AMERICAS

View:

May 07, 2024

U.S. Fiscal Problems: 2025 More Than 2024

May 7, 2024 1:10 PM UTC

Current real yields in the U.S. government bond market already large reflect the large government deficit trajectory. Even so, H1 2025 could see some extra fiscal tensions that add 30-40bps to 10yr U.S. Treasury yields as the post president election environment will either see a reelected Joe Bide

April 26, 2024

Headwinds To Long-term Global Growth

April 26, 2024 9:30 AM UTC

Bottom line: While much focus is on the cyclical economic position to determine 2024 monetary policy prospects, the 2025-28 structural growth trajectory differs to the pre 2020 GDP trajectory for major economies. While global fragmentation has a role to play, aging populations are already having a

April 22, 2024

Short-end European Government Bonds Following U.S. But June Decoupling

April 22, 2024 1:15 PM UTC

The Fed’s shift to higher for longer has spilled over to drag European government bond yields higher through April. This now looks overdone as a June ECB rate cut is not fully discounted and ECB officials/data clearly point towards a 25bps cut. UK money markets are more out of line, with a Jun

April 17, 2024

Markets: Fed Rather Than Middle East Worries

April 17, 2024 12:34 PM UTC

Global markets are being driven by a scale back in Fed easing expectations and we see a 5-10% U.S. equity market correction being underway. However, with the market now only discounting one 25bps Fed cut in 2024, any downside surprises on U.S. growth or better controlled monthly inflation numbers

April 03, 2024

April 02, 2024

Asset Allocation: Pausing for Breath

April 2, 2024 9:00 AM UTC

Into Q2, data and policy (actual and perceived) will dominate DM markets. The ECB will likely take the spotlight with a 25bps cut on June 7, as the Fed face a better growth/more fiscal policy expansion and a tighter labor market than the EZ but also with a better productivity backdrop and outlook to

March 27, 2024

March 25, 2024

January 11, 2024

Webinar Recording December Outlook: Rate Cuts Into 2024

January 11, 2024 8:22 AM UTC

You can now access the webinar for the December Outlook here.

To read the individual chapters please see the weblink below.

Outlook Overview: Rate Cuts Into 2024 (here)

U.S. Outlook: Slower Growth to Sustain Improved Inflation Picture (here)

LatAm Outlook: Diverging Paths in 2024 (here)

China Outloo

January 08, 2024

Charting our Views December Outlook

January 8, 2024 9:05 AM UTC

Outlook Overview: Rate Cuts Into 2024 (here)

Economic Scenarios

U.S. Outlook: Slower Growth to Sustain Improved Inflation Picture (here)

LatAm Outlook: Diverging Paths in 2024 (here)

Brazil Policy Rate and CPI Inflation (YoY, %)

China Outlook: Headwinds To China Growth (here)

Japan Outlook: Normalizing

January 02, 2024

December Outlook: Rate Cuts Into 2024

January 2, 2024 9:53 AM UTC

Outlook Overview: Rate Cuts Into 2024 (here)

U.S. Outlook: Slower Growth to Sustain Improved Inflation Picture (here)

LatAm Outlook: Diverging Paths in 2024 (here)

China Outlook: Headwinds To China Growth (here)

Japan Outlook: Normalizing Monetary Policy Soon (here)

Asia/Pacific (ex-China/Japan) Outlook:

December 19, 2023

December 18, 2023

Outlook Overview: Rate Cuts Into 2024

December 18, 2023 3:42 PM UTC

· Uncertainty still prevails around this central view. The impact of lagged monetary tightening could be greater than our estimates and deliver mild recessions in some DM countries. We also feel that the disinflationary process could be stronger and this would help bring inflation back

December 15, 2023

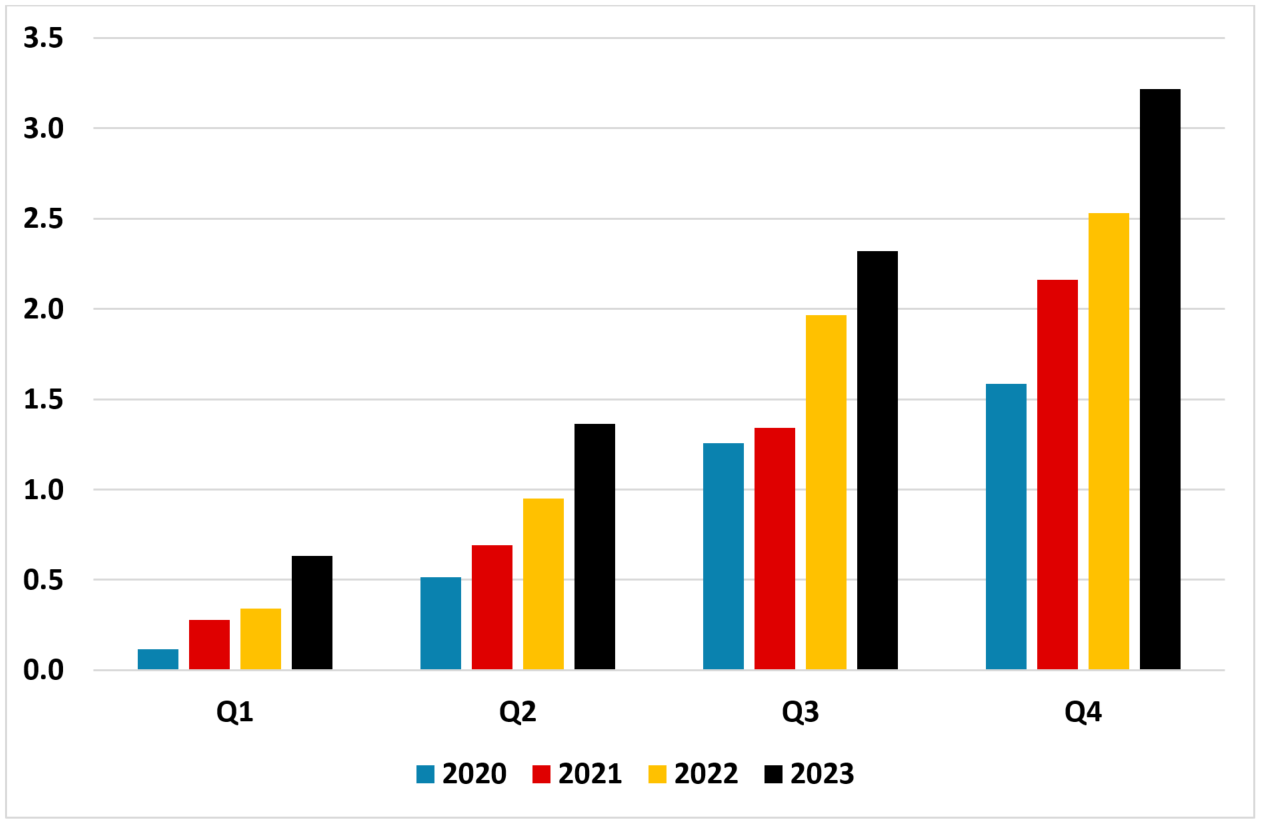

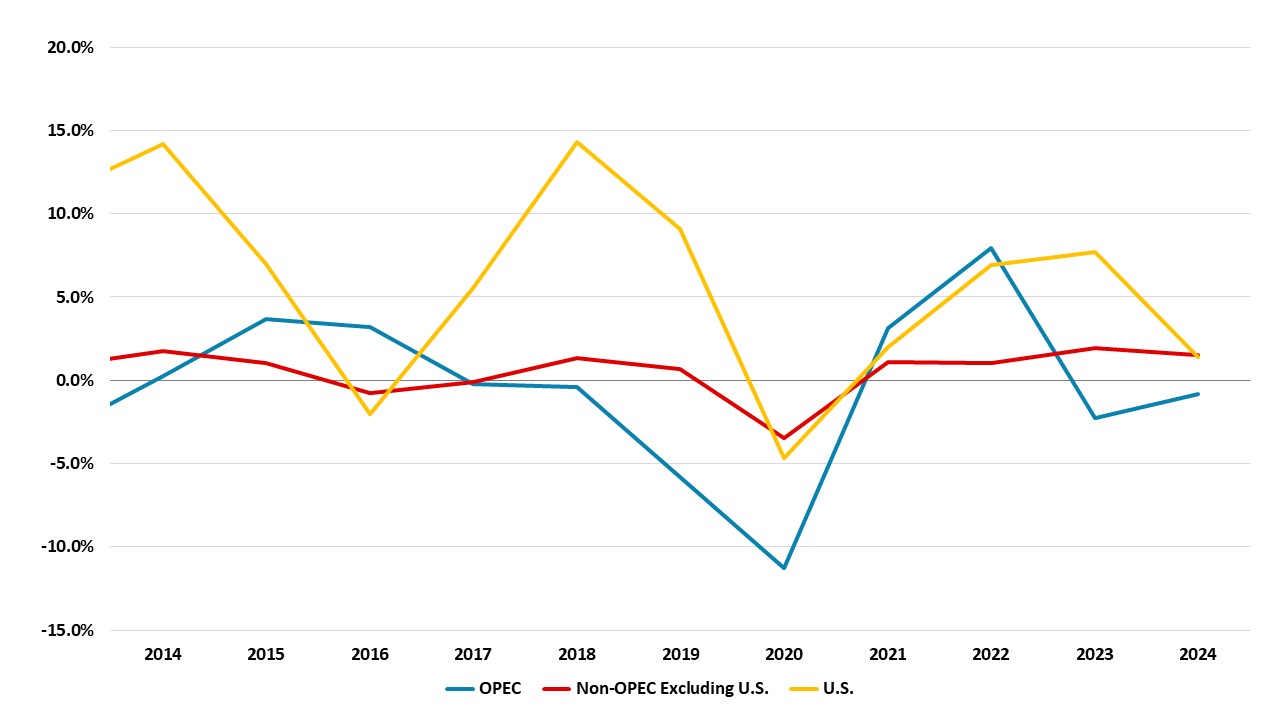

Commodities Outlook: Economic Forces at Play

December 15, 2023 11:21 AM UTC

• Oil: Production Cuts and Demand DynamicsThe trajectory of oil prices will be significantly shaped by both the production policies to be adopted by OPEC and the global economic growth. In light of the voluntary cuts agreed upon by several countries within the cartel during the November 202