China

View:

May 17, 2024

May 16, 2024

France and Japan: Debt Fuelled Growth Problem

May 16, 2024 10:30 AM UTC

Most of the surge in debt/GDP in Japan and 40% in France is due to higher government debt and this should not be a binding constraint provided that large scale QT is avoided – we see the ECB slowing QT in 2025 and are skeptical about BOJ QT in the next few years. The adverse impact of higher deb

May 15, 2024

China: Too Much Debt In Some Sectors

May 15, 2024 9:55 AM UTC

While part of corporate debt is quasi government (SOE and LGFV’s) and China creditors can be pursued to rollover by the authorities for larger borrowers, households and part of the private sector are focused on the previous buildup of debt. With China authorities reluctant to aggressive ease fis

May 13, 2024

China RRR and Rate Cuts

May 13, 2024 7:54 AM UTC

The latest China money supply and lending figures show that private household and business lending is very subdued. More need to be done to boost credit demand as well as credit supply. However, the authorities desires to avoid too much Yuan weakness will likely mean that the next move is a 25bp

May 10, 2024

Asset Allocation 2024: Tricky Seven Months Remaining

May 10, 2024 1:06 PM UTC

Fed easing expectations for 2025 and 2026 can shift from a terminal 4% Fed Funds rate towards 3%, as the U.S. economy slows due to lagged tightening effects. Combined with Fed easing starting in September this should mean a consistent decline in 2yr yields. However, 10yr U.S. Treasury yields wil

May 08, 2024

China Equities: A Tactical Play

May 8, 2024 2:20 PM UTC

China equities can see a tactical bounce of 5-10% in the coming months. Cheap valuations and underweight global fund positions means that the scale of pessimism only has to get less bad on the economy and China authorities attitude towards businesses. While we see a tactical opportunity, we do

May 03, 2024

EMFX: Diverging On Domestic Forces Not Less Fed Easing Hopes

May 3, 2024 10:45 AM UTC

While U.S. economic developments, plus Fed policy prospects, will be important in terms of EM currency developments, domestic politics and fundamentals will also be decisive. These can keep the South Africa Rand volatile in the remainder of 2024, given the risk of a coalition government and African

May 02, 2024

China Politburo: Help for Housing, But No Game changers

May 2, 2024 10:50 AM UTC

Politburo statement in late April suggests extra support for residential property. However, we see this as being incremental rather than any game changers and we still see residential investment remaining a negative drag on 2024 GDP growth.

April 29, 2024

China: Depreciation Rather Than Devaluation

April 29, 2024 1:00 PM UTC

We feel that a devaluation of the Yuan is unlikely in 2024, both to avoid potentially politically destabilizing capital outflows but also to avoid upsetting the next U.S. president. Policy is geared more towards controlled depreciation to help competiveness but reduce other risks. The Yuan has a

April 26, 2024

Headwinds To Long-term Global Growth

April 26, 2024 9:30 AM UTC

Bottom line: While much focus is on the cyclical economic position to determine 2024 monetary policy prospects, the 2025-28 structural growth trajectory differs to the pre 2020 GDP trajectory for major economies. While global fragmentation has a role to play, aging populations are already having a

April 24, 2024

China: Surging Government Debt and Does It Matter?

April 24, 2024 9:30 AM UTC

Total non-financial sector debt, plus the IMF estimates of government debt/GDP, do seem to matter for the action of China authorities, as fiscal policy stimulus is targeted rather aggressive as in 2009 or 2015. The overall debt picture also matters for the growth outlook, as the excess debt/GDP le

April 18, 2024

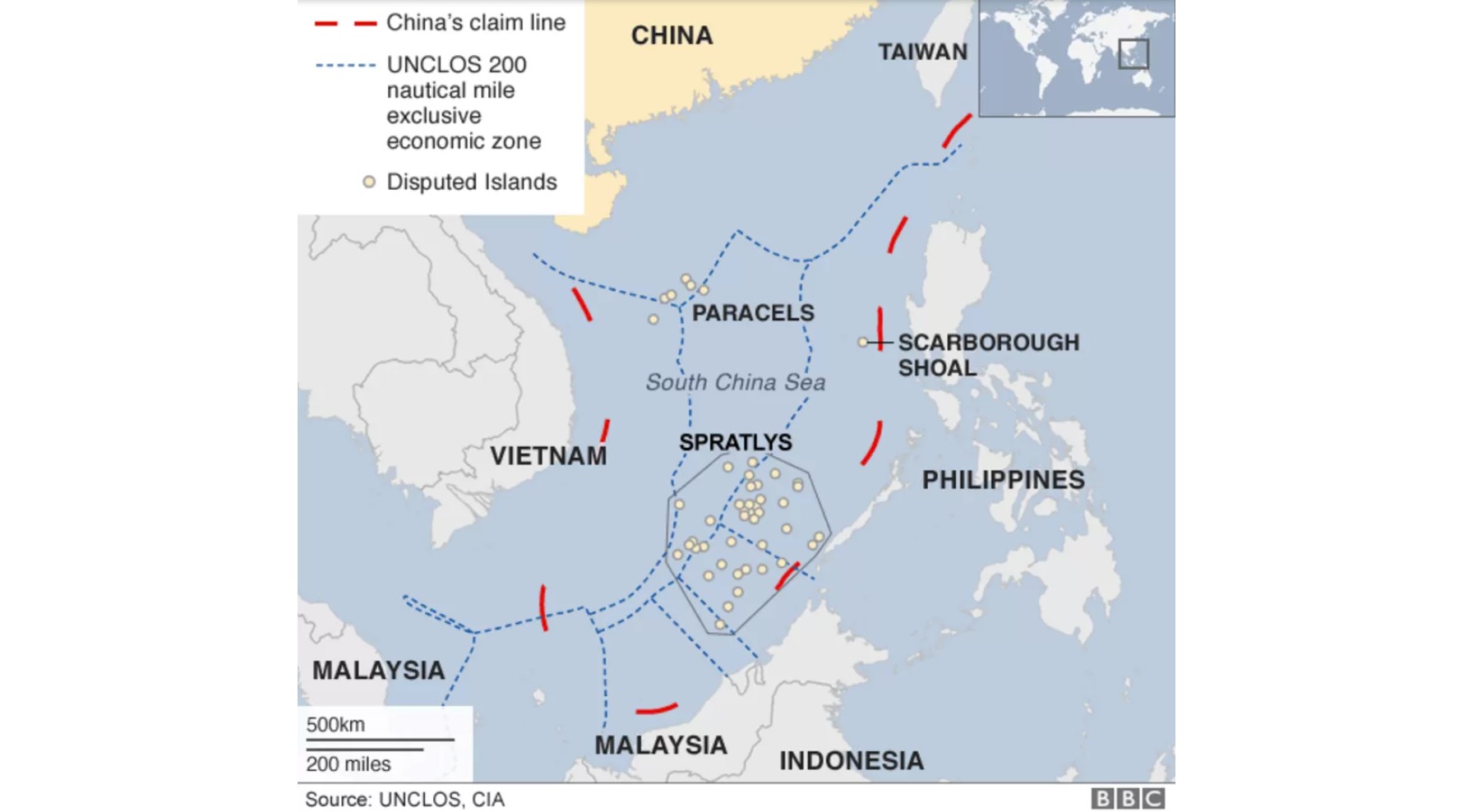

China and the South China Sea

April 18, 2024 2:00 PM UTC

Bottom Line: A China coastguard vessel blocked two Philippines government vessels over the weekend in the Second Thomas shoal area near the Philippines, which has raised questions over whether the South China Sea will be another geopolitical flashpoint. We would say not in 2024, both given China

April 17, 2024

April 16, 2024

China: Q1 Upside Surprise, but March Disappoints

April 16, 2024 8:33 AM UTC

Q1 GDP upside surprise was driven mainly by public sector investment. With the government still to implement the Yuan 1trn of special sovereign bonds for infrastructure spending, public investment will likely remain a key driving force. However, the breakdown of the March data show that retail s

April 03, 2024

April 02, 2024

Asset Allocation: Pausing for Breath

April 2, 2024 9:00 AM UTC

Into Q2, data and policy (actual and perceived) will dominate DM markets. The ECB will likely take the spotlight with a 25bps cut on June 7, as the Fed face a better growth/more fiscal policy expansion and a tighter labor market than the EZ but also with a better productivity backdrop and outlook to

March 27, 2024

March 26, 2024

EM FX Outlook: Domestic Drivers Key

March 26, 2024 9:01 AM UTC

In terms of spot EM FX projections domestic drivers remain critical, with a desire to avoid appreciation versus the USD for some countries. Fed easing in H2 2024 should however help EMFX more broadly and allow some recovery in spot rates (e.g. Indonesian Rupiah (IDR), South African Rand (ZAR)

March 25, 2024

Equities Outlook: Cyclical Recovery Versus Structural Headwinds

March 25, 2024 9:00 AM UTC

· In the U.S., a tug of war between momentum and U.S. exceptionalism on the one side versus valuations and any deviations from the U.S. goldilocks scenario now means volatility and a risk of a correction. We feel that the U.S. equity market recovery can push onto 5250 for the S&P5

March 20, 2024

China Outlook: The Struggle to Hit 5% Growth

March 20, 2024 11:00 AM UTC

China’s 5% growth target will likely be tough to meet with residential property investment likely to knock 1.0-1.5% off GDP and net exports a small negative. With sluggish private investment, this means some of the old engines of growth are not firing. Some additional fiscal stimulus will likely

March 18, 2024

China: Unbalanced Growth

March 18, 2024 8:28 AM UTC

The February monthly data shows unbalanced growth. Industrial production and public investment picked up, but retail sales slowed and residential property remains a negative drag on GDP. While H1 GDP growth will be ok, it will likely slow in H2 and we still stick to a forecast of 4.4% for 2024 a

March 15, 2024

China: No PBOC MTF Cut and Protesting Low Government Bond Yields

March 15, 2024 8:51 AM UTC

Bottom Line: The PBOC decided not to cut the Medium-Term Facility (MTF) rate, but surprised by also withdrawing liquidity in what looks like a protest at the recent decline in government bond yields. A 10bps MTF cut should still arrive in Q2, but later rather than sooner.

March 11, 2024

China: Lunar New Year Boosts CPI, But Disinflation Still In Place

March 11, 2024 8:29 AM UTC

Bottom Line: February China CPI surged to +0.7% v -0.8% Yr/Yr due to three factors. The late lunar New Year boosted CPI seasonally, while the good lunar New Year also boosted pork/food prices and travel prices. The bounce is unlikely to be sustained and we see a fall back to 0.3-0.4% Yr/Yr in Ma

March 06, 2024

March 05, 2024

China: 5% 2024 Goal Tough with L Shaped Residential Property

March 5, 2024 9:43 AM UTC

Bottom Line: China’s 5% growth target will likely be tough to meet with residential property investment likely to knock 1.0-1.5% off GDP and net exports a small negative. With sluggish private investment, this means the old engines of growth are not firing. Some additionally fiscal stimulus will

March 04, 2024

Taiwan Speaker Reduces China/Taiwan War Risk

March 4, 2024 10:30 AM UTC

Bottom Line: Taiwan new speaker, Han Kuo Yu, has a willingness to open dialogue with China. This does not stop China likely undertaking large scale military exercises in the spring around Taiwan, as it still seeks to pressure the incoming DPP president. However, we see the new Taiwan speaker elect

February 28, 2024

China: Authorities Views and Policy Changes

February 28, 2024 10:15 AM UTC

Bottom Line: China authorities leave the impression that further policy stimulus will likely be measured rather than aggressive. We feel that they are not pessimistic enough on the medium-term hangover from the residential property sector and this is why we are downbeat on 2024 GDP growth and beyo

February 22, 2024

EMFX: Carry and Domestic Fundamentals Rather Than the USD

February 22, 2024 10:00 AM UTC

Bottom Line: Most major EMFX currencies have performed better than the Euro or the Japanese Yen against the USD in 2024 (Figure 1). This is due to carry trades in Latam, but elsewhere reflects global equity love on Indian equities or domestic fundamentals. This resilience for Brazilian Real/Indi

February 21, 2024

China: Yuan Outflow Fears Versus Net Exports

February 21, 2024 11:00 AM UTC

Despite a still overvalued Yuan, China authorities are reluctant to accept too much Yuan weakness for fear of causing domestic capital outflows and discontent with China’s government. At some stage, if GDP growth surprises on the downside, China authorities could decide that a controlled Yuan decl

February 20, 2024

China: 5yr LPR Cut But Not 1yr LPR

February 20, 2024 9:17 AM UTC

A larger than expected 25bps cut in the 5yr Loan Prime Rate (LPR) has been delivered, but the 1yr LPR rate was unchanged given that PBOC reluctance to cut the 1yr Medium-Term Facility rate (MTF) this month. The 5yr LPR rate is not a game changer for residential property, as bigger policy moves are

February 13, 2024

China: 5% or 4.5-5.0% Growth Target

February 13, 2024 10:34 AM UTC

Though economics would argue for a 4.5-5.0% growth target for 2024, politics will likely mean that a 5% growth target is chosen in March. With the residential property overhang, weak net exports with a shift of global supply chains and sluggish private sector business investment growth, this will

January 17, 2024

China: GDP 5.2% for 2023, but 2024 To Struggle

January 17, 2024 9:24 AM UTC

Quarterly GDP is interesting and came in at 1.0% after the 1.3% quarterly gain in Q3. The trend in quarterly GDP (Figure 1) is also not consistent with 5% growth and the Yr/Yr will dip in Q1 2024 when the large gain in Q1 2023 drops out (due to the end of zero COVID policies). We maintain the 4.

January 16, 2024

January 15, 2024

Taiwan: DPP Weaker than 2020

January 15, 2024 8:49 AM UTC

The DPP have won the Taiwan presidential election. However, the DPP has lost its majority in parliament, while the 3rd party (Taiwan People Party (TPP) are signalling they will not form a coalition with (Kuomintang) KTT. This will restrain the DPP. However, China will still likely show its dis

January 12, 2024

China: January MTF and March RRR Cut?

January 12, 2024 9:25 AM UTC

Figure 1: China RRR (%)Source: Datastream/Continuum Economics

A senior PBOC official has hinted at an RRR cut on Tuesday (here), given the desire to sustain credit growth. Similar comments were evident last July before the RRR cut in September. We would argue that further monetary easing is l

January 11, 2024

Webinar Recording December Outlook: Rate Cuts Into 2024

January 11, 2024 8:22 AM UTC

You can now access the webinar for the December Outlook here.

To read the individual chapters please see the weblink below.

Outlook Overview: Rate Cuts Into 2024 (here)

U.S. Outlook: Slower Growth to Sustain Improved Inflation Picture (here)

LatAm Outlook: Diverging Paths in 2024 (here)

China Outloo

January 09, 2024

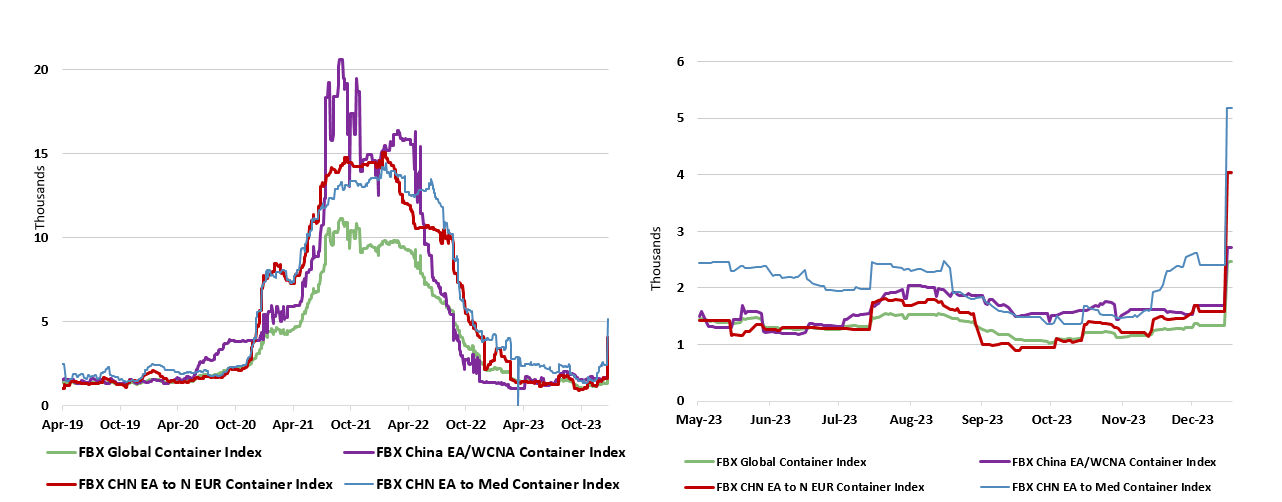

Shipping Freight Cost Jump and Inflation – Some Perspectives

January 9, 2024 2:24 PM UTC

Figure 1: Freight Cost Surge in Perspective

Source: DataStream

How Long?

Houthi rebels have been attacking some ships in the Red Sea in recent weeks. The key question is how long this will last? One line of thinking is that the Houthi attacks are part of Iran axis of resistance alongside attacks

January 08, 2024

Charting our Views December Outlook

January 8, 2024 9:05 AM UTC

Outlook Overview: Rate Cuts Into 2024 (here)

Economic Scenarios

U.S. Outlook: Slower Growth to Sustain Improved Inflation Picture (here)

LatAm Outlook: Diverging Paths in 2024 (here)

Brazil Policy Rate and CPI Inflation (YoY, %)

China Outlook: Headwinds To China Growth (here)

Japan Outlook: Normalizing

January 05, 2024

China: Five Headwinds To Long Term Growth

January 5, 2024 9:00 AM UTC

The catch-up productivity argument would point towards 4-5% growth in China in the 2025-2030 period. However, we are concerned that the residential property downturn and rewiring of global supply chains will be persistent headwinds for China GDP growth in the coming years and that the adverse popu

January 03, 2024

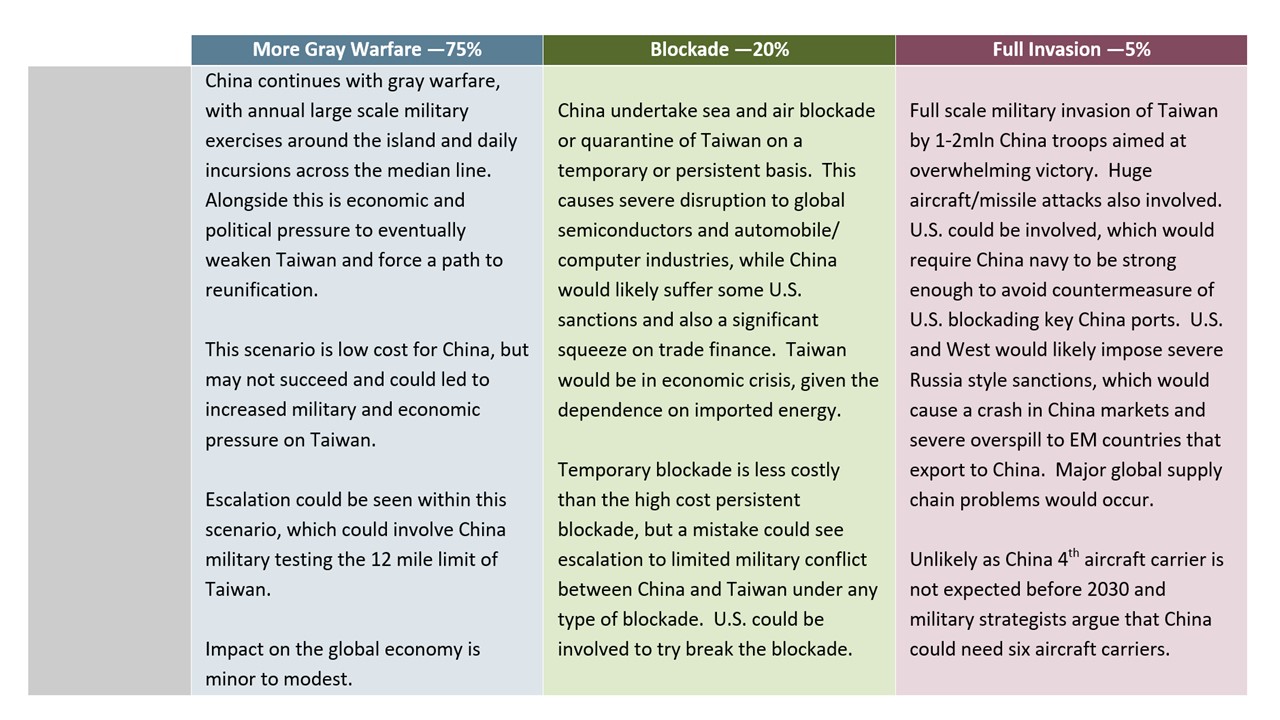

Taiwan: Gray Warfare After A Mixed Election

January 3, 2024 11:02 AM UTC

With the Taiwan elections on January 13 expected to re-elect the DPP, and the U.S. focused on Ukraine and Middle East, how will the Taiwan situation develop after the election and in the coming years?

Figure 1: Taiwan Scenarios for the Next 5 Years

Source: Continuum Economics

More Gray W

AI and Technology Impact on Growth and Inflation

January 3, 2024 10:30 AM UTC

Bottom Line: The full benefits of the latest AI wave will likely not kick in until the late 2020/early 2030’s.However, 5G over the last couple of years has been enabling more connectivity via the Internet of Things and allowing more big data analysis, including AI tools and algorithms. In the 2hal

January 02, 2024

December Outlook: Rate Cuts Into 2024

January 2, 2024 9:53 AM UTC

Outlook Overview: Rate Cuts Into 2024 (here)

U.S. Outlook: Slower Growth to Sustain Improved Inflation Picture (here)

LatAm Outlook: Diverging Paths in 2024 (here)

China Outlook: Headwinds To China Growth (here)

Japan Outlook: Normalizing Monetary Policy Soon (here)

Asia/Pacific (ex-China/Japan) Outlook:

December 27, 2023

USD Reserve Status: Slow Slippage

December 27, 2023 1:23 PM UTC

Figure 1: Pct of USD in Allocated FX Reserves

Source: IMF COFER/Continuum Economics

The latest IMF COFER data (here) shows that the USD still remain the dominant currency among central banks, with the Euro in 2nd place at 19.6% followed by the Japanese Yen and British Pound. The Chinese Yuan i

December 20, 2023

Outlook Forecasts to download in Excel

December 20, 2023 7:31 AM UTC

We forecast across 23 countries annual and quarterly. Our annual forecasts go out to 2028, while our quarterly forecasts are now updated out to Q4 2025. The forecasts are consistent with the December Global Outlook ‘Rate Cuts Into 2024’ published on 18th December 2023.

The file contains nine sh

December 19, 2023

EM FX Outlook: USD Decline v Inflation Differentials

December 19, 2023 9:59 AM UTC

· In spot terms, we see the Indonesian Rupiah (IDR) and Malaysian Ringgit (MYR) rising against the USD as Fed rate cuts narrow interest rate differentials and a move away from an overvalued USD occurs. Brazilian Real (BRL) and Mexican Peso (MXN) will likely be stable against the USD

December 18, 2023

Outlook Overview: Rate Cuts Into 2024

December 18, 2023 3:42 PM UTC

· Uncertainty still prevails around this central view. The impact of lagged monetary tightening could be greater than our estimates and deliver mild recessions in some DM countries. We also feel that the disinflationary process could be stronger and this would help bring inflation back