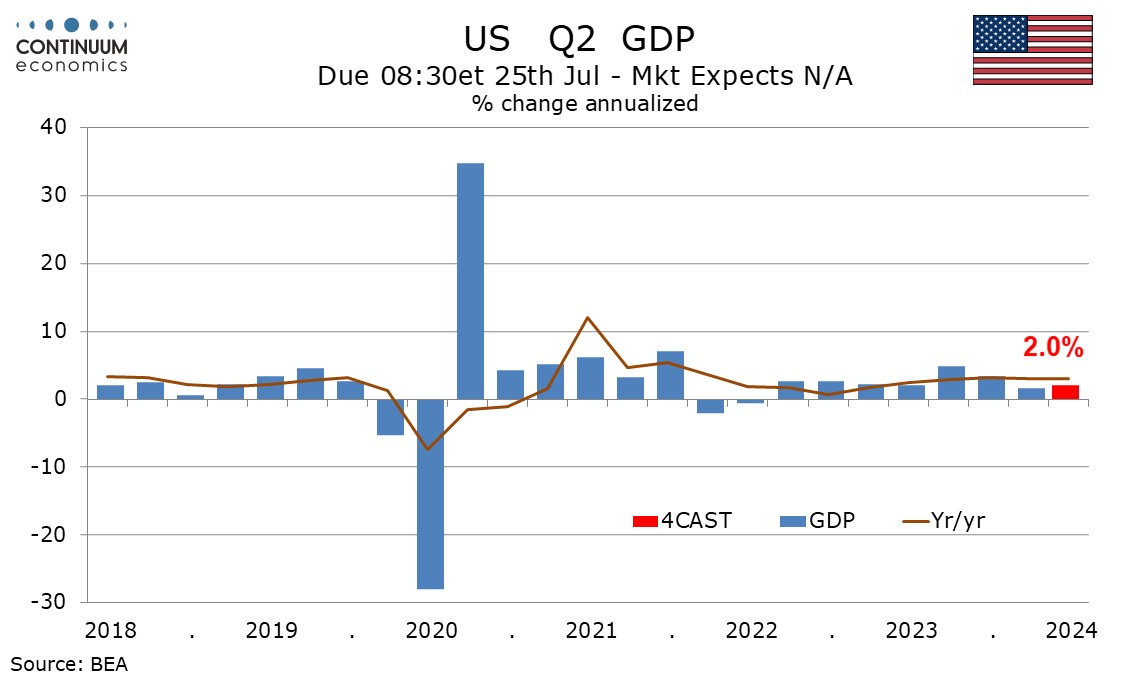

U.S. Q2 GDP to Increase by 2.0% Annualized Before Slowing In the Second Half

In our quarterly outlook on March 22 we looked for Q1 US GDP to rise by 2.4% annualized followed by growth of near 1.0% in the remaining three quarters. While Q1 at 1.6% came in weaker than expected details were constructive for Q2 for which we now expect a 2.0% annualized gain. We continue to expect growth of near 1.0% in the second half of the year. Our view for 2024 as a whole is not significantly changed.

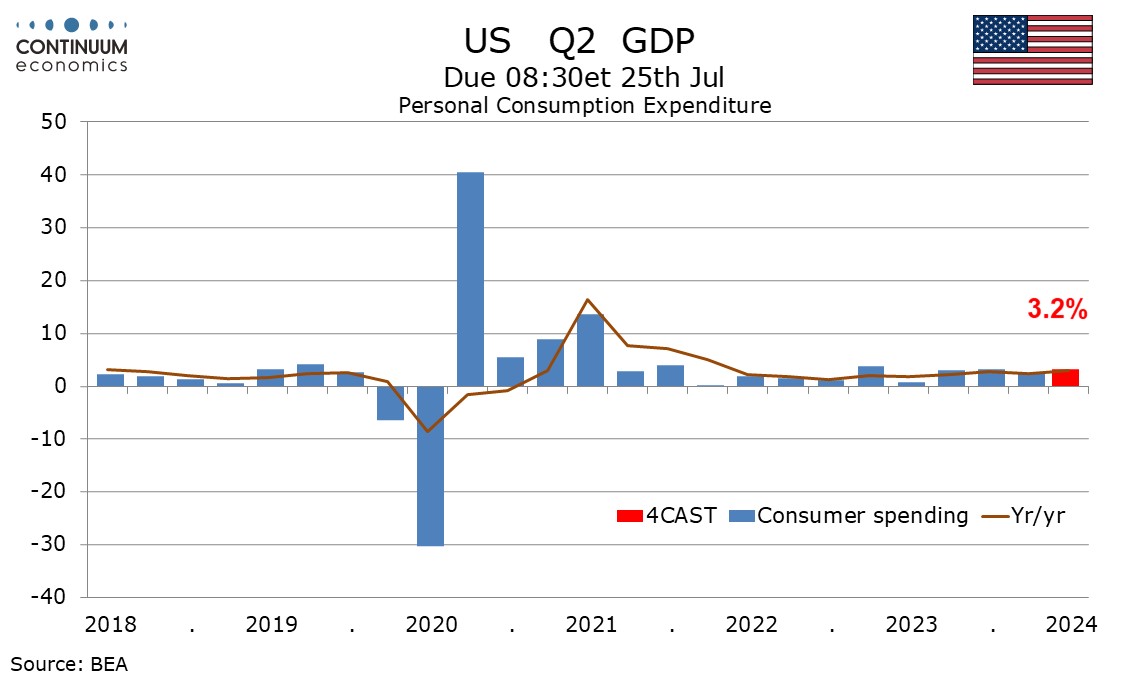

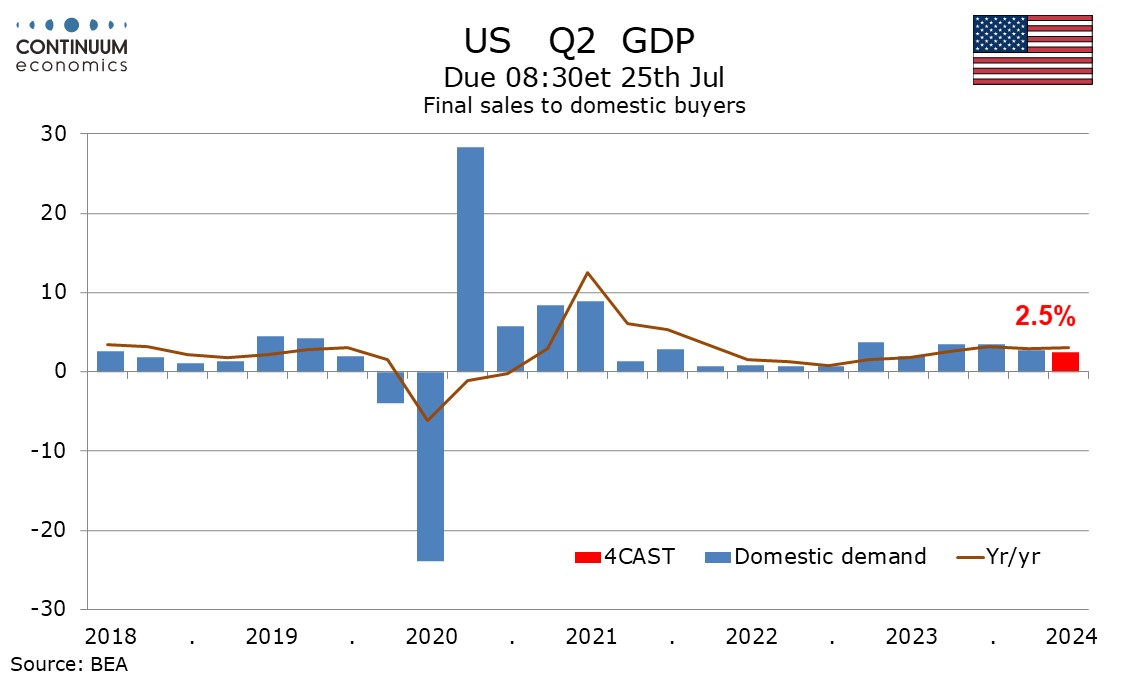

The Q1 GDP detail showed a healthy 2.8% increase in final sales to domestic buyers (GDP less inventories and net exports) with net exports taking 0.86% from GDP and inventories taking of 0.35%. Consumer spending rose by 2.5% despite a weak January that was depressed by weather. With the Q1 average depressed by January data Q2 is starting on a firmer level.

We expect consumer spending to increase by 3.2% in Q2, despite monthly increases in each month likely to be considerably slower than these of February and March, and this leaving a loss of momentum entering Q3. Consumer spending has significantly outperformed real disposable income, which increased by only 1.1% in Q1, for three straight quarters. With savings built up during the pandemic close to exhausted, this will be difficult to sustain, particularly if employment growth loses momentum.

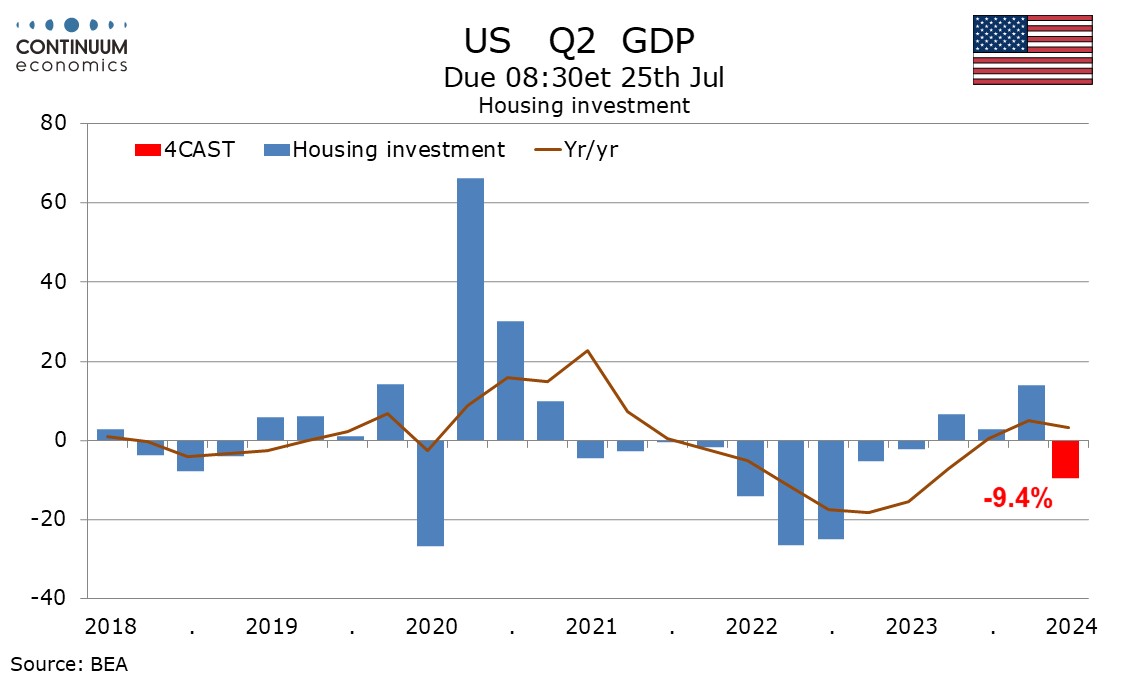

Despite seeing a stronger Q2 from the consumer, we expect a marginal slowing in final sales to domestic buyers to a 2.5% pace. The main contrast from Q1 is that we expect housing investment to fall by 9.4% after a 13.9% Q1 increase. Q1’s increase was supported by falling mortgage rates in Q4. Q2 is likely to be restrained by rising mortgage rates in Q1.

With the Q2 Senior Loan Officer Opinion Survey on bank lending practices sustaining an improved tone seen in Q1 we expect business investment to rise by 3.1% in Q2 after a 2.9% increase in Q1 while we expect government at 1.7% to also see a modest improvement from Q1’s 1.2%, though this will remain significantly lower than in each quarter of 2023.

We expect a neutral contribution from inventories in Q2 with final sales (GDP less inventories) at 2.0% set to exactly match its Q1 pace. From net exports we expect a negative contribution of 0.4%. The trade deficit trended higher through Q1 signaling negative momentum in net exports entering Q2.

For core PCE prices we expect a 3.1% annualized increase in Q2, down from 3.7% in Q1 but above the 2.0% paces seen in Q3 and Q4 of 2002. With 2023 having seen gains of 5.0% in Q1 and 3.7% in Q2 progress is still being made on a yr/yr basis and we expect 2024 will also see softer core PCE price data in the second half of the year.