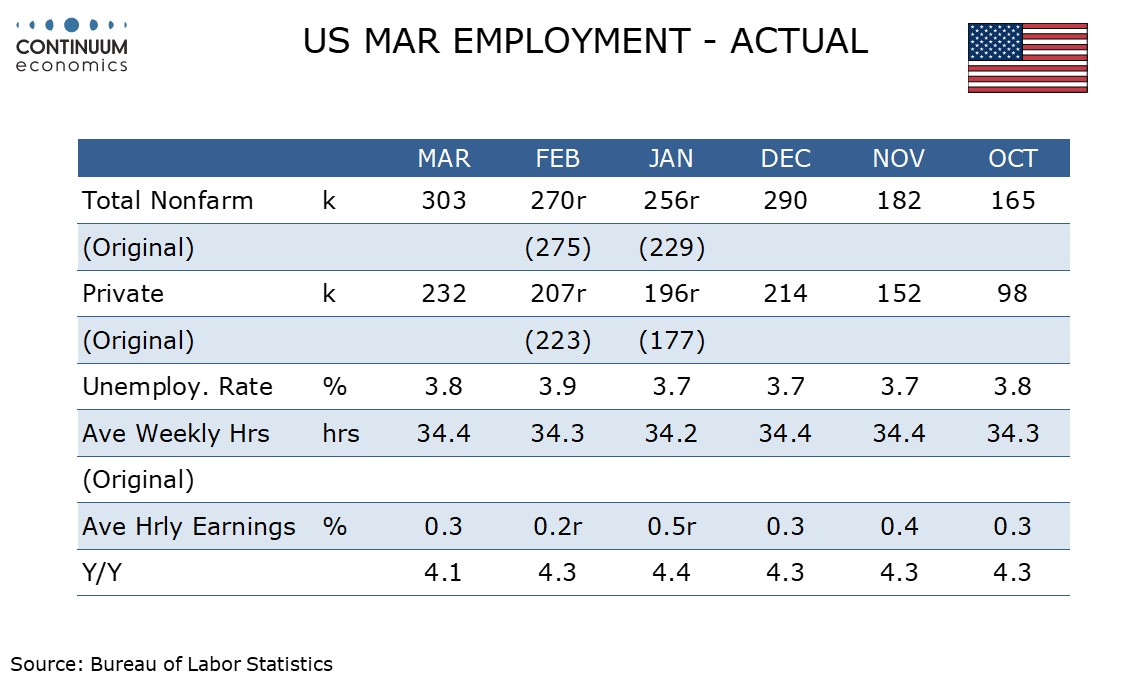

U.S. March Employment - On the strong side in all key details

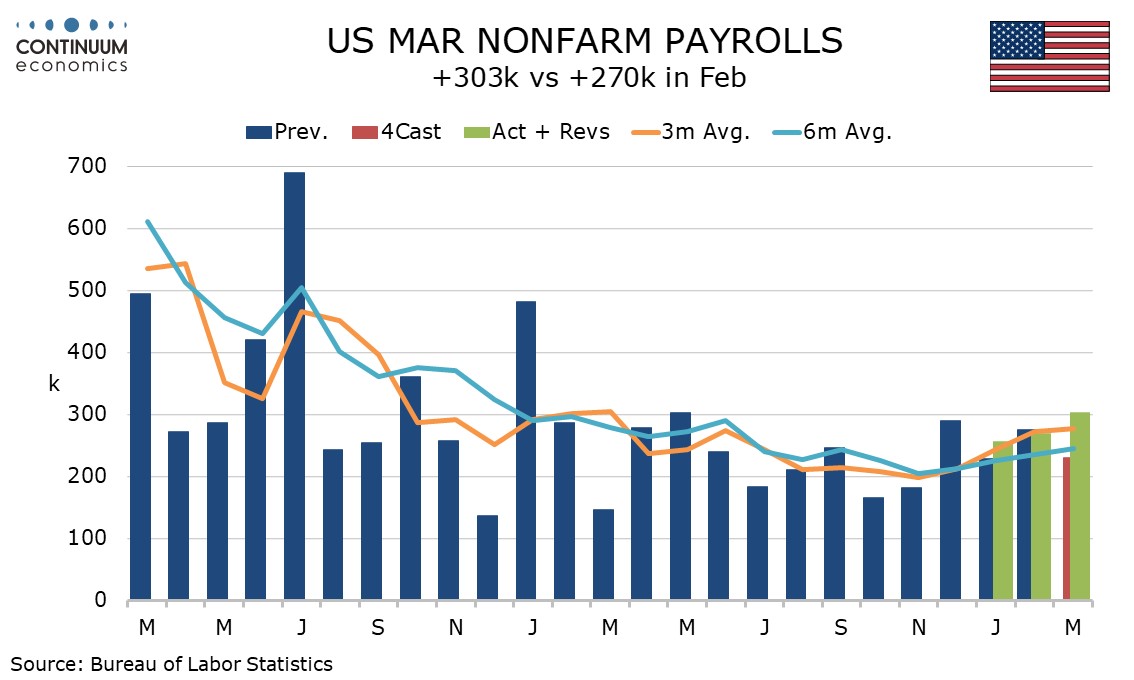

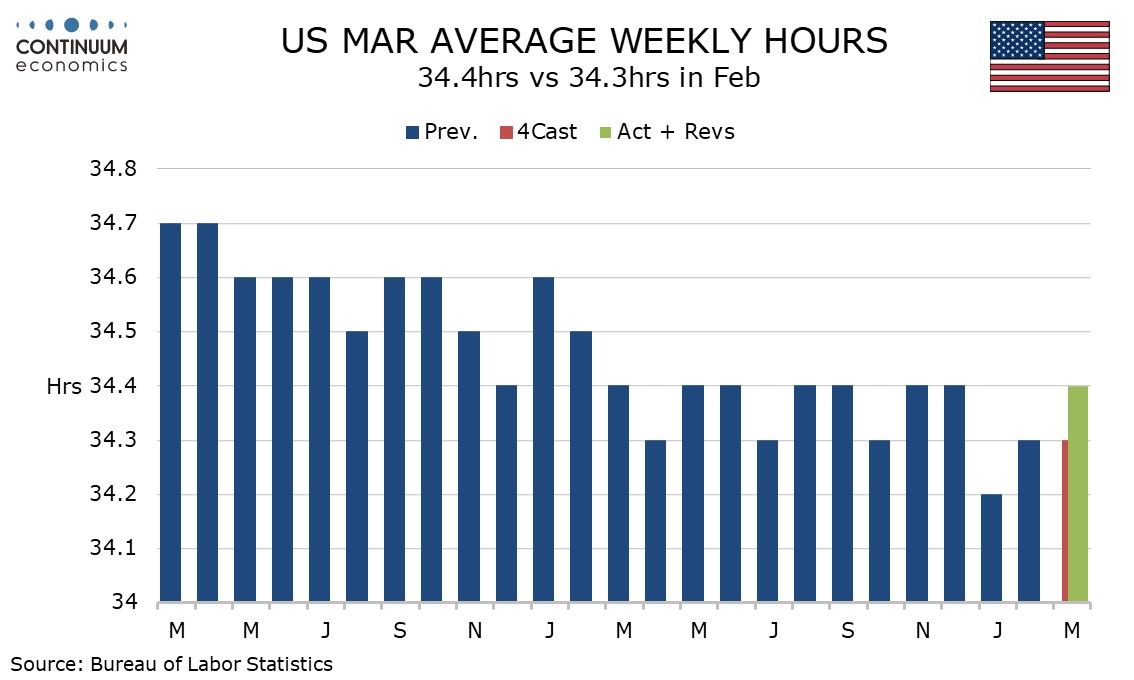

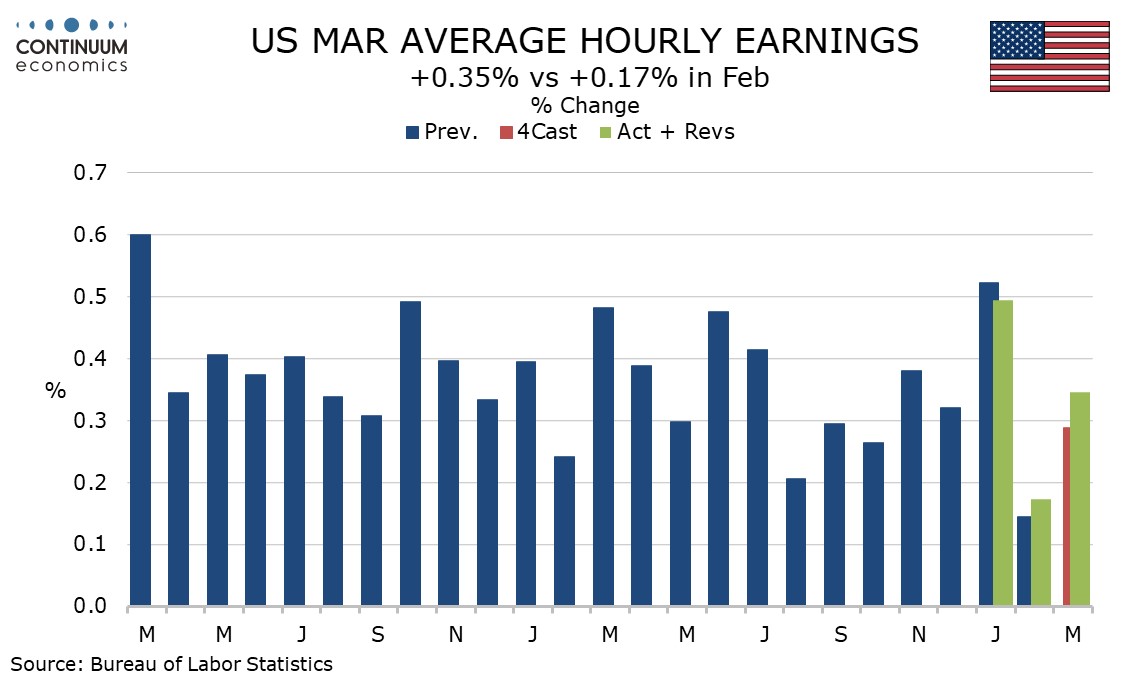

March’s non-farm payroll increase of 303k is clearly above expectations and maintains a strong pace though the private sector gain of 232k, while above consensus, is not quite as impressive. A rise in the workweek to 34.4 from 34.3 hours adds to a picture of positive activity while unemployment corrected lower to 3.8% from 3.9% while remaining above January’s 3.7%. Average hourly earnings rose by a consensus 0.3%, but by 0.347% before rounding, to complete a generally strong if not stunning report.

Revisions are modest if positive at a net 22k, with an upward revision to January outweighing a downward revision to February’s change. For the private sector revisions are minimal, a net positive of 3k. The data leaves four straight gains in excess of 250k and March’s gain is the strongest since a matching 303k gain in May 2023. The 3-month average of 276k is a 12-month high and the 6-month average of 244k is a 9-mongth high.

Government at 71k is the most obvious area of strength though education and health at 88k maintains a strong trend and leisure and hospitality at 49k saw a strong month. Construction at 39k saw its strongest month since May 2022 while manufacturing was unchanged. Private services at 190k matched February’s gain while goods were above trend at 42k, led by construction.

The workweek at 34.4 hours is a return to the levels of November and December after a weather-induced dip to 34.2 in January and a partial recovery to 34.3 in February. This leaves aggregate hours worked up by 0.5% on the month and 1.0% annualized in Q1, the latter down from 1.4% in Q4 and 1.5% in Q3, both quarters in which GDP was strong. This suggests respectable if slower GDP growth in Q1 even with January’s bad weather and importantly, solid momentum entering Q2.

A 0.347% rise in average hourly earnings marks a return to trend after a strong January was followed by a below trend February. Revisions were minimal, with February now at 0.174% rather than 0.145%, even if now rounding to 0.2% rather than 0.1%, while January while still rounding to 0.5% in now 0.495% rather than 0.524%. Yr/yr growth slowed to 4.1% from 4.3% as expected, to its slowest pace since June 2021.

The household survey, which calculates the unemployment rate, unusually showed stronger employment growth, of 498k, than did the non-farm payroll. While labor force growth of 469k almost matched the former, the difference was just enough to allow the unemployment rate to correct lower to 3.8% from 3.9%, the actual change being to 3.83% from 3.86%. The rate remains above the 3.7% was saw in the 3 months to January and further above the April 2023 low of 3.4%, but the labor market remains tight. There remains no urgency to ease monetary policy even if inflationary pressures are gradually fading.