U.S. PCE Prices, Residual Seasonality and the Fed Outlook

Strength in Q1 inflation data contrasts the encouraging subdued data seen in the second half of 2023, and it looks likely there is some residual seasonality in the data even after seasonal adjustments. The underlying picture is still probably in a gradual downtrend, which should become clear later this year. We are not ready to adjust a view that the Fed will deliver three 25bps rate cuts in the second half of 2024.

Reconsidering our Core PCE Price Forecasts

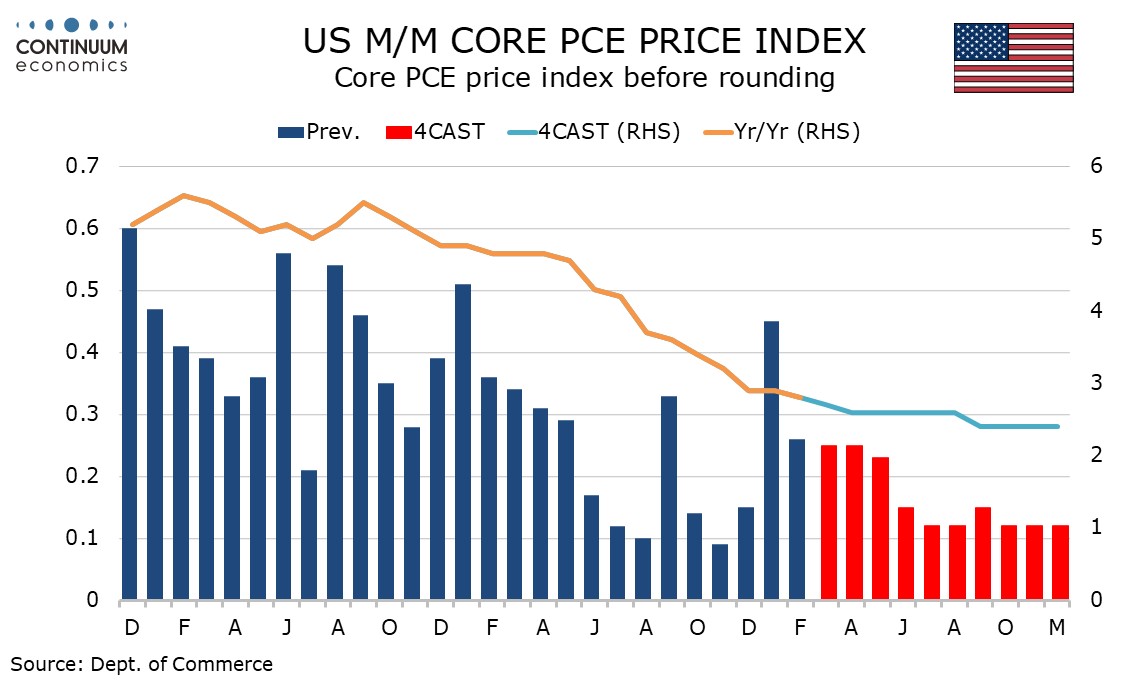

After two straight quarters in which annualized core PCE prices came in on the Fed’s 2.0% target, Q1 looks set to see an annualized gain close to 3.5%. This assumes March core PCE prices will look similar to February’s 0.26% increase, after March’s 0.36% core CPI rise matched February’s.

Yr/yr data is continuing to slow, with core PCE prices not having accelerated on a yr/yr basis since September 2022 reached 5.5%. The latest outcome, for February 2024, stood at 2.8%. March’s core CPI at 3.8% yr/yr matched February’s which was the lowest since May 2021, though March was slightly stronger than February before rounding. Fed minutes from the March 20 meeting considered residual seasonality as an explanation of the strength of January and February CPI data. Unless yr/yr growth shows renewed acceleration, this will remain a plausible explanation for disappointing monthly data.

In 2023 core PCE prices rose by 0.51% in January, 0.36% in February, 0.34% in March, 0.31% in Aril and 0.29% in May. After that only September’s 0.33% reached 0.2% before rounding. In 2024 we saw a 0.45% rise in January and a 0.26% rise in February. We expect slightly slower data in March, April and May, and significantly slower data in the remainder of the year.

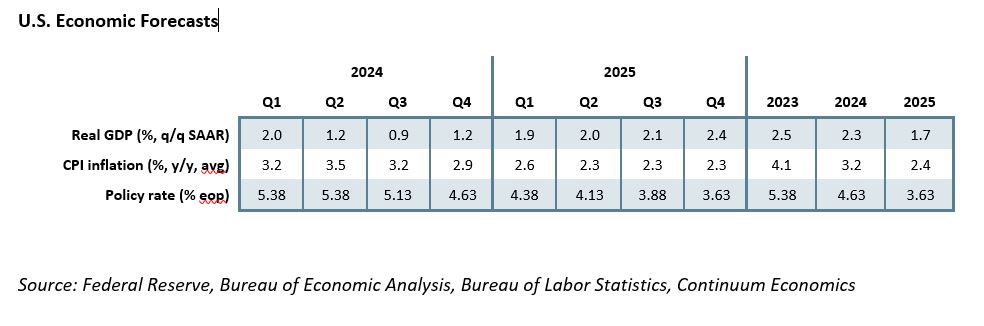

We expect annualized gains of 3.4% in Q1, 2.9% in Q2, 1.7% in Q3 and 1.5% in Q4, all below their respective 2023 gains of 5.0%, 3.7%, 2.0% and 2.0%. This would leave yr/yr growth at 2.4% in Q4 2024, still above the 2.0% target but not by much. This is higher than a 2.2% forecast we made in March but is below the FOMC's median 2.6% forecast made after March’s meeting. We continue to expect core PCE prices to reach the 2.0% target on a yr/yr basis in mid-2025, something the Fed does not project until 2026.

There are reasons for the start of the year having greater upside inflationary risk. January data reflects decisions taken at the start of the year, and is the month of greatest upside risk, but subsequent months coincide with a usual spring pickup in activity. In the early 1990s there was a recognition of the first four months of the year being a season for strong inflationary data, but as inflation became reliably subdued this phenomenon faded. That we are seeing strength in the New Year means underling inflationary pressures are still above target, but not as strongly as the data for those months suggest.

No major adjustments to our GDP or Fed views yet

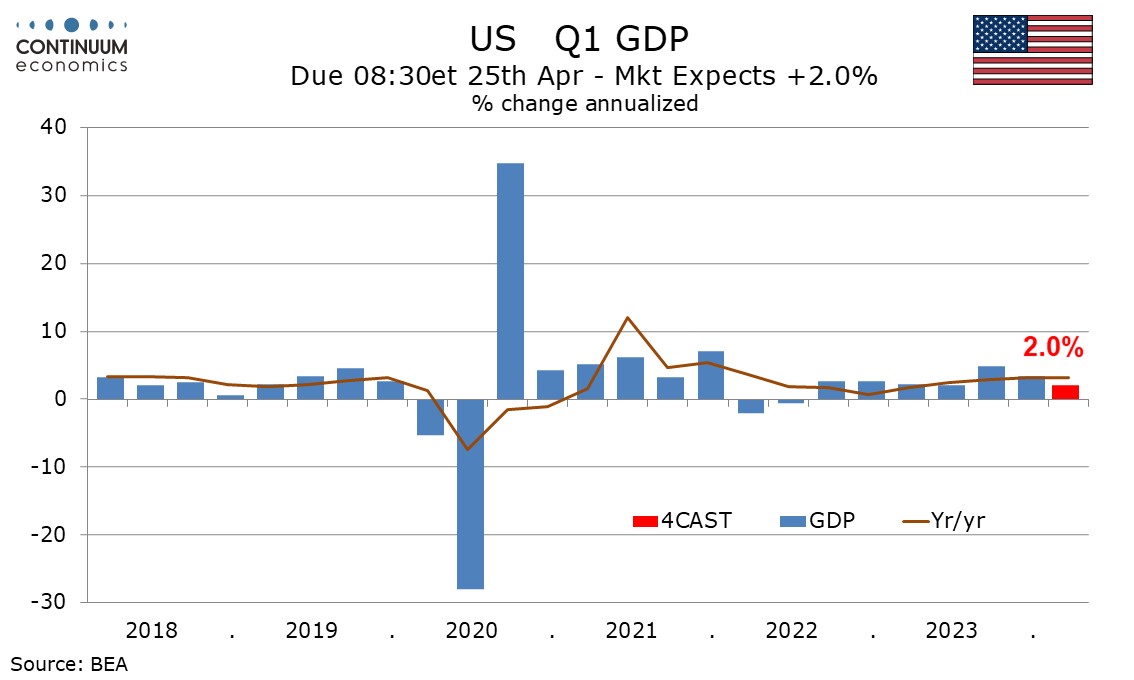

While we have been surprised on the upside by recent inflation data, Q1 GDP appears to be coming in close to a 2.4% annualized forecast we made in our March outlook. We stick to a view of some further slowing, though risk is on the upside of our 1.2% annualized Q2 forecast, with little sign of a loss of momentum at the end of Q1. Still, higher than expected inflation and prospects of Fed easing being delayed are downside risks to activity.

Our March outlook projected one 25bps Fed easing in Q3 and two 25bps cuts in Q4. We saw the Q3 move as slightly more likely in July than September, though now we see September as slightly more likely than July. We suggested a June easing was possible if March, April and May inflation data all came in subdued, but that is no longer possible after the March CPI. A July easing is still possible if April, May and June all come in subdued and job growth starts to slow. By September’s FOMC meeting we will have July and August CPI data too, and we expect by then early year inflationary strength will have clearly faded.

Two 25bps easings in Q4 will likely require rising unemployment as well as soft inflationary data, but that is consistent with our GDP view. We stick with a view for two rate cuts in Q4, though risk is for less than more. Still, it does not appear appropriate to significantly revise views for Fed policy late in the year in what was a marginal upside March CPI surprise, rising by 0.36% before rounding compared to a 0.3% consensus.