BoE Preview (May 9): Easing Bias Clearer?

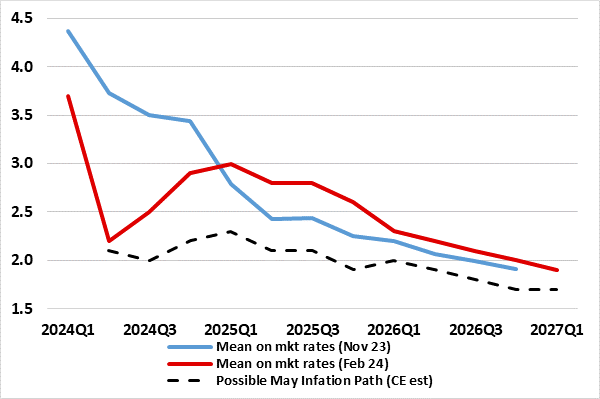

In flagging no need to be dominated by Fed policy, we think that the BoE is not only moving towards rate cuts but the MPC majority may be overtly advertising such a likelihood. But we do not see any move at the looming May 9 verdict, with Bank Rate again likely to remain at 5.25%. But the accompanying updated Monetary Policy Report (MPR) may show a much softer and more persistent near/below target inflation outlook (Figure 1), enough to make one or maybe two more MPC members vote for a cut even at this juncture. However, the rest of the MPC, not least the three hawks, will want to see the possibly vital April CPI data (due May 22) to assess the likelihood of a target undershoot and the extent to which persistent price pressures may have ebbed. Even given what we feel are somewhat better but exaggerated real economy signs now emerging, we remain of the view that disinflation (already evident even in falling services inflation, Figure2) will continue. As a result, we still think the first 25 bp BoE cut may still arrive at the June 20 meeting and for around 75 bp of cuts this year and even more in 2025.

Figure 1: A Probable Softer Inflation Profile from the BoE?

Source: BoE, CE

MPC Divisions Continue

It is clear that MPC thinking is in state of flux. Although it was no shock that the BoE voted to keep policy on hold at the last (March) meeting, there was some surprise that all hawkish dissents ended, with the one dissent instead still calling for a cut. Dominating BoE thinking then - and still - is a focus on assessing how ‘persistent’ are price pressures. Thus the MPC in March still suggested policy would need to remain restrictive for sufficiently long to return inflation to the 2% target but was also more open in accepting that the stance of monetary policy could remain restrictive even if Bank Rate were to be reduced, a view implicitly reiterated by Chief Economist Pill recently. Notably, and possibly indicative of a swing towards favouring near-term rate cuts, Dep Gov Ramsden was recently more willing to accept that persistent price pressures have actually eased. Indeed, he stressed that he saw the balance of risks to the inflation outlook has now now tilted to the downside, with a scenario where inflation stays close to the 2% target over the whole forecast period as very possible.

Inflation Outlook Stays Near Target?

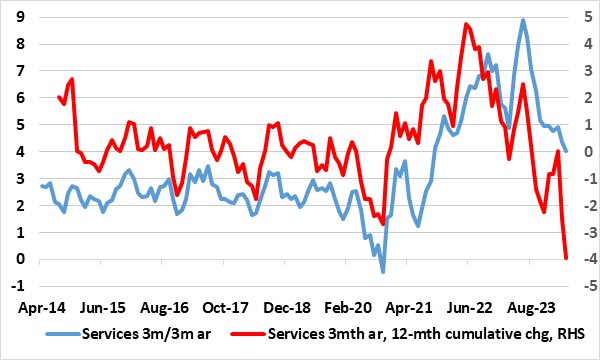

This is something we agree with, and note (Figure 1) that even with a small upgrade to the 2024 GDP picture (the MPC will surely have early access to Q1 national account data ahead of their formal release on May 10), the updated forecasts may see a clear downward revision. This will not only reflect what will be a higher market interest rates assumption of around an average 0.5 ppt, but also better inflation indicators even for seemingly resilient services. Indeed, while not matching the slump in non-energy industrial goods inflation, the pace of the recent fall is actually much greater when looked at using more short-term dynamics (Figure 2) which exclude current marked adverse base effects. Using a 3-month annualized seasonally adjusted rate (ie a measure that the BoE seems to be embracing increasingly of late), services inflation is now running at just over 4%, having halved in the last year, encompassing an average m/m drop of 0.5 ppt, over twice the rate at which services rose to the May 2023 peak.

Figure 2: Current Fall in Services Inflation Faster than the Surge?

Source; ONS, CE

Downside Growth Risks Remain

This leaves the UK as less of an outlier when it comes to recent inflation dynamics and where we remain cautious about the likely speed of any recovery in the real economy. Admittedly, the BoE is likely to suggest that an even greater proportion of the interest rate hikes may have come through already than the two-thirds estimate it offered in February, albeit with the full impact only to come well in to 2025. But a further and also sizeable –and possibly more prolonged – hit to spending power is now hitting those renting as rent inflation has risen to a 30-year high of over 7% and may remain elevated.

Again this background, we think an even clearer easing bias will be the theme of the May MPR, as the MPC also seeks to embrace the improved communication that was the major theme of the recent Bernanke Report.

Regardless, clearly MPC thinking had shifted a little further, not least as the rate hike demands have stopped amid a clear(er) acceptance that itis no longer a question of how restrictive policy needs to be but one of how long current restriction needs to stay in place. Particularly given what we think is over-pessimism about so-called persistent inflation pressures, we think that the implicit easing bias will be exercised soon, with rate cuts starting in June and 75 bp on the cards for the whole of this year and more to come in 2025. The QT issue, will again be left to one side at least for the time being.