U.S. February Employment - Strong but not too strong

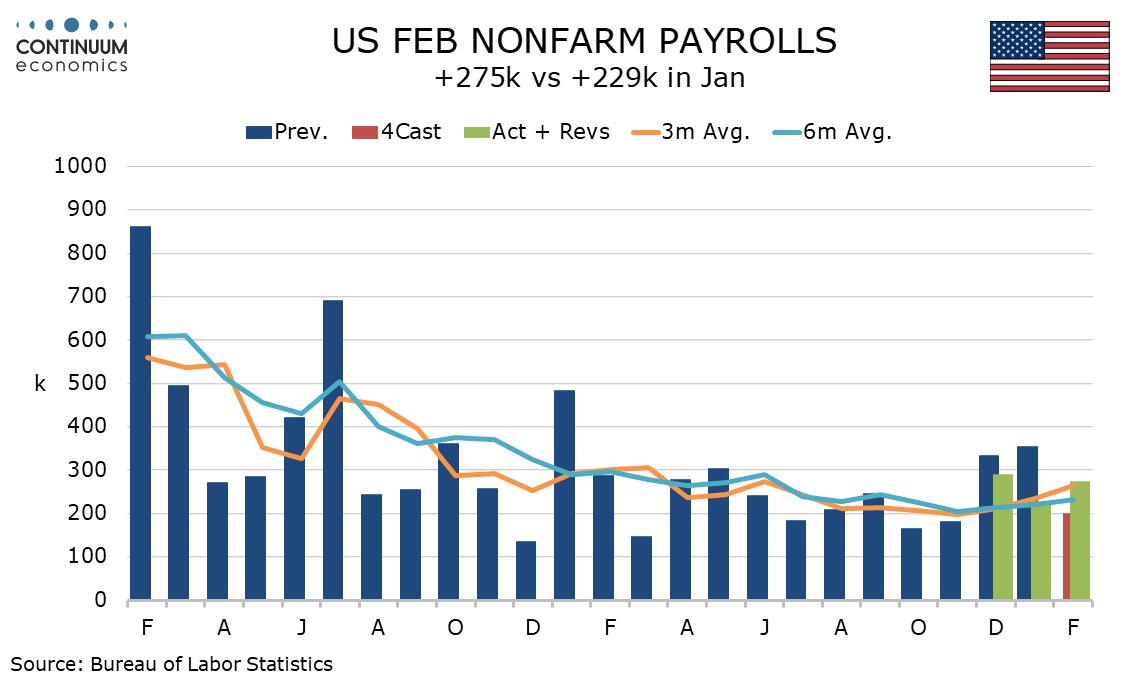

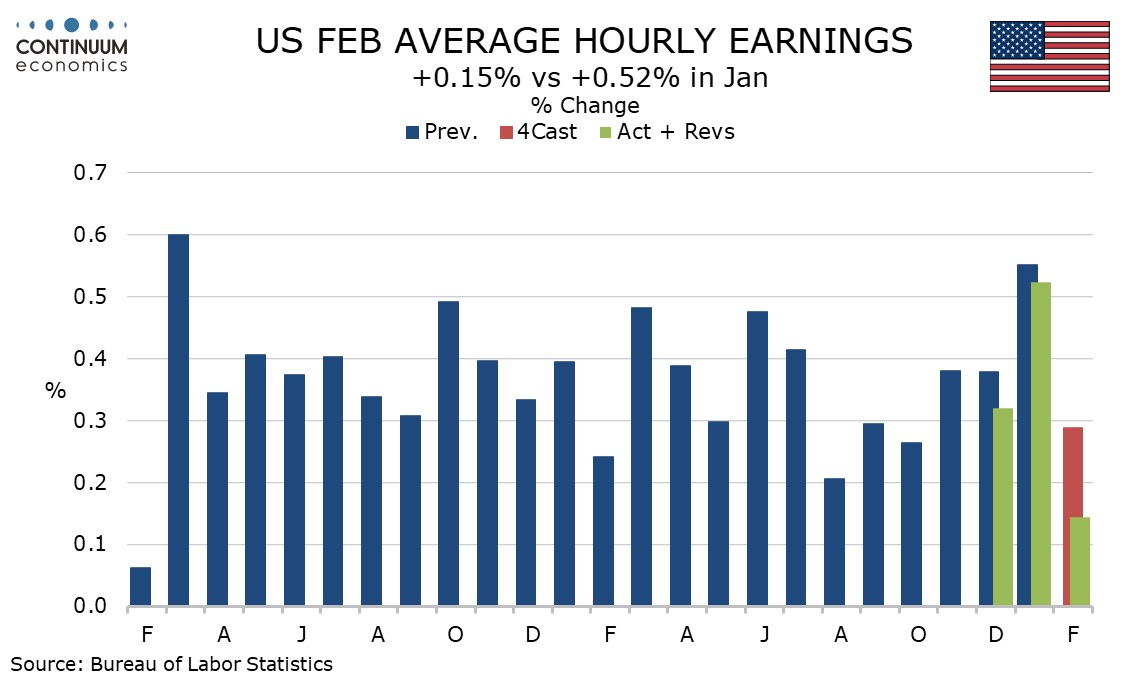

February’s non-farm payroll increase of 275k is strong though the upside surprise is offset by 167k of net downward revisions to December and January. Other details are softer, a 0.1% rise in average hourly earnings correcting from January’s above trend 0.5% (revised from 0.6%) and a rise in unemployment to 3.9% from 3.7%. The workweek did however rebound from a weather-related dip in January, and that is positive for activity.

The data is consistent with an economy still growing at a healthy pace but not so strongly as to be causing a resurgence in inflationary pressures, so is likely to be seen as good news at the Fed, maintaining the case for easing but not suggesting any pressing need to act quickly.

The non-farm payroll data continues to outperform the household survey which calculates the unemployment rate. The latter showed employment falling by 184k which combined with a 150k increase in the labor force pushed the unemployment rate to its highest since January 2022, at 3.9%.

January’s payroll was revised down to 229k from 353k and December’s to 290k from 333k, though three straight gains above 200k is clearly a strong pace with the 3-month average of 264k at 7-month high. Some saw the strong January as due to supportive winter seasonal adjustments. February seasonal adjustments are less generous so the continued strength is harder to dismiss.

February’s employment gains were led by health care and social assistance at 91k, the sector remaining strong, and leisure and hospitality at 58k, rebounding from a below trend January, where weather may have been an issue. Government at 52k maintains a strong trend, led by local government. There were few areas of weakness, though manufacturing did fall by 4k and temporary help, sometimes seen as a leading indicator, fell by 15k.

Average hourly earnings rose by 0.145% before rounding but with the revisions to January (to 0.524% from 0.553%) and December (to 0.321% from 0.38%) negative the data is clearly weaker than expected, and suggests January’s above trend data may have been inflated by a fall in the workweek. Yr/yr growth of 4.3% from 4.4% however still looks a little too strong to be consistent with 2% inflation.

The workweek at 34.3 hours corrected a January dip to 34.2 (revised from 34.1, with December also revised up to 34.4 from 34.3), meaning that aggregate hours worked with a 0.4% increase reversed a January decline and that suggests February economic data is likely to be stronger than January’s. Construction and retail saw particularly strong gains in aggregate hours.