UK Budget Review: Demographics Fail to Prevent Ever Smaller Fiscal Headroom?

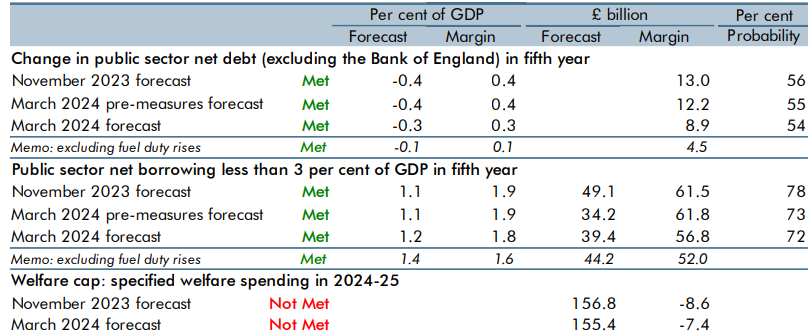

Chancellor Hunt’s Budget today was an even clearer politically driven affair. Hence the focus on offering alleged tax cuts, all framed as helping boost growth potential but where the tax as a share of GDP is forecast to rise to a post-war record 37.1% of GDP in 2028-29. The political question here is why; the same-sized 2p cut in national insurance contributions made in last November’s Autumn Statement failed to bolster the government’s opinion poll position, the very opposite; the latest poll reading put Conservative support at 20%, the lowest level since this survey began in 1978. Of course, cutting NI can be seen a pro-growth measure – back in November the Office of Budget Responsibility (OBR) did accept it boosted the supply side by some 0.2% of GDP. But politics is the focus as Chancellor Hunt will not have wanted to leave any fiscal leeway for the next government, this on the far from heroic assumption that it will not be Conservative! Hence, the decision to use some of the tax raising measures proposed by Labour but still resulting in virtually all fiscal headroom disappearing (Figure 1). As for BoE implications, they are modest but not negligible; this Budget according to the OBR provides a boost to demand in the near term and to supply in the medium term, averaging some 0.3% of GDP out to 2029, with the structural budget gap some 0.2% of GDP higher.

Figure 1: Performance Against Government Fiscal Targets

Source: OBR

Surprise Real Growth Outlook Upgrade

In contrast to most expectations, the real GDP outlook has been boosted, albeit marginally, this a result of inflation having receded more quickly than the OBR expected in November this inter-related with markets now expecting a sharper decline in interest rates. However, underscoring the stark fiscal outlook is the fact that the nominal and per capita growth outlook have been pared back. This is in spite of a major change in the OBR economy forecast (which we highlighted in our review), namely an increase in the size and growth of the UK population. However, the net impact considered by the OBR is minimal as higher and rising levels of inactivity offset its impact on the overall size of the workforce, leaving the assumed forecast for the level of GDP in five years virtually unchanged from the autumn, and the level of GDP per person slightly lower.

But Borrowing Profile Little Changed

As a result, the overall outlook for the public finances is also similar to November. Lower inflation and interest rates reduce the Government’s projected debt servicing and welfare costs, but they also reduce revenues. These pre-measures forecast changes result in a £20 billion fiscal improvement over the next two years but leave borrowing largely unchanged in five years’ time. The Budget announces a package of net tax cuts, including a further 2p cut to the main rates of employee and self-employed national insurance contributions, the cost of which is partially recouped by tax rises in later years. Borrowing is still projected to fall in each of the next five years thanks to tax as a share of GDP rising to near to a post-war high, debt interest costs falling, and per person spending on public services being held flat in real terms. This is just enough to meet the Government’s fiscal rules on our central forecast with underlying debt falling as a share of GDP in 2028-29 by a historically modest margin of £8.9 billion, or to just 0.1% of GDP on the basis that an assumed fuel duty hike does not occur.

Minimal Fiscal Headroom

We think this is unlikely. Moreover, even though the OBR forecast does suggest the opposite, there may still be a concern for markets, especially as the OBR were very wary of the fiscal assumptions the government is offering in order to meet its debt reduction target. Indeed, the OBR stressed that its fiscal forecast is also conditioned on the tax take rising to near record highs, including through planned rises in fuel duty that have not, in practice, been implemented since 2011, without which the fiscal margin to meet the debt rule would be around £ 4.5 bln or 0.1% of GDP (Figure 1). It also assumes the Government will stick to assumptions which imply no real growth in public spending per person over the next five years, despite committing to increase spending on some major public services in line with or faster than GDP.

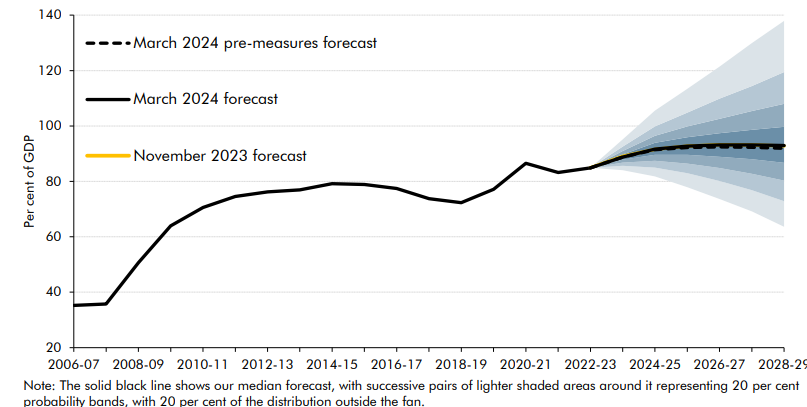

Figure 2: Government Debt Rise Has Upside Risks?

Source: OBR

Thus this delivers only a 0.3% ppt fall in the debt ratio in five years’ time, umping from 88.8 % this fiscal year to a peak of 93.2% in 2027-28 and with the drop to 92.9% actually a notch above that projected in the Autumn Statement. Moreover, the risk tilted to the upside Figure 2)