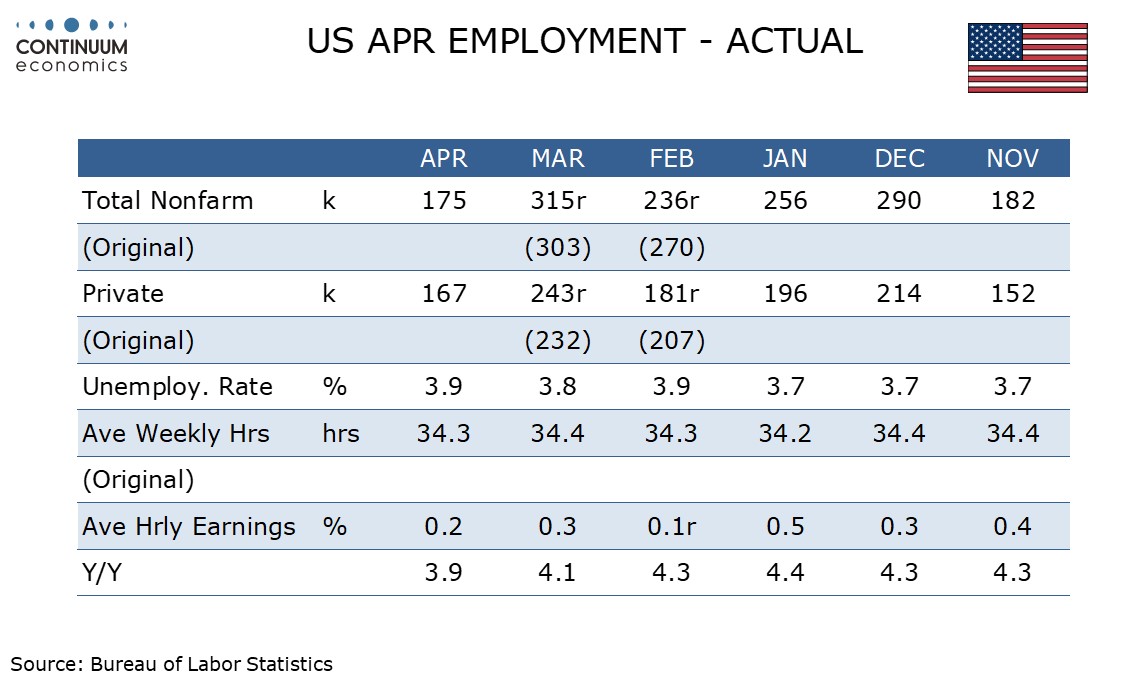

U.S. April Employment - On the weak side in all key details, following strength in March

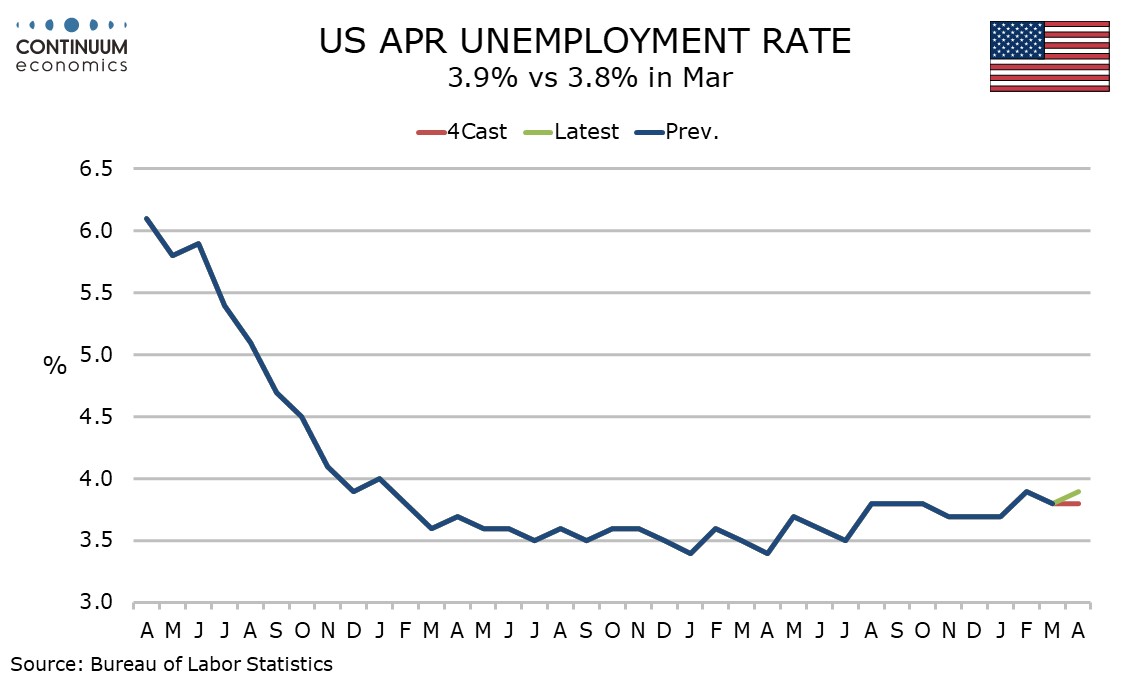

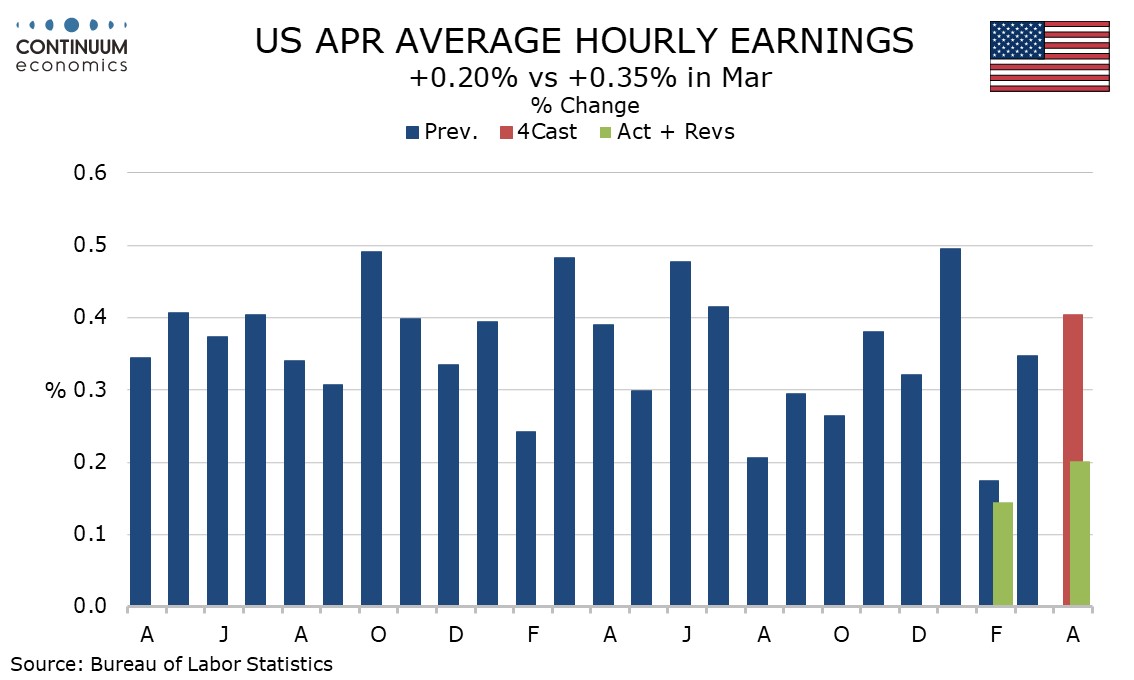

April’s non-farm payroll is on the low side of consensus across the board, with a 175k increase (though the 167k private sector rise is only modestly below consensus), with a 0.2% rise in average hourly earnings, a fall in the workweek and a rise in unemployment to 3.9% from 3.8%. The data should not be seen as weak, but does suggest the economy is losing momentum from recent strength.

Revisions were net a modest negative at 22k though March was revised even stronger to 315k from 303k while February was revised down to 236k from 256k. The average of the stronger March and slower April of 245k is similar to the three and six month averages, which both stand at 242k. One month of slower data after a very strong month should not be overstated. April may have been weaker than expected in all key details, but March was stronger than expected in all key details.

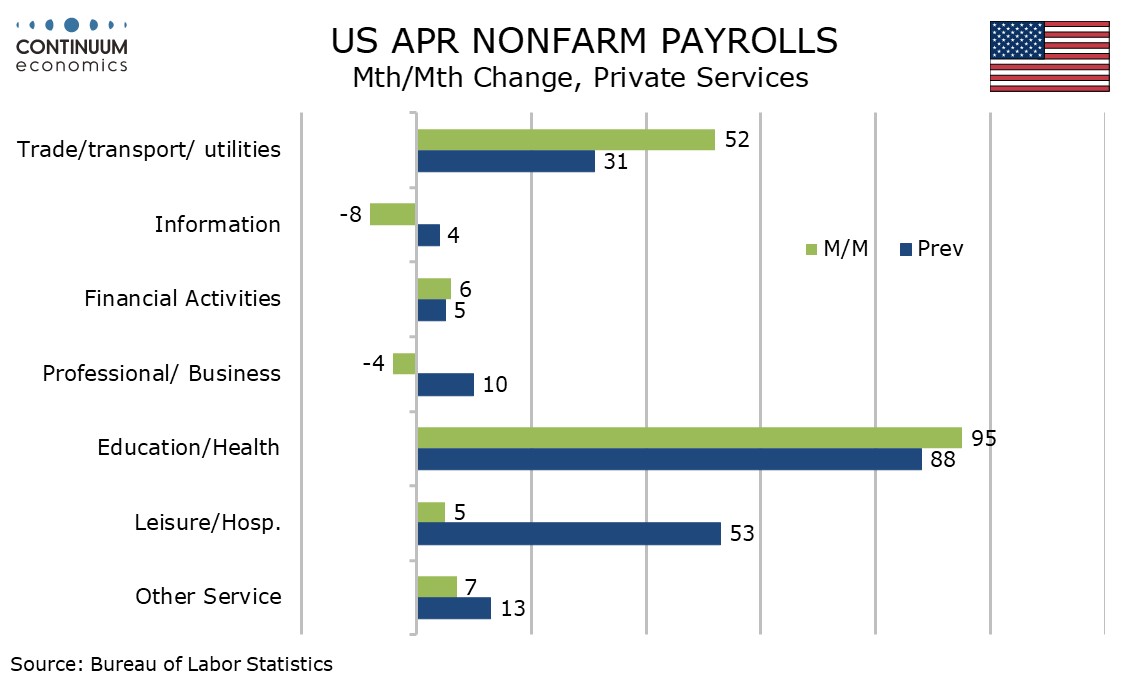

The April employment breakdown is very subdued outside a 87k increase in health care and social assistance, which maintained a strong trend, and an above trend 52k increase in trade, transport and utilities. Construction at 9k, leisure and hospitality at 7k and government at 8k have slowed from previously strong trends. Manufacturing’s 8k increase is however a marginal improvement from the preceding two months.

Seasonal adjustments are negative in the spring and the non-seasonally adjusted payroll increased by 803k. Seasonal adjustments are negative in May and June too. There may be a shortage of workers to full the usual seasonal labor demand, but a rise in unemployment and a slowing in average hourly earnings growth does not suggest so.

The household survey breakdown shows a small 87k increase in the labor force and an even smaller 25k rise in employment, leading to the higher unemployment rate.

Average hourly earnings rose by 0.20% before rounding and yr/yr growth at 3.9% from 4.1% is the slowest since June 2021. We had suspected a minimum wage hike for California fast wood workers would lift the data. The 0.2% rise overall came despite a 0.5% increase in leisure and hospitality.

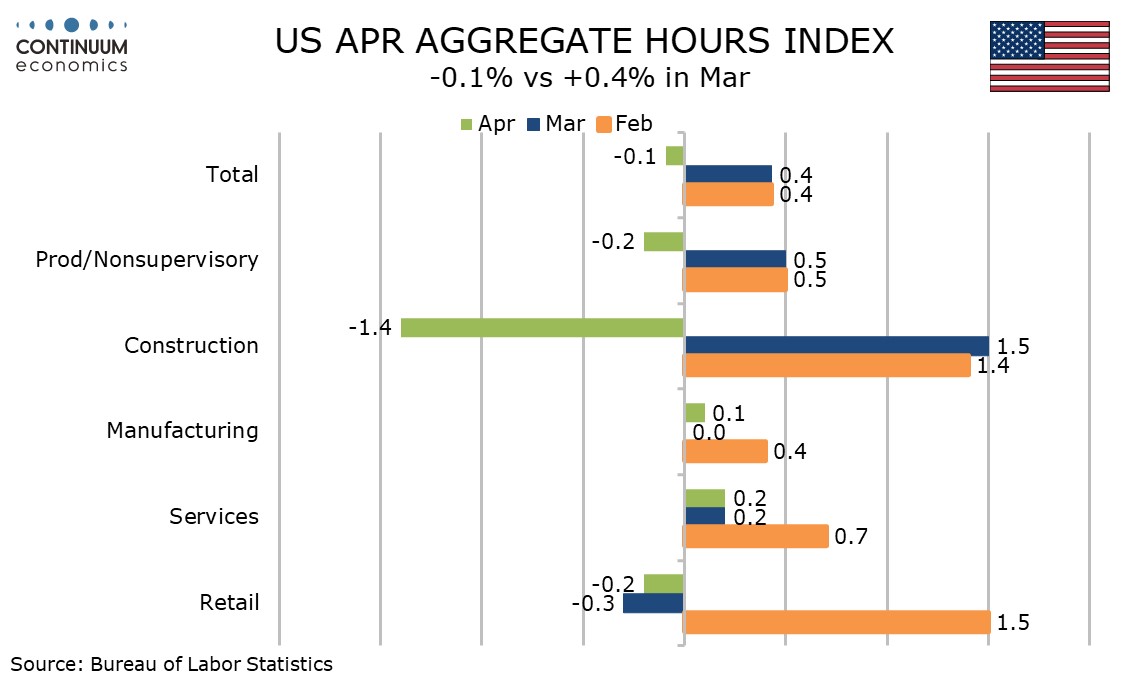

With the workweek slipping aggregate hours worked fell by 0.1% which means a weak start to Q2, though this might be a response to slower GDP growth in Q1. Mining and construction showed particularly steep falls in aggregate hours.

The Fed is not going to be in a rush to ease on this data but further slowing in payrolls could allow easing later in the year. The data also reinforces Powell’s Wednesday remarks that tightening is unlikely.