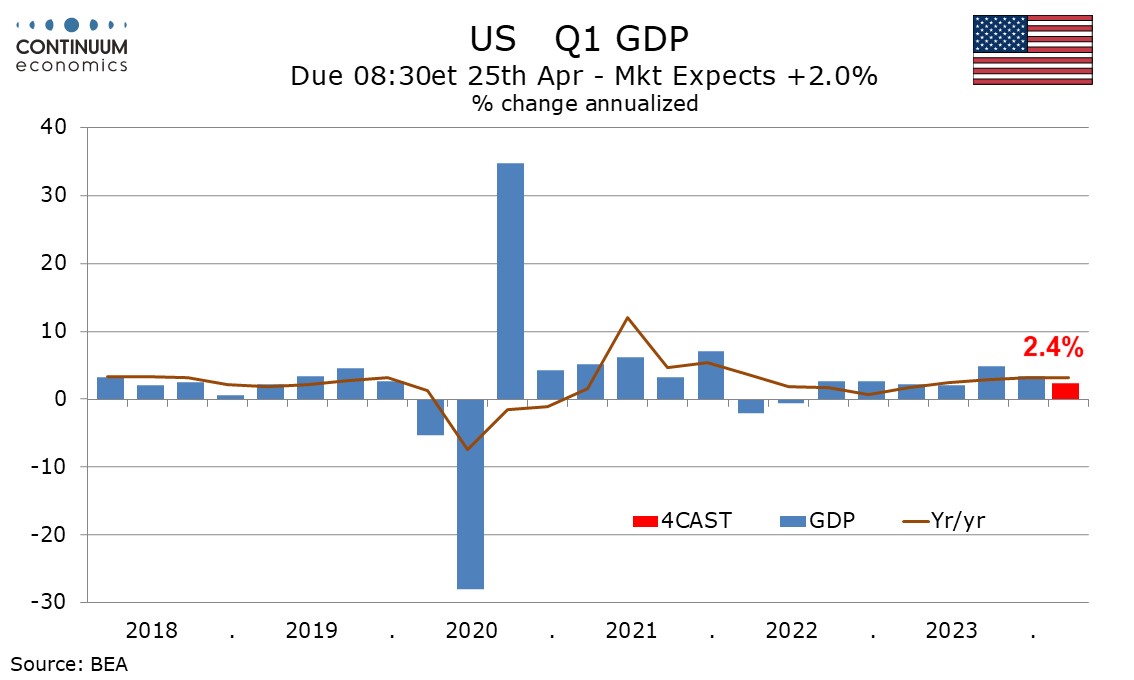

Preview: Due April 25 - U.S. Q1 GDP - Slower but Still Healthy With Stronger Core PCE Prices

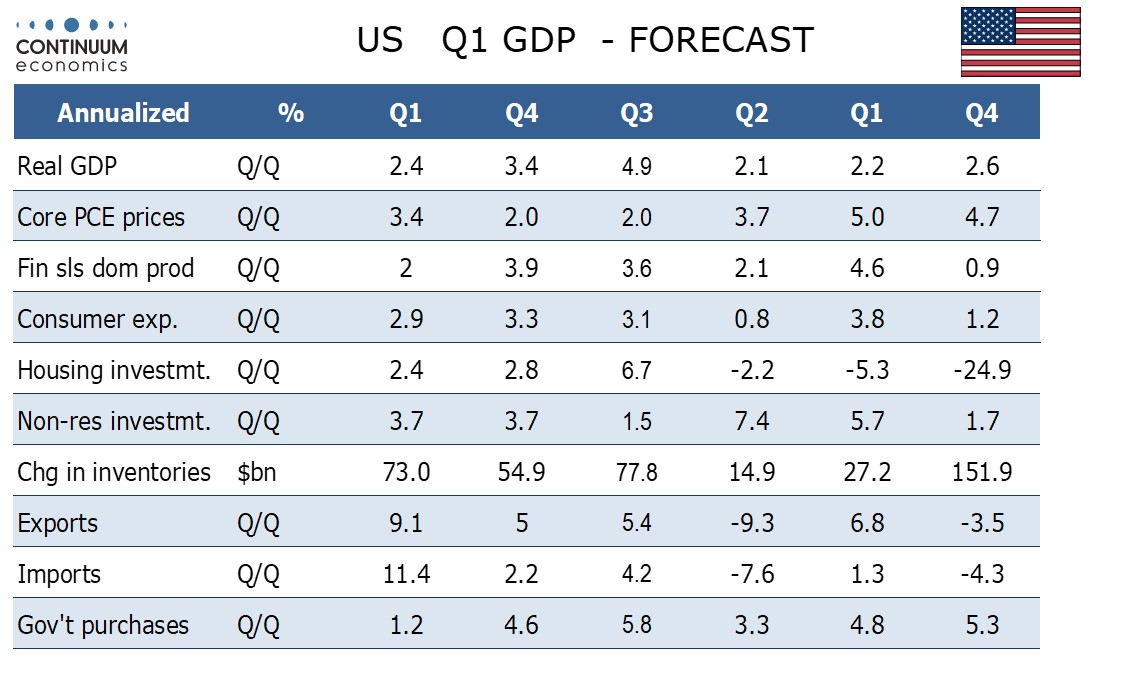

We expect a 2.4% annualized increase in Q1 GDP, significantly slower than the second half of 2023 but slightly stronger than the first half and still a heathy pace of growth. We expect a pick up in the core PCE price index to 3.4% annualized after two straight quarters at 2.0%.

A 2.4% increase will not be a conclusive signal that a significant underlying slowing is under way, with much of the slowing due to a bounce in imports hitting net exports, and bad weather in January hitting the Q1 total. March data is mostly showing solid momentum entering Q2.

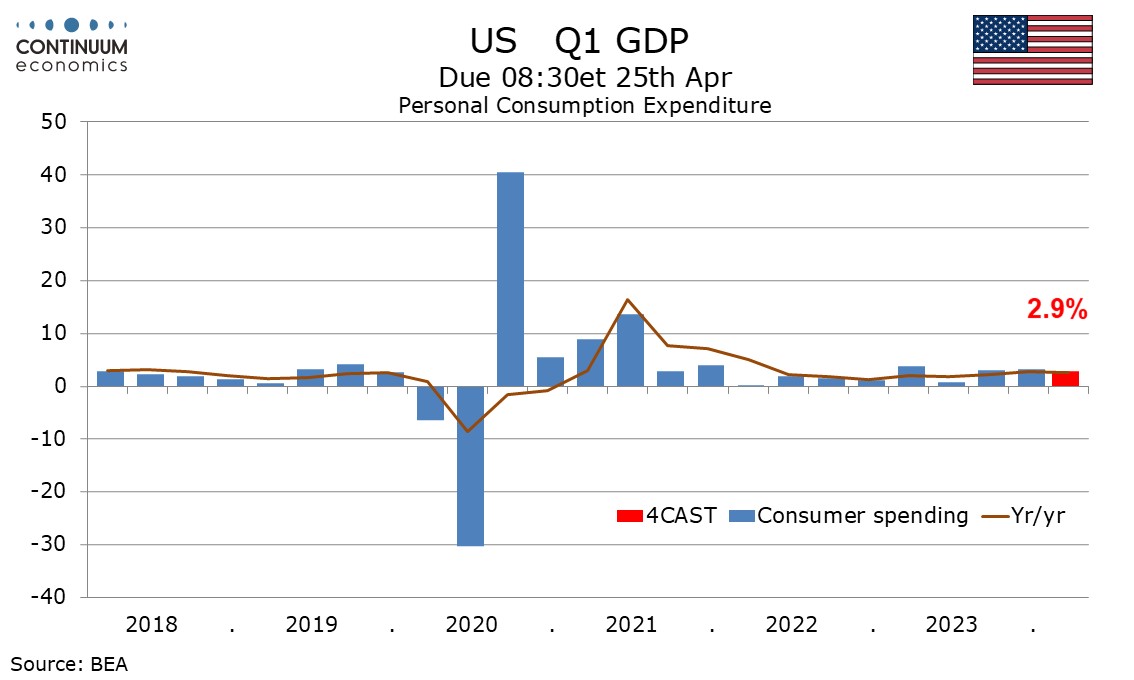

We expect a 2.9% increase in consumer spending after two straight gains slightly above 3.0%, with mixed detail.

We expect a 2.9% increase in consumer spending after two straight gains slightly above 3.0%, with mixed detail.

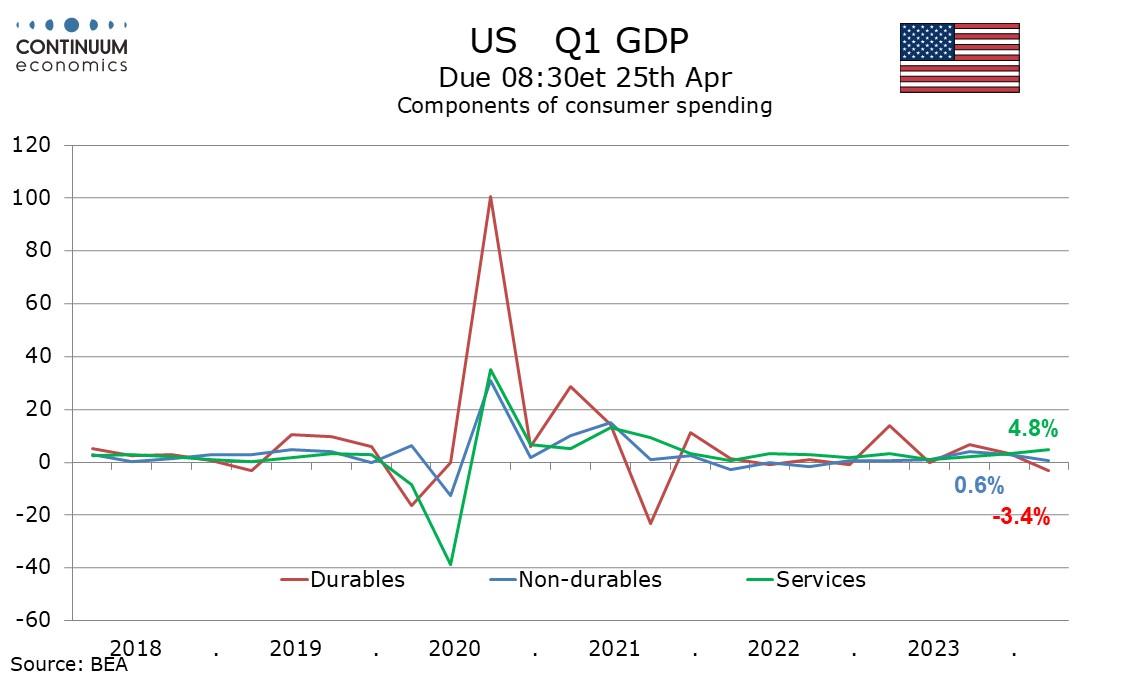

Retail data will still look subdued despite stronger than expected March data that lifted our GDP forecast from 2.0%. but services are heading for a gain of 4.8%, which would be the strongest since Q3 2021.

Consumer spending will continue to outpace real disposable income, where we expect a rise of only 1.1%. Savings built up during the pandemic and rising equities are likely supporting spending, but the current pace will be difficult to sustain going forward.

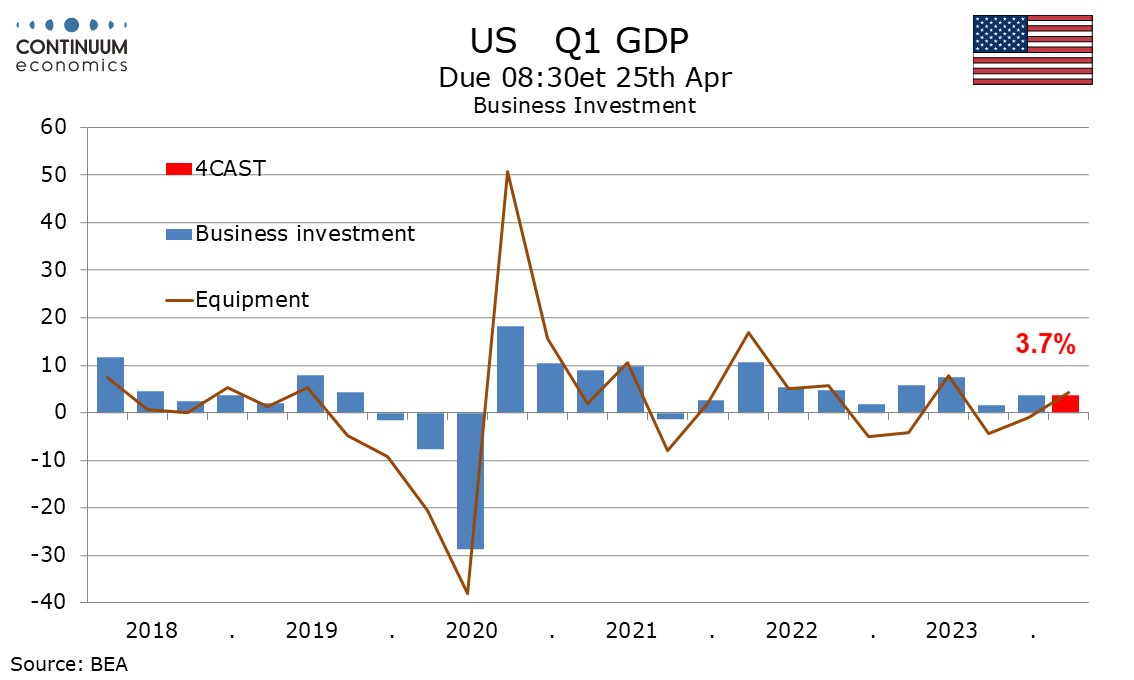

We expect a 3.7% increase in business investment, matching the Q4 increase, with a pick up from two straight declines in equipment but with structures slowing significantly from four straight strong gains.

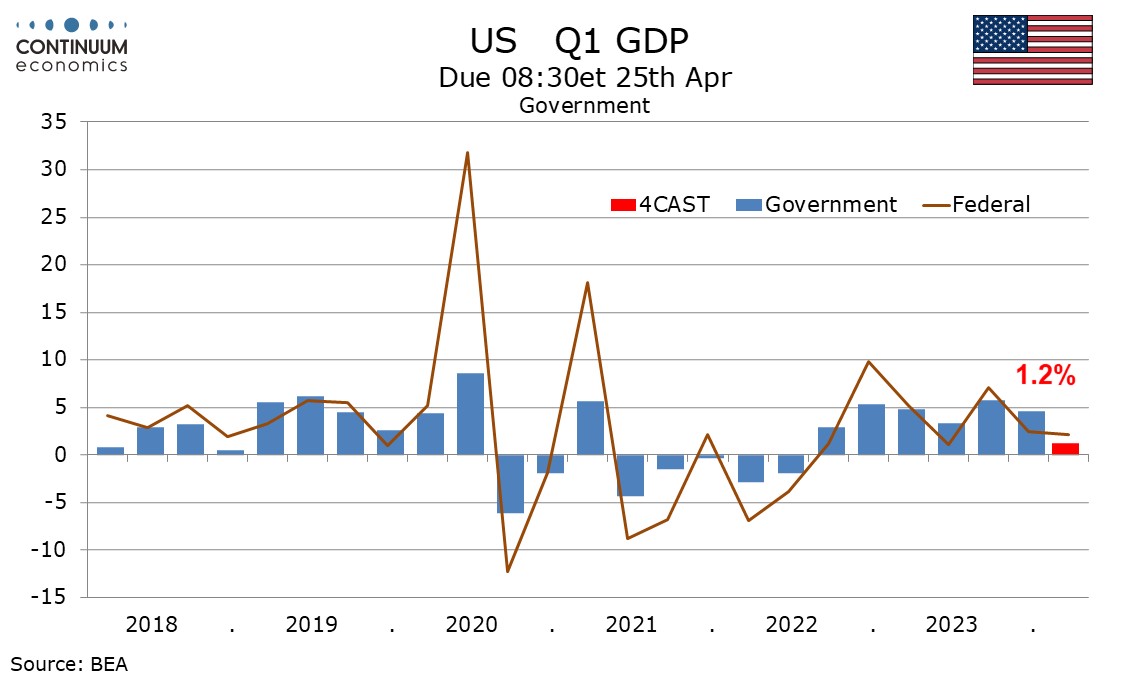

Construction spending has generally been weaker in Q1 to date, with weather probably a factor. Slower public construction spending has us forecasting a seven quarter low 1.2% increase in government.

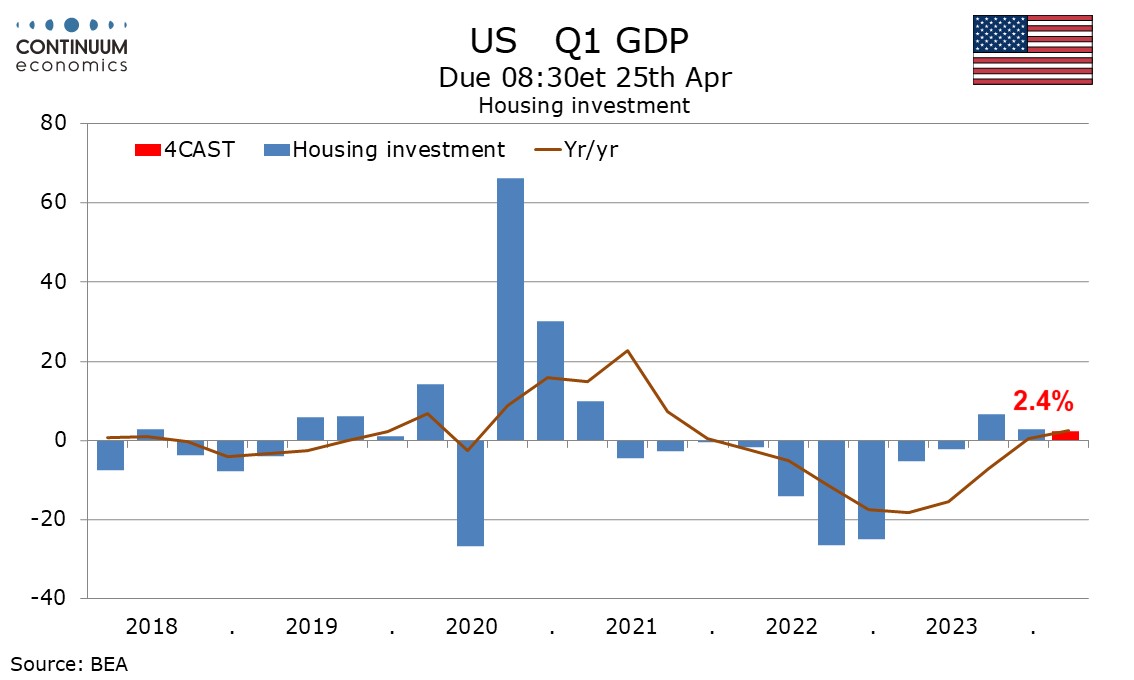

Residential construction has been holding up better. We expect residential investment to rise by 2.4%, versus 2.8% in Q4.

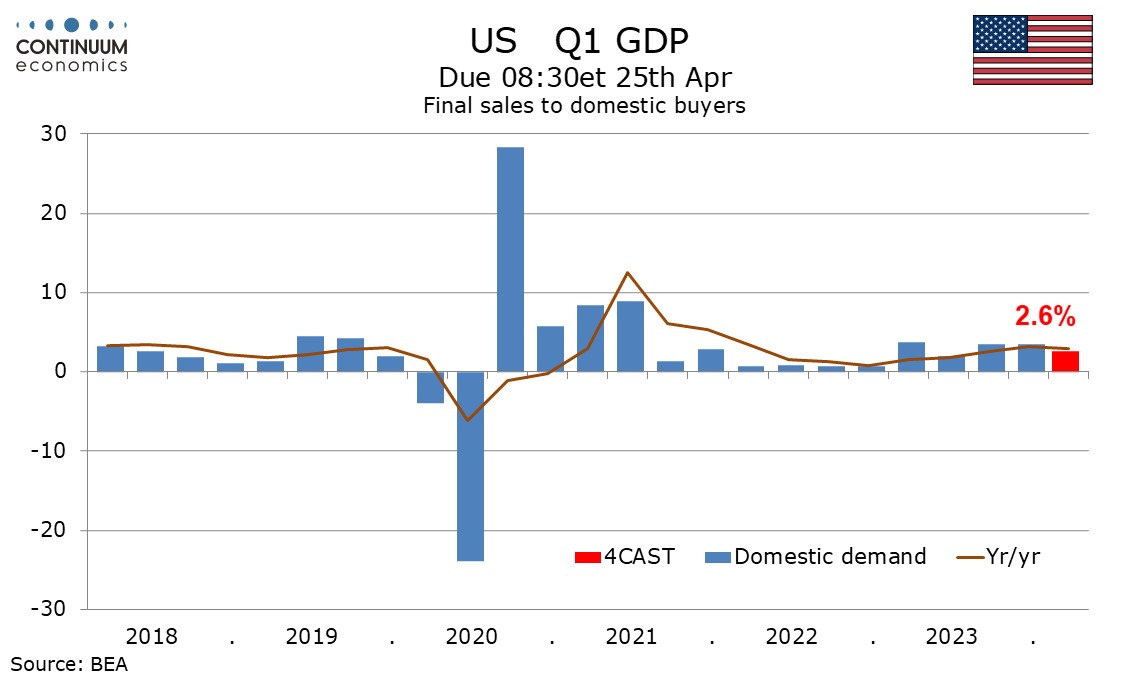

Under our forecast final sales to domestic buyers (GDP less inventories and net exports) would rise by 2.6% after two straight gains of 3.5%.

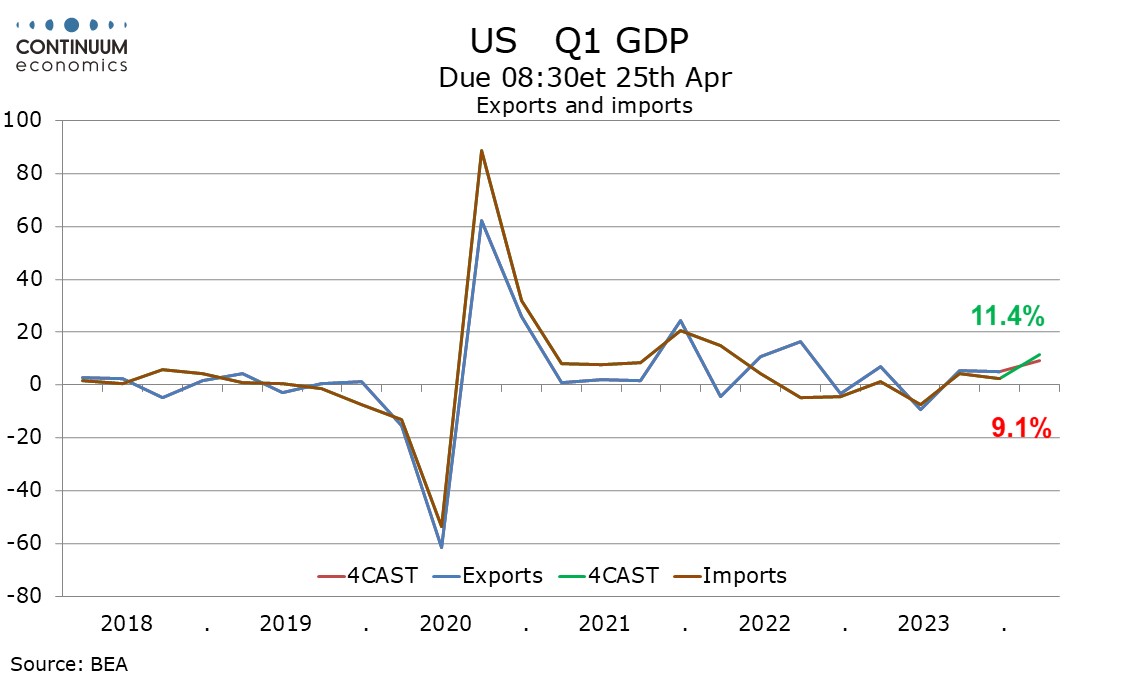

Net exports is likely to be a significant negative taking 0.6% off GDP though this will be due to a strong 11.8% rise in imports outpacing a healthy 9.1% rise exports and thus not a suggestion of economic weakness. The imports gain will comfortably outpace that of exports in USD terms.

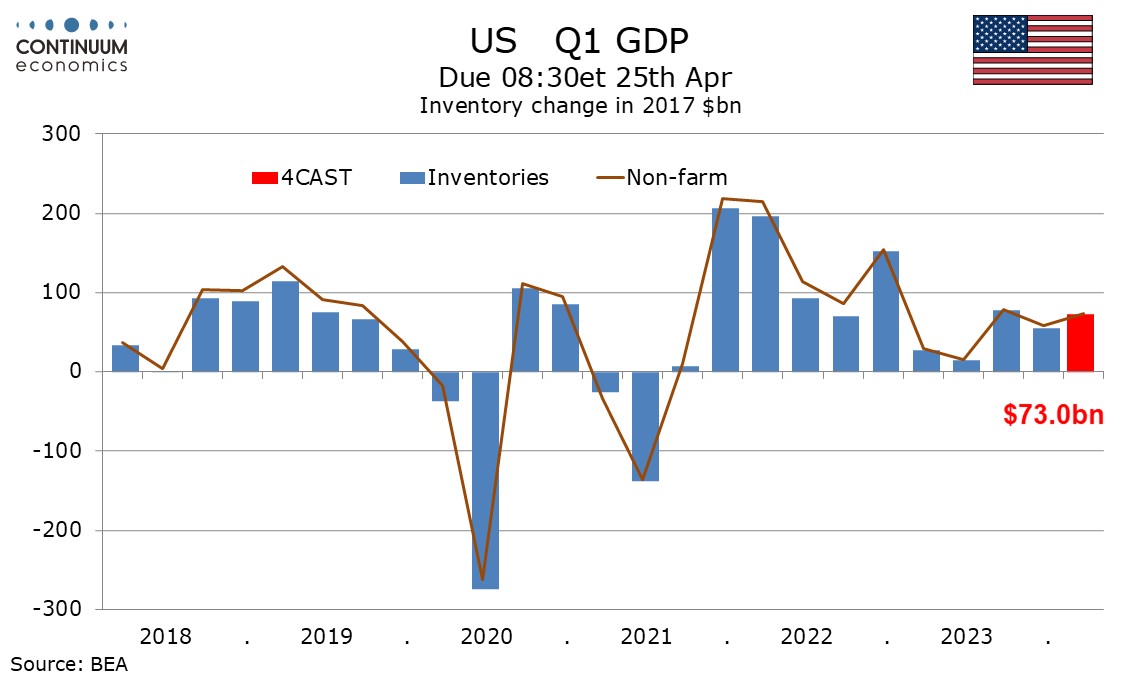

Some of the rise in imports will go into inventories, where we expect a positive contribution of 0.4% to GDP.

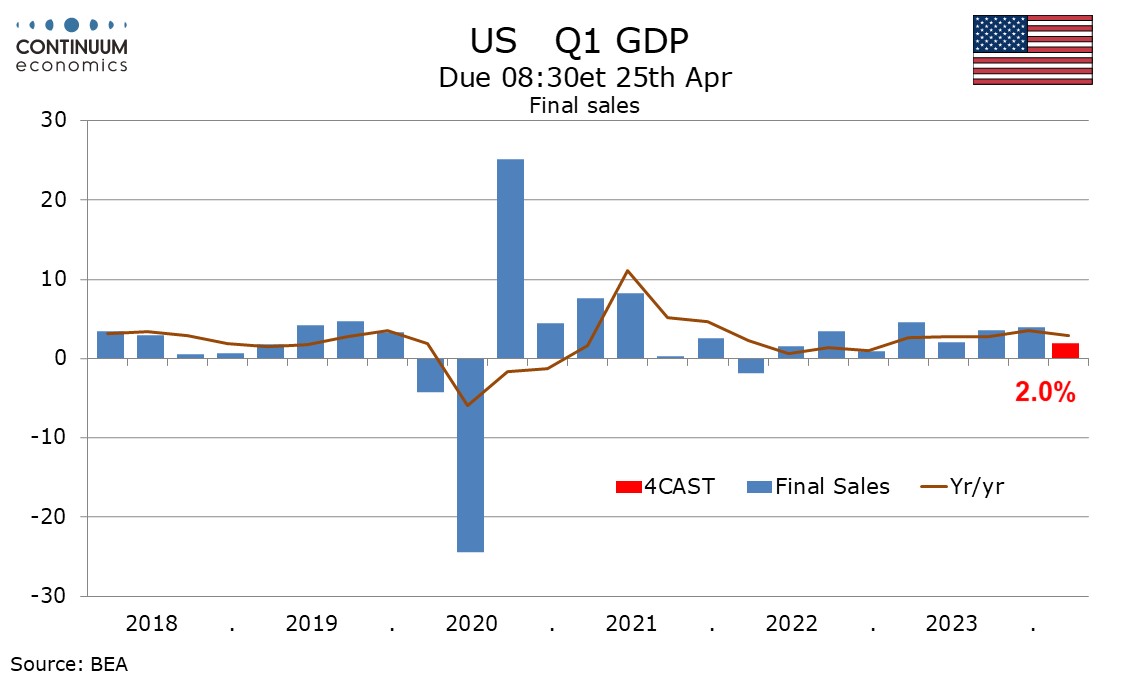

We expect final sales (GDP less inventories) to rise by 2.0%.

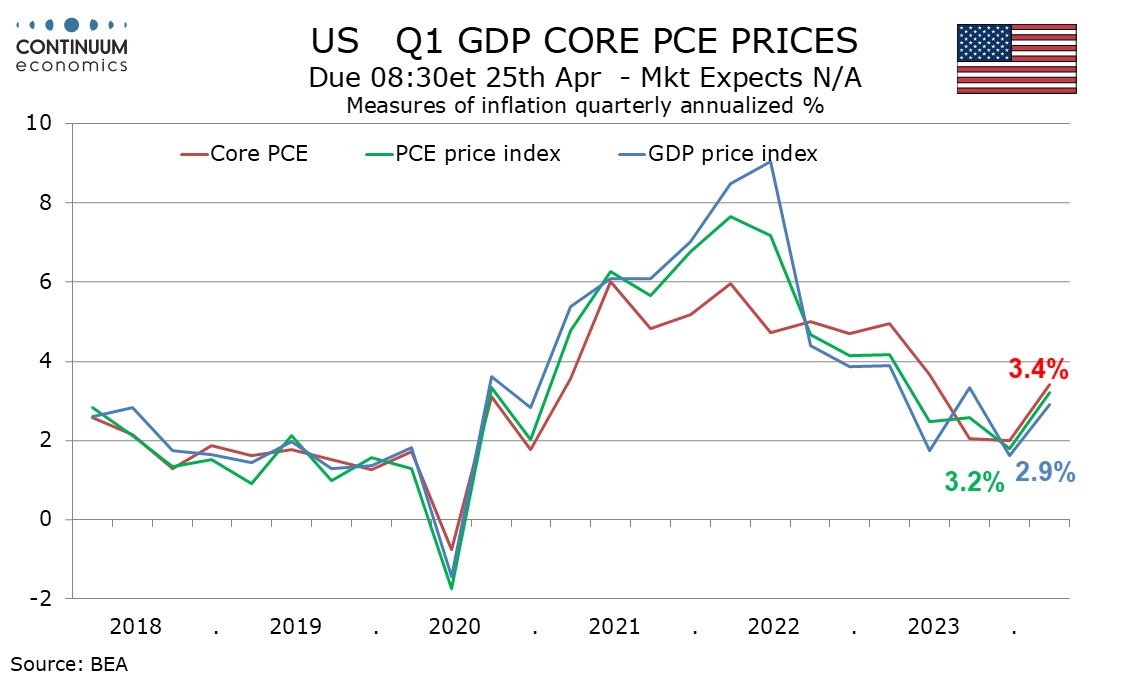

After strong data in January and to a lesser extent February, and with continued strength seen in March’s core CPI, Q1 is set to see an acceleration in core PCE prices, we project by 3.4%, after two straight quarters at 2.0%. We see overall PCE prices at 3.2% and the GDP price index at 2.9%.