View:

August 29, 2025

Preview: Due September 16 - Canada August CPI - Higher as year ago weakness drops out

August 29, 2025 7:15 PM UTC

Weakness a year ago is likely to see August Canadian CPI picking up on a yr/yr basis, we expect to 2.0% from 1.7%. The Bank of Canada’s core rates are likely to remain fairly stable, and above the 2.0% target.

Preview: Due September 4 - U.S. July Trade Balance - Deficit to rise as imports from China rebound

August 29, 2025 4:24 PM UTC

We expect a July goods trade deficit of $79.2bn, up from $60.2bn in June. The deficit will compare to a Q2 average of $64.0bn but remain well below Q1’s pre-tariff average of $130.2bn. It will be similar to where trend was before the November election result signaled higher tariffs were coming.

U.S. August Final Michigan CSI - Inflation expectations revised down

August 29, 2025 2:12 PM UTC

August’s final Michigan CSI of 58.2 is not much changed from the preliminary 58.6 but a little further off July’s 61.7. There are some surprises in the detail however, in particular a downward revision to the 5-10 year inflation view.

Preview: Due September 2 - U.S. August ISM Manufacturing - Back to neutral with firmer prices

August 29, 2025 1:52 PM UTC

We expect August’s ISM manufacturing index to rise to a neutral 50.0 more than fully reversing a dip to 48.0 in July from 49.0 in June. This would be the strongest reading since January and February edged above neutral for the first time since October 2022.

Canada Q2 GDP falls as exports plunge outweighs stronger domestic demand

August 29, 2025 1:34 PM UTC

Canada’s 1.6% annualized decline in Q2 GDP is weaker than the market expected, though in line with a -1.5% Bank of Canada forecast. Details are mixed with domestic demand positive and the GDP decline due to a plunge in exports due to US tariffs. June GDP was weaker than expected with a 0.1% declin

U.S. July Personal Income and Spending and Core PCE Prices as expected, but Advance Goods Trade Deficit up as imports rebound

August 29, 2025 12:58 PM UTC

July’s personal income and spending report is in line with expectations, with the 0.3% core PCE price index matching the core CPI, and gains of 0.4% in income and 0.5% in spending also as expected. However a rise in the July advance goods trade deficit to $103.6bn from $84.9bn is unexpected, and l

German HICP Review: Headline Back Higher But EZ Price Picture Still Reassuring?

August 29, 2025 12:12 PM UTC

Germany’s disinflation process hit a slightly more-than-expected hurdle in August, as the HICP measure rose 0.3 ppt from July’s 1.8% y/y, that having been a 10-mth low (Figure 1). This occurred largely due to energy base effects with food prices also contributing slightly. The result was that

August 28, 2025

Preview: Due September 10 - U.S. August PPI - A moderate gain after a surge in July

August 28, 2025 6:13 PM UTC

We expect August PPI to rise by 0.3% overall and 0.2% ex food and energy, moderate gains after shocking surges of 0.9% in each series in July, which broke a string of mostly subdued outcomes from February through June. Ex food, energy and trade, we expect a 0.3% increase to follow a 0.6% rise in Jul

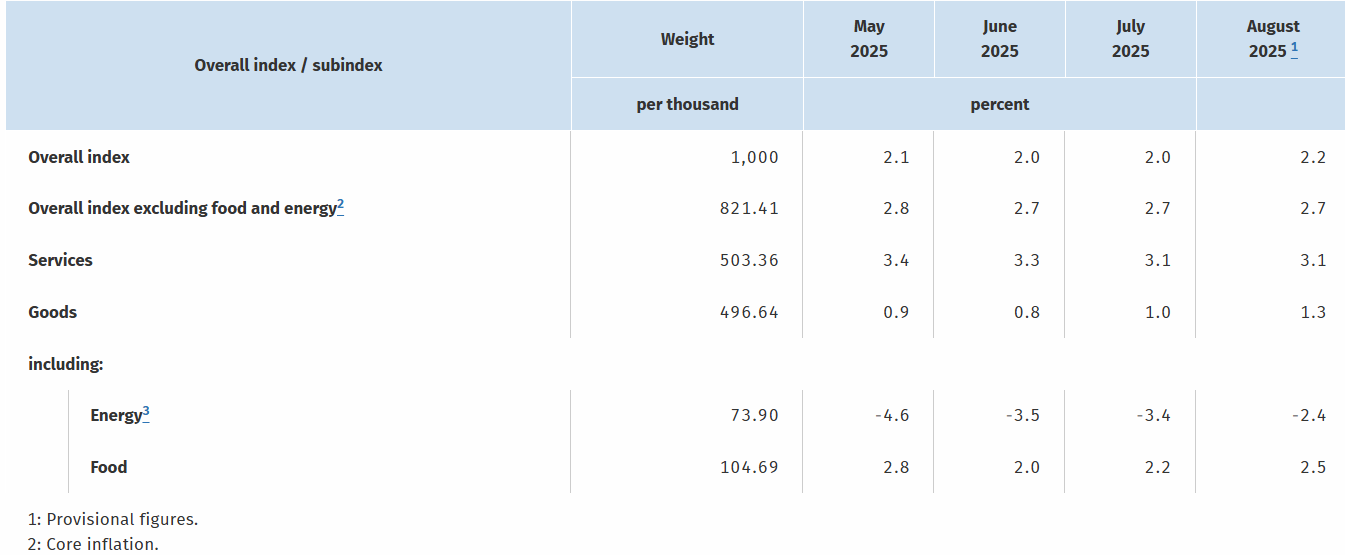

Preview: Due September 11 - U.S. August CPI - Tariff impact slowly building

August 28, 2025 5:19 PM UTC

We expect August CPI to increase by 0.4% overall and by 0.3% ex food and energy, with the respective gains before rounding being 0.37% and 0.31%. This would be the second straight gains slightly above 0.3% in the core rate with the impact of tariffs starting to escalate.

Preview: Due August 29 - Canada Q2/June GDP - Exports plunge to send GDP lower

August 28, 2025 2:17 PM UTC

We expect Q2 Canadian GDP to fall by 1.0% annualized after five straight gains marginally above 2.0%. This would be slightly stronger than a Bank of Canada forecast of -1.5% but weaker than what monthly GDP data is likely to imply for the quarter, with June seen rising by 0.1%.

Preview: Due August 29 - U.S. July Advance Goods Trade Balance - Deficit to rise as imports from China rebound

August 28, 2025 1:50 PM UTC

We expect an advance July goods trade deficit of $99.8bn, up from $84.9bn in June but still closer to the Q2 average of $89.0bn than the Q1 average of $155.0bn when imports surged ahead of tariffs.

Preview: Due August 29 - U.S. July Personal Income and Spending - Core PCE Prices to match Core CPI

August 28, 2025 1:35 PM UTC

We expect PCE price data to match the July CPI, with a 0.3% rise in the core rate and a 0.2% increase overall. We expect both personal income and spending to rise by 0.5%, ahead of prices.

August 27, 2025

Preview: Due September 4 - U.S. August ADP Employment - Slower than July which corrected a June decline

August 27, 2025 3:39 PM UTC

We expect a rise of 60k in August’s ADP estimate for private sector employment growth. This would be a slowing from 104k in July which outperformed the non-farm payroll, with July’s improved data looking in part corrective from a 23k decline in June.

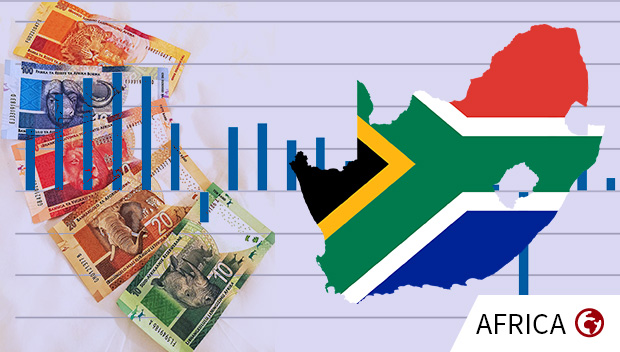

South Africa GDP Growth Preview: Moderate Growth Will Resume in Q2

August 27, 2025 3:22 PM UTC

Bottom line: Department of Statistics of South Africa (Stats SA) will announce Q2 GDP growth on September 3, and we expect that South African economy will likely grow by around 1.0%-1.2% YoY in Q2 2025. We think that the growth momentum will continue to be supported by low inflation and interest rat

Preview: Due August 28 - U.S. Preliminary (Second) Estimate Q2 GDP - Upward revision on retail and construction

August 27, 2025 2:33 PM UTC

We expect the second (preliminary) estimate of Q2 GDP to be revised up to 3.2% from the first (advance) estimate of 3.0%. The rise should be seen alongside a 0.5% decline in Q1 given recent extreme volatility in net exports.

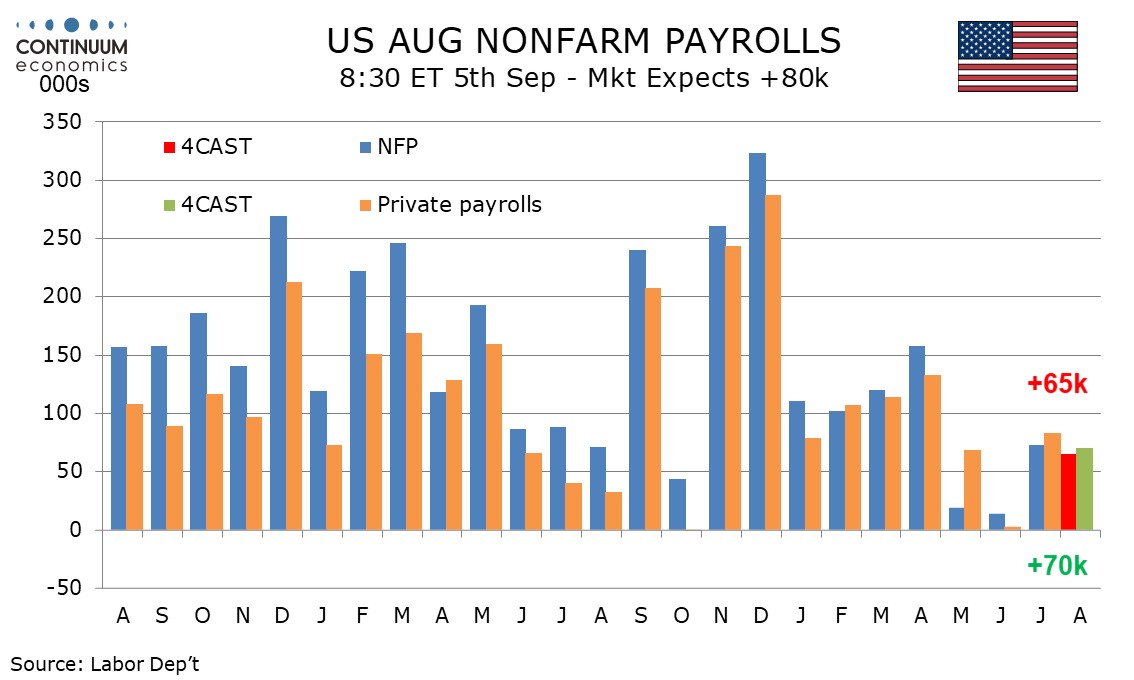

Preview: Due September 5 - U.S. August Employment (Non-Farm Payrolls) - Similar to July's, still not recessionary

August 27, 2025 2:20 PM UTC

We expect August’s non-farm payroll to look similar to July’s, with a rise of 65k versus 73k in July, above the 14k rise of June and the 19k rise of May but well below the trend that was running above 100k through April. We also expect unemployment to remain at July’s 4.2% rate and a second st

August 26, 2025

Turkiye GDP Growth Preview: Slowdown Will Continue in Q2

August 26, 2025 5:14 PM UTC

Bottom Line: Turkish Statistical Institute (TUIK) will announce Q2 GDP growth on September 1 and we expect that Turkish economy will expand around 1.7% -2.0% YoY backed by private consumption despite early indicators demonstrate a lower acceleration rate in domestic demand amid tightening financial

Preview: Due September 2 - U.S. August ISM Manufacturing - Back to neutral with firmer prices

August 26, 2025 4:59 PM UTC

We expect August’s ISM manufacturing index to rise to a neutral 50.0 more than fully reversing a dip to 48.0 in July from 49.0 in June. This would be the strongest reading since January and February edged above neutral for the first time since October 2022.

U.S. August Consumer Confidence resilient but worries on jobs and prices increase

August 26, 2025 2:19 PM UTC

August’s Conference Board’s Consumer Confidence Index has held up a little better than expected, particularly given a weaker preliminary August Michigan CSI, falling to 97.2 from 98.7 only because July as revised up from 97.2. There has not been much change in the index in the last four month

U.S. July Durable Goods Orders - Signs of underlying improvement

August 26, 2025 12:51 PM UTC

July durable goods orders with a 2.8% decline are less weak than expected given a strong 1.1% rise ex transport, where trend appears to be gaining some momentum. While manufacturing surveys are mixed August’s S and P manufacturing survey was stronger too.

EZ HICP and Jobs Review: Headline at Target as Services Inflation at Fresh Cycle-low

August 26, 2025 11:51 AM UTC

HICP, inflation – still at target – is very much a side issue for the ECB at present, albeit with the likes of oil prices and tariff retaliation and a low but far from authoritative jobless rate (Figure 3) possibly accentuating existing and looming Council divides. Regardless, despite adverse

August 25, 2025

U.S. July New Home Sales - Trend has little direction, prices weak

August 25, 2025 2:14 PM UTC

July new home sales at 652k are on the firm side of expectations and down 0.6% from June only because June was revised up to 656k from 627k, now up 4.1% rather than 0.6%. Trend still looks fairly stable and downside risks are fading as prospects of Fed easing increase.