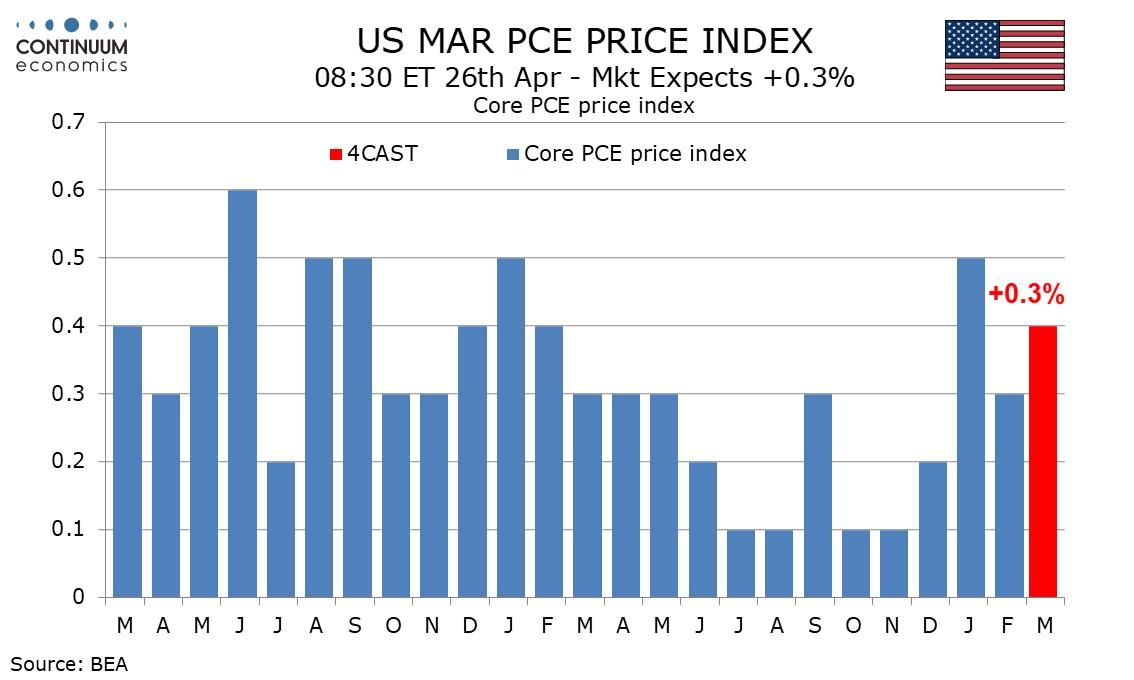

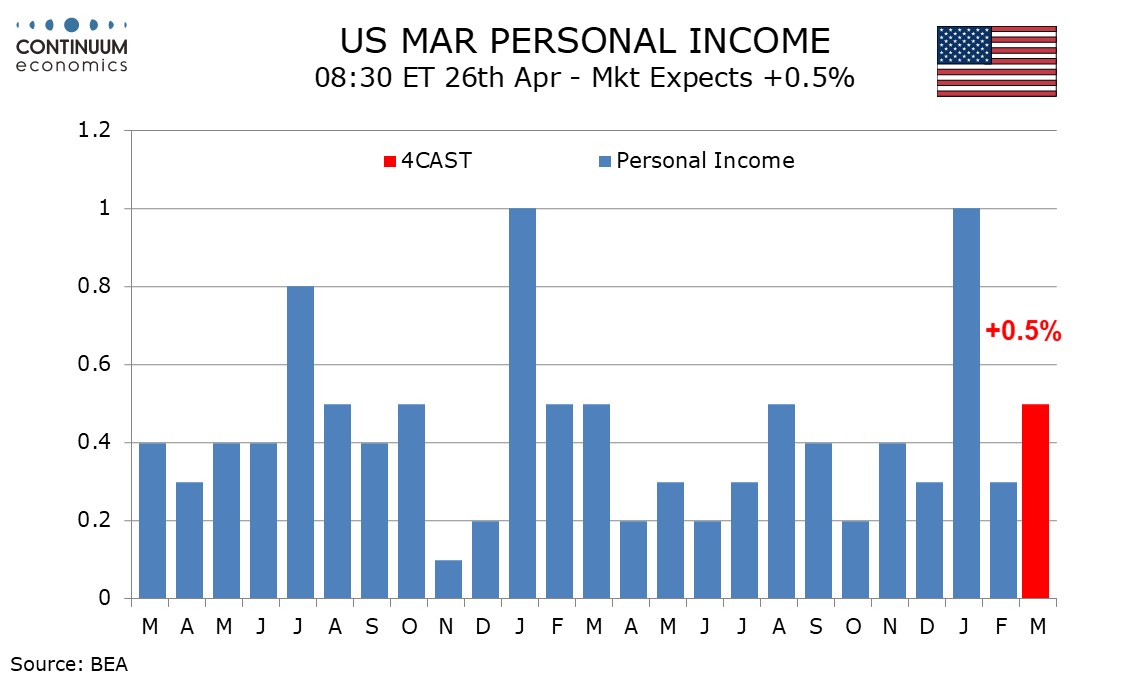

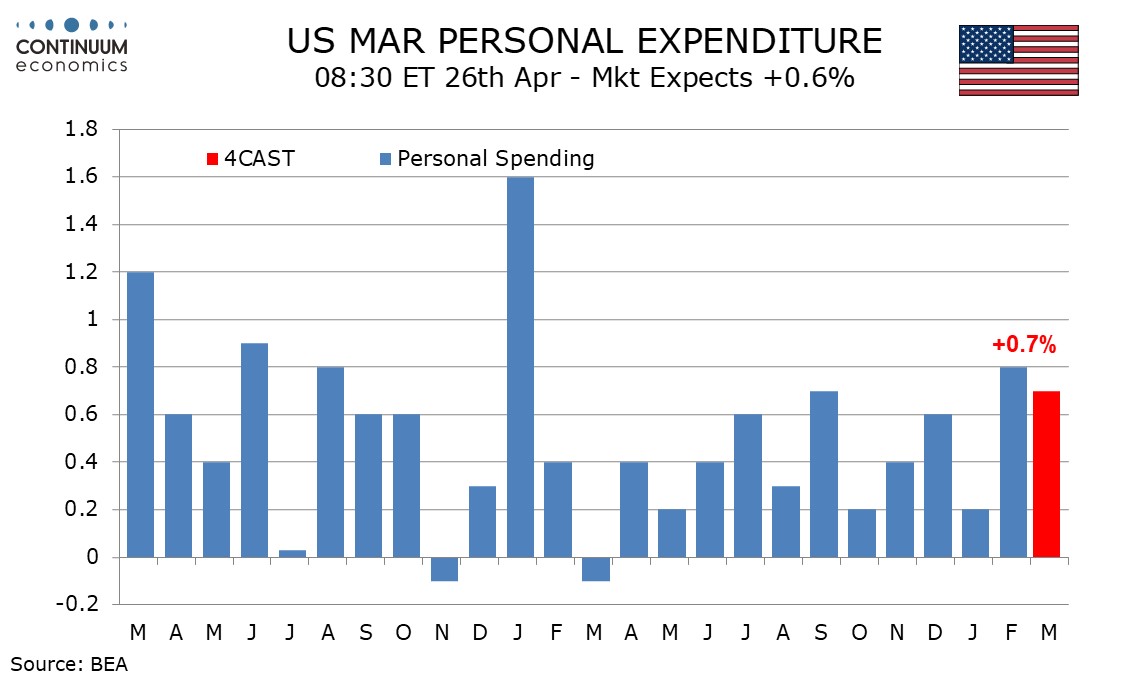

Preview: Due April 26 - U.S. March Personal Income and Spending - Upside risk in Core PCE prices given Q1 outcome

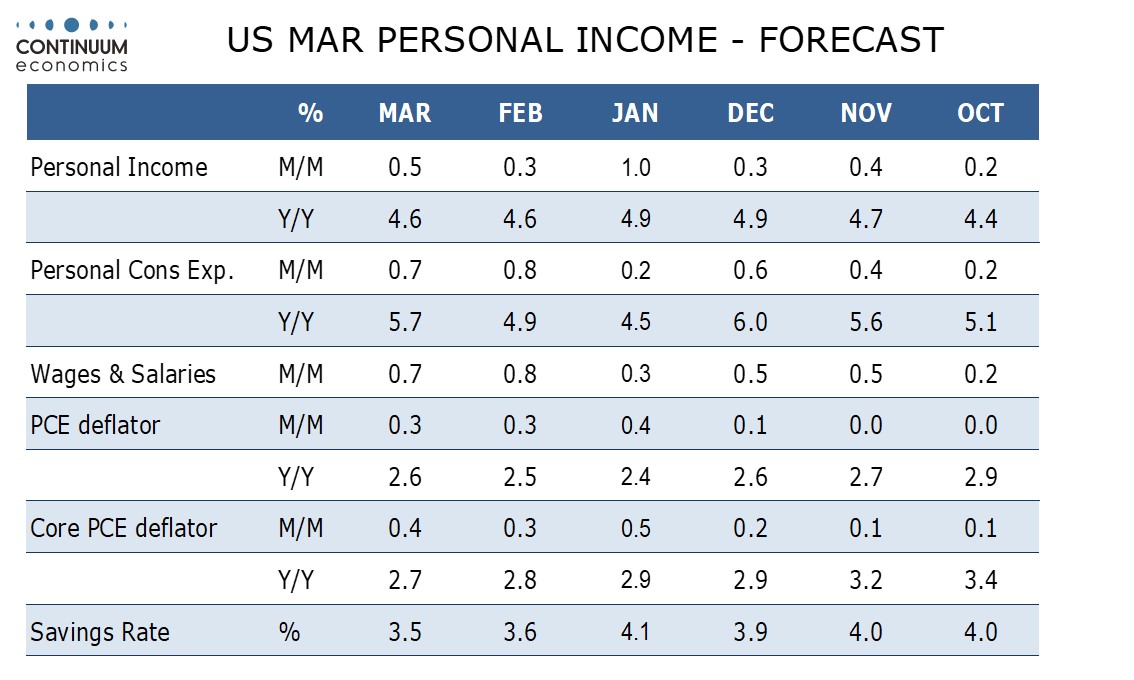

March personal income and spending data will be largely old news as we have already seen Q1 totals in the GDP report. The GDP details are consistent with gains of 0.6% in personal income, 0.8% in personal spending and 0.4% in core PCE prices, all 0.1% above our pre-GDP forecasts of 0.5%, 0.7% and 0.3% respectively. Our forecasts could still prove accurate if back month data sees upward revisions.

Before the GDP data we had expected the core PCE price index to come in below 0.3% before rounding, similar to a 0.26% increase seen in February. That now looks unlikely. A 0.35% increase with no back month revisions would deliver a 3.6% annualized increase in Q1, slightly below the actual outcome of 3.7%. However, a March outcome rounded down to 0.3% would require only modest upward revisions to February and/or January.

We expect overall PCE prices to see a similar rise to the core rate. CPI saw both the headline and core rates rounded up to 0.4% in March. Q1 data saw yr/yr growth slip to 2.9% from 3.2% for core PCE prices while overall PCE prices fell to 2.6% from 2.8% in Q4.

Our 0.5% forecast for personal income growth assumed a 0.7% increase in wages and salaries, as implied by a payroll breakdown which saw strong employment growth and a rise in the workweek as well as a moderate 0.3% rise in average hourly earnings. For the other components we expect a return to trend after February corrected a very strong increase in January, which was inflated by New Year Social Security cost of living adjustments and dividend payments. The GDP data implies a 0.6% rise in personal income and a 0.8% rise in wages and salaries, meaning our forecast would require only modest upward back month revisions.

Retail sales increased by 0.7% in March and we expected a similar rise from services. We expected upward revisions to retail data given revisions with March’s retail sales report, so we do not expect March consumer spending to reach the 0.8% rise implied by the GDP report. In fact service consumption in the GDP detail, while strong, slightly underperformed our expectation. March personal spending data is more likely to fall short of our forecast than to beat it, though upward revisions will be needed for that to be the case.