Preview: Due March 8 - U.S. February Employment (Non-Farm Payrolls) - Slower but Labor Market Remains Strong

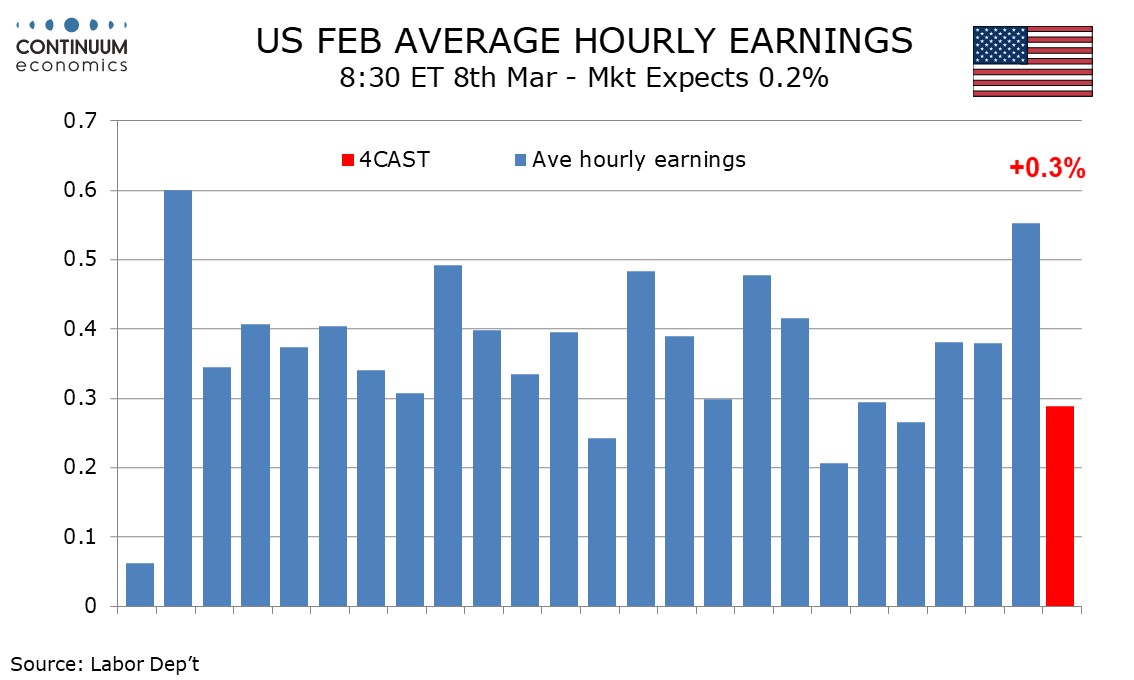

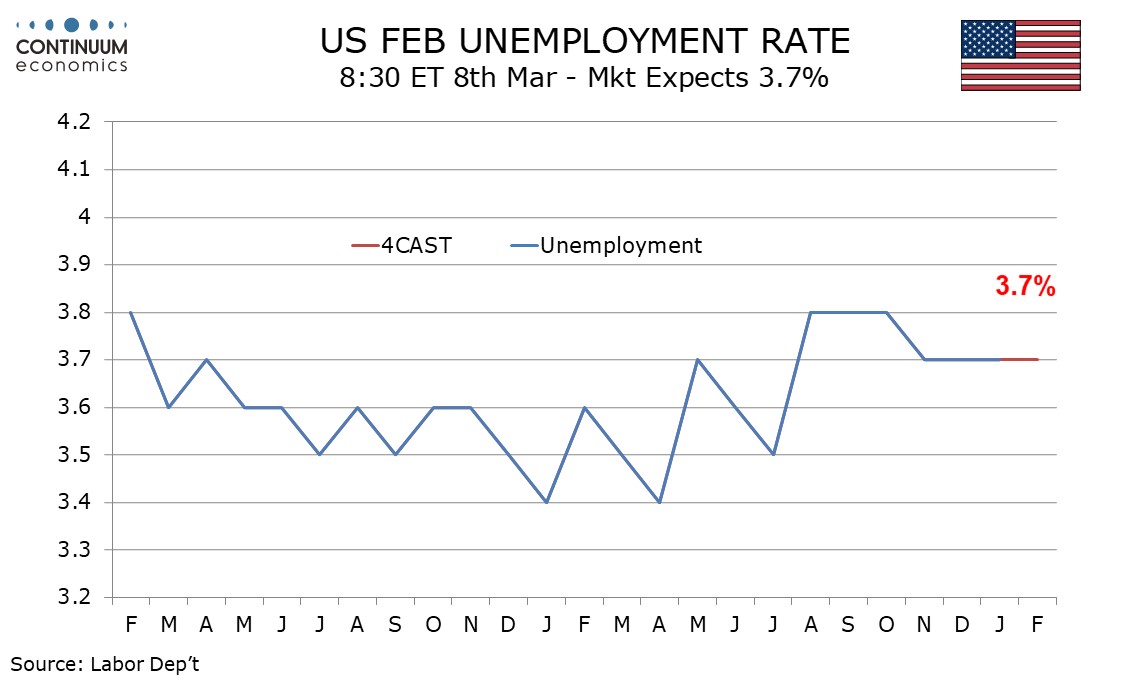

After two straight very strong non-farm payroll gains exceeding 300k we expect a 200k increase in February’s non-farm payroll, which is where trend was before the recent acceleration. We expect an unchanged unemployment rate of 3.7% to show the labor market remains tight, but average hourly earnings to slow to a 0.3% increase after an unusually strong 0.6% increase in January.

The economy’s recent acceleration may have been assisted by falling long term rates as hopes for Fed easing increased, and may now be starting to fade. Mild weather in December and supportive seasonal adjustments in January may also have flattered the last two months. Weather looks like a downside risk for February and its seasonal adjustments are moderately negative.

The initial and continued claims 4-week averages have moved a little higher after falling in January, though initial claims were very low in the February payroll survey week. The message from initial claims and several other indicators is that the labor are remains strong, but a bit less so than in January. We expect a 160k rise in private sector payrolls as government payrolls continue to see solid gains.

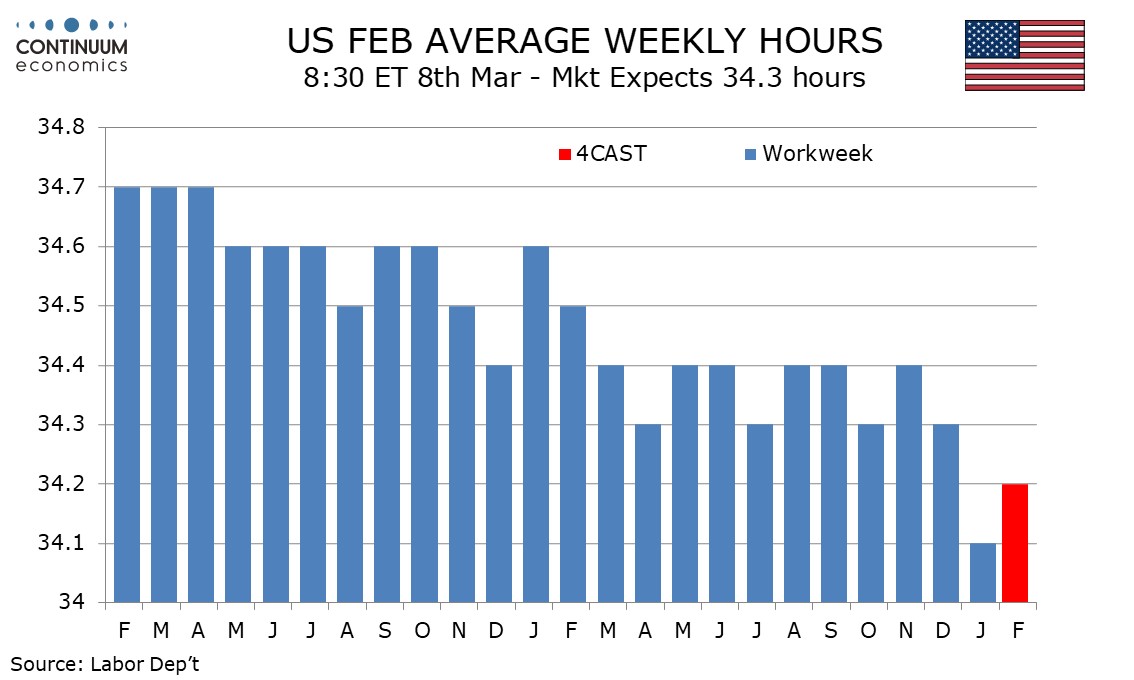

While January saw a strong gain in payrolls, aggregate hours worked slipped because of a sharp dip in the workweek to 34.1 for 34.3 hours. That may have been due to bad weather in the survey week and a correction looks likely in February. However February’s payroll survey week saw some bad weather too and we expect only a partial reversal of January’s dip, with a rise to 34.2 hours.

A 0.6% increase in January average hourly earnings, the strongest since March 2022, may have been in part due to the fall in the workweek and we expect a slightly below trend 0.3% increase in February. This would leave yr/yr growth unchanged at January’s 4-month high of 4.5%.

The strong gains in the last two non –farm payrolls have also been contrasted by the household survey, which calculates the unemployment rate, showing two straight declines in both the labor force and unemployment. We expect both to bounce in February, with the labor force seeing the slightly stronger rebound, though we expect the unemployment rate to remain at 3.7% for a fourth straight month. January’s rate was 3.66% before rounding, hinting that a fall is more likely than a rise.