FX Weekly Strategy: Europe, May 6th-10th

USD/JPY returns to previous highs after BoJ action

Further downside seen for USD/JPY

USD could also slip lower against riskier currencies

SEK may rise as Riksbank leaves rate hike until June

GBP vulnerable to more dovish BoE stance

Strategy for the week ahead

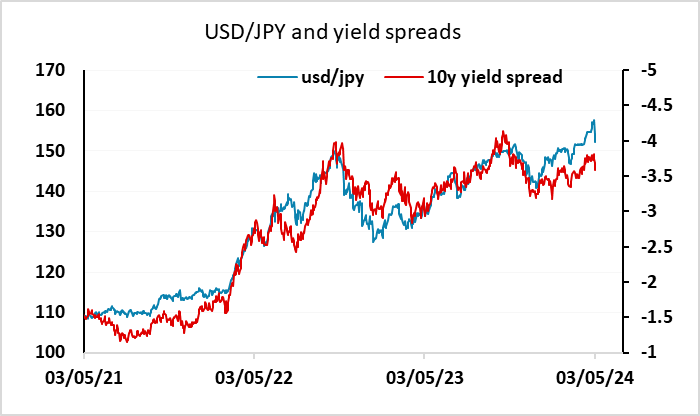

The focus in the last week has very much been on the JPY, with the BoJ intervention reversing the JPY weakness of the previous few weeks. USD/JPY and EUR/JPY are both back to the levels seen on April 10, the day that USD/JPY broke through the previous highs from October 2022. It is significant that the BoJ have forced USD/back to those levels, as it was at those levels that the BoJ intervened in October 2022. The message is that you need to take notice of BoJ intervention levels, and speculating on JPY weakness beyond those intervention levels will not be profitable. While the official data on the size of BoJ JPY buying will not be available for another month, BoJ data suggests something in the region of $35bn, which is somewhat less than the $60bn spent in October 2022. But the size is of limited relevance. The message is that, whatever they say in public about volatility, USD/JPY gains beyond 150 are not welcome and will not be allowed to persist.

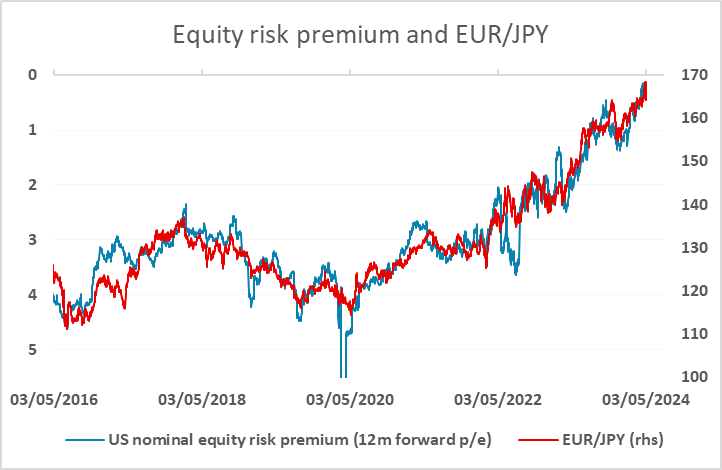

From here, we may now see some further JPY gains, as the correlation with yield spreads suggests scope for USD/JPY to fall back to the high-140s. The correlation with equity risk premia has, however, held up rather better in recent weeks, and suggests there is more limited downside scope for EUR/JPY, with current risk premia suggesting EUR/JPY should hold somewhere in the mid-160s. This suggests there may also be further upside for EUR/USD. While front end yields don’t suggest major upside potential for the EUR. The positive equity tone is supportive, and the relatively weak US survey data from the PMIs and the ISM also provide some rationale for a generally weaker USD.

Datawise, there isn’t much this week from the US and Eurozone, but there is the Japanese labour cash earnings data, which is seen as significant for BoJ policy. The data is only for March, and there is more focus on the wage agreements made in April for the coming year, but this could nevertheless be a trigger for JPY moves.

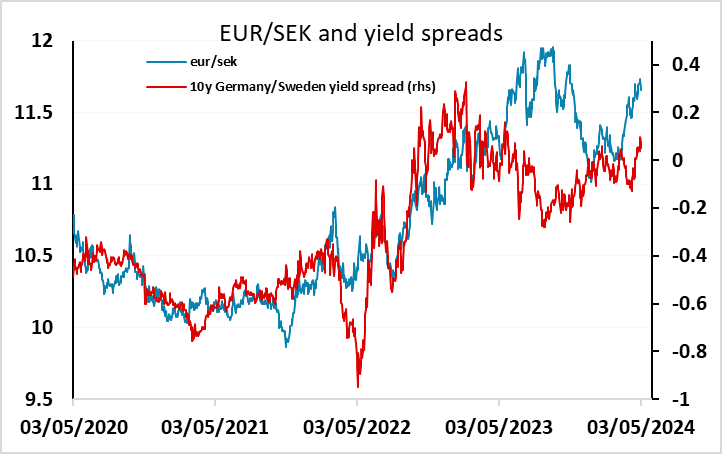

This week also has central bank meetings in the UK, Australia and Sweden, with the UK and Sweden likely to be the most interesting. We don’t expect a policy change at any of the meetings, but the Riksbank is a very close call, with the market pricing a cut as around a 50-50 chance. This being the case, the SEK can be expected to rise if the Riksbank don’t cut, even though in that case they will probably signal a cut is likely in June. EUR/SEK already looks a little extended, so should have potential down to 11.60 on no change in policy. If there is a cut, we would favour NOK/SEK higher, as the more hawkish Norges Bank stance and the low level of NOK/SEK relative to yield spreads suggests scope to parity and beyond.

For the UK, there is little chance of a cut at this week’s meeting. But the accompanying updated Monetary Policy Report (MPR) may show a much softer and more persistent near/below target inflation outlook, enough to make one or maybe two more MPC members vote for a cut even at this juncture. However, the rest of the MPC, not least the three hawks, will want to see the possibly vital April CPI data (due May 22) to assess the likelihood of a target undershoot and the extent to which persistent price pressures may have ebbed. But we still think the first 25 bp BoE cut may still arrive at the June 20 meeting and we look for around 75 bp of cuts this year and even more in 2025. With the market only pricing 50bps of cuts, and no move until August, there is potential for EUR/GBP to rise to 0.86 and beyond on a more dovish BoE stance.

Data and events for the week ahead

USA

It is a very quiet week for US data which will put focus on Fed speakers. Monday sees Barkin and Williams, while the Fed’s Senior Loan Officer Opinion Survey on bank lending practices is due. On Tuesday Kashkari will speak and March consumer credit is due. Wednesday sees Cook speak and March wholesale trade. Weekly jobless claims are due on Thursday. Friday sees the preliminary May Michigan CSI where inflation expectations should be watched while Goolsbee is due to speak.

Canada

Canada’s most significant release is April employment on Friday which will be the last employment report before the June 5 Bank of Canada rates decision. Tuesday sees April’s Ivey manufacturing PMI.

UK

A key but holiday-shortened week sees the BoE gives its next verdict on Thursday. We think that the BoE is moving towards rate cuts but we do not see any move this time around, with Bank Rate again likely to remain at 5.25%. But the accompanying updated Monetary Policy Report may show a much softer and more persistent near/below target inflation outlook, enough to make one or maybe two more MPC members vote for a cut even at this juncture. The decision will be accompanied by more BoE compiled survey data (Decision Makers’ Survey) and where after the press conference Chief Economist Pill will give a virtual Q&A. The BoE may have seen the GDP data due the following day. Notably, the modest added momentum so far in Q1, and despite what we think may be a 0.1% m/m March contraction (Figure 1), suggests that the last quarter may still see GDP growth of 0.3% q/q, higher than current BoE thinking and fully reversing the slide and continued mild recession in Q4 last year. One key area for the BoE is the extent to which the housing market is recovering – the RICS survey (Thu) will provide some important insights.

Eurozone

Datawise, the main event media-wise will be Fridays account of the last ECB Council meeting, this preceded by an array of speeches due from Council members through the week. The account may offer needed insight into a possible path for rate cuts amid what was some dissent from a minority in favor of actual cuts at that juncture. One area we will be looking for any comments is the negative impact from the ECB’s balance sheet reduction on credit dynamics which was very much underscored in the bank lending survey. (Probably), there are also the European Commission economic forecast update where GDP projection may be curbed with the question being whether the just-above target rate for HICP inflation is belatedly trimmed.

Data is thin on the ground, but more weak retail sales (Tue) and PPI (Mon) numbers may be followed by more construction sector weakness in the sector PMI numbers. German industrial production (Tue) likely to see a fresh and perhaps a clear m/m falls as may manufacturing orders numbers due a day earlier.

Rest of Western Europe

There are key events in Sweden, with orders and production numbers on Friday. But the main event will be the Riksbank decision (Wed). Even at it previous policy assessment in February it was clear(er) that the Riksbank accepted that it could and should make its policy stance less contractionary, at least in conventional terms. On balance, and in spite of the latest downside CPI surprise, amid Board concerns about continued krona weakness we see a split vote, but with no change this time around, with the first move coming next month instead. Otherwise, the SNB releases FX reserve data (Tue). Finally, CPI data in Norway may see these April numbers fall even further below the Norges Ban’s projections with a drop to 4.3% for CPI-ATE, which would be a 21-mth low.

Japan

Labor cash earning is the only critical release next week on Friday, apart from BoJ’s summary of opinion on Thursday. The labor cash earning will of period in March, likely beginning to see a pick up in wage after the negotiation phrase and should see further acceleration above or close to 2%. BoJ Summary of Opinion likely non-event as there does not seem to be any debate on April decision.

Australia

RBA’s interest rate decision is on Tuesday and is forecast to be on hold. The inflation picture does not allow RBA to ease but is not hot enough to trigger a hike. The slightly higher than expected CPI may deter the RBA from signalling an early easing cycle and likely to see another copy and paste statement. We also have ANZ job ads on Monday and Retails Sales on Thursday, with the later could help assessing the softening of domestic demand.

NZ

We only have Business PMI on Friday for NZ.