U.S. February Core PCE prices provide some relief, Spending outpaces Income

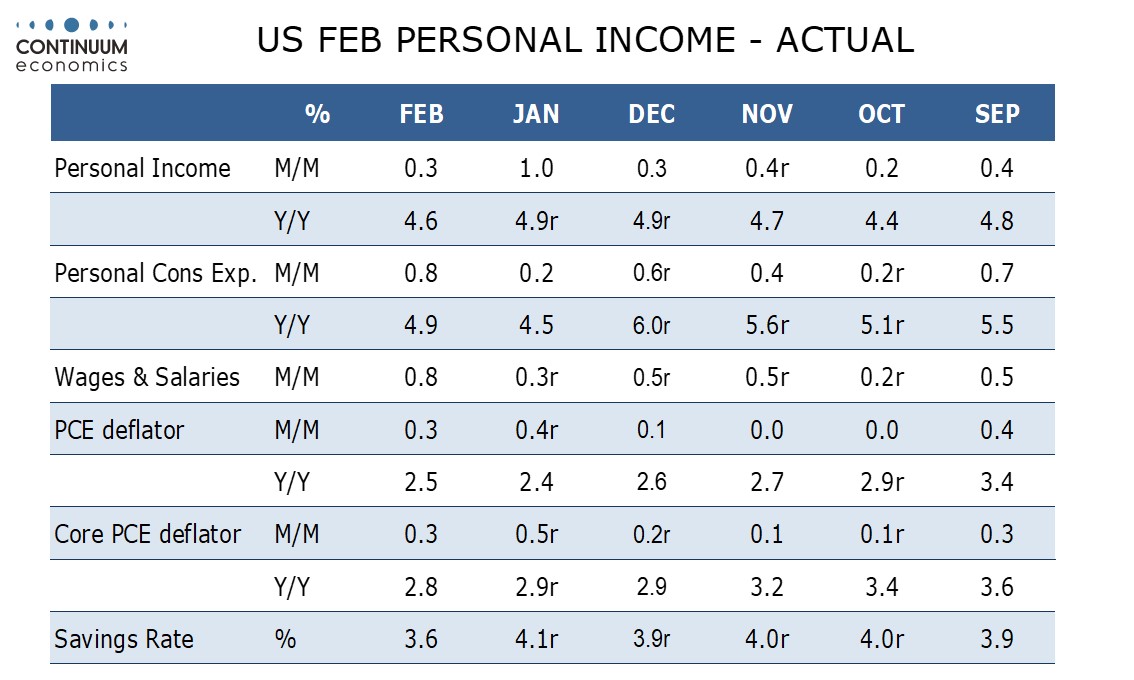

February’s PCE price data comes as a relief, with a consensus 0.3% core rate up only 0.2615% before rounding, well below a core CPI that was rounded up to 0.4%, while the 0.3% headline (0.333% before rounding) is below consensus, after a strong CPI gain that was rounded down to 0.4%.

While February data may be below consensus January’s core PCE price index was revised up to 0.5% from 0.4% (marginally before rounding) and its headline revised up to 0.4% from 0.3%, though it should be remembered that Q4 core PCE prices were revised down to 2.0% annualized from 2.1% with the GDP revision. Yr/yr data came in on consensus, the core rate at 2.8% from an upwardly revised 2.9%, and the overall pace at 2.5% from an unrevised 2.4%.

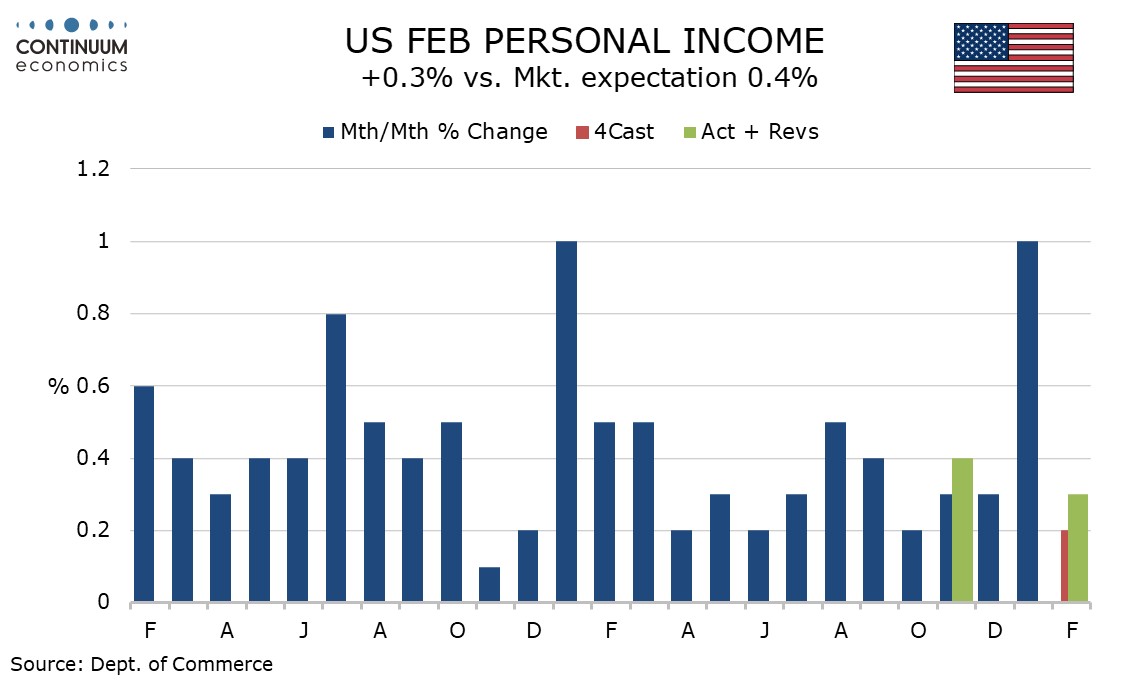

Personal income with a 0.3% rise was weaker than expected despite a strong 0.8% rise in wages and salaries, as the other components of personal income corrected from a strong January. Dividends reversed a sharp January rise but government benefits saw a slightly above trend gain after a very strong January when Social Security benefited from annual cost of living adjustments.

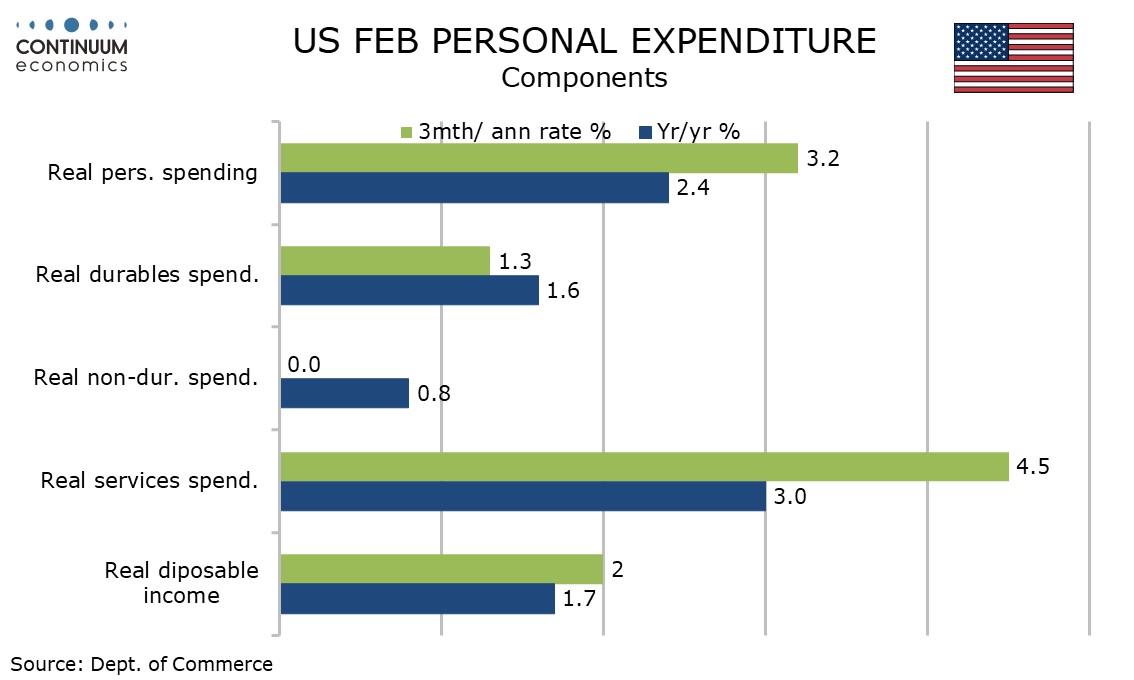

Personal spending was stronger than expected with goods up a moderate 0.5% in line with retail sales but services up a strong 0.9%, and by an impressive 0.6% in real terms. Service consumption, which also led the upward revision to Q4 GDP, look increasingly positive.

Spending outpacing income saw the savings rate fall to 3.6% from 4.1%, with January revised up from 3.8%, with February’s being the lowest since November 2022. Savings accumulated during the pandemic may be fading as a source of support but strong equity markets are increasingly supportive.

If real disposable income and spending are unchanged in March Q1 would see a subdued annualized gain of 0.8% in the former and a moderate 2.1% pace in the latter. The strong January will still lift Q1 core PCE prices. If March is unchanged we would see a 3.1% annualized gain after two straight quarters on the 2.0% Fed target. More plausibly, under a 0.2% March gain the Q1 pace would be 3.4%.