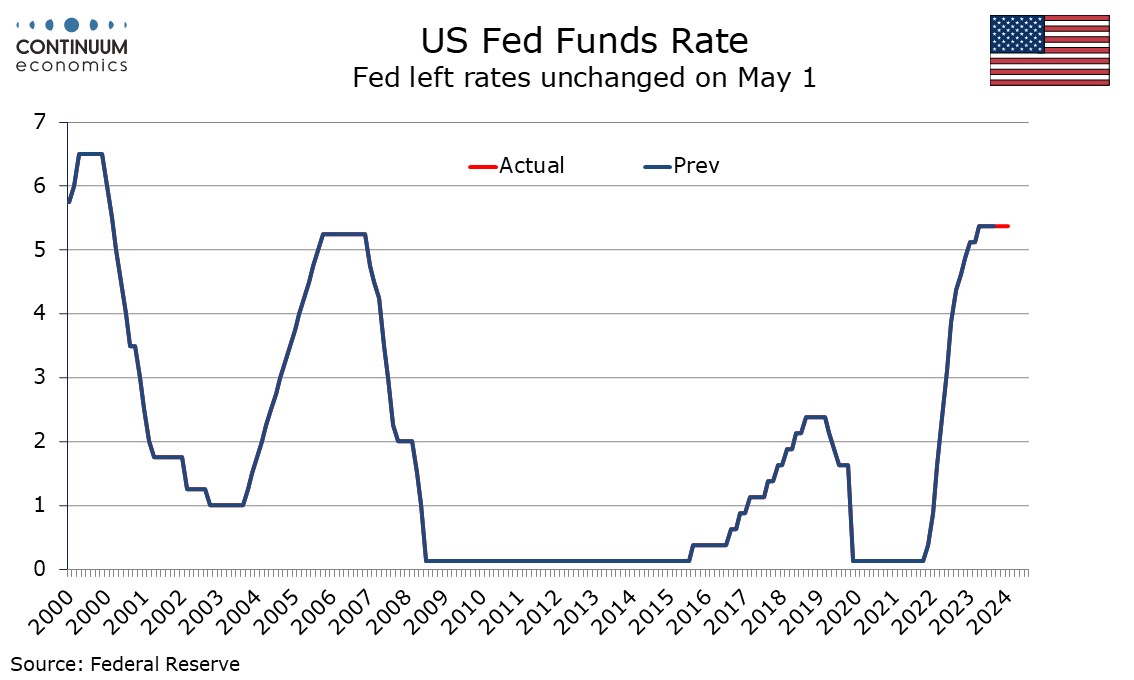

FOMC Still Waiting For Data to Justify Easing

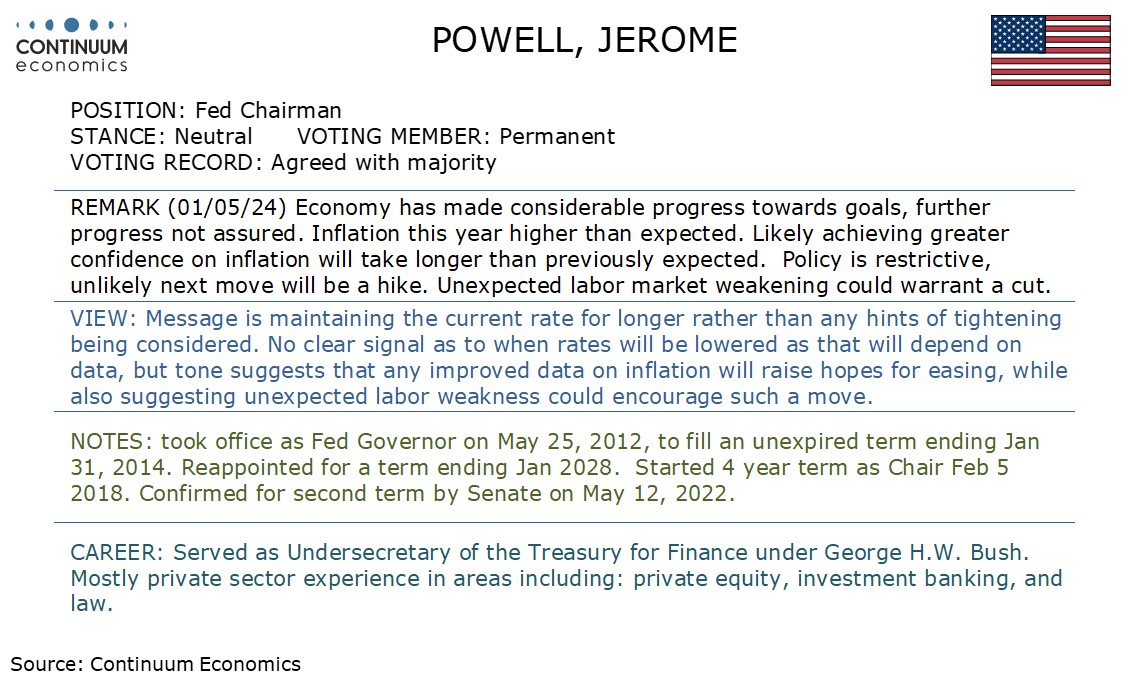

The May 1 FOMC statement, and Chairman Jerome Powell’s press conference, while noting recent inflation disappointment, did not deliver a strong pivot in tone. The Fed is still waiting for data to allow easing to take place, but still expects inflation to slow, and looks ready to respond once data allows. We do not expect easing until September, but stick with a view for two more moves in Q4, assuming that by then data has slowed significantly.

The main change to the statement was an addition rather than an edit, stating that in recent months there has been a lack of progress toward to 2% inflation objective. A more subtle adjustment was to state that risks have moved into a better balance over the past year rather than are moving into better balance, to emphasize the recent stalling of progress on inflation while noting that last year did see significant progress. Otherwise the only significant change was to announce a slowing of the pace of Quantitative Tightening starting in June, with the monthly cap for USTs falling to $25bn from $65bn, though that for agencies will be left at $35bn. The decision on the balance sheet does not come as a major surprise though some may have expected the tapering to be phased in a little more slowly.

The key phrase, not expecting to reduce the target range until there is greater confidence that inflation is moving sustainably towards target, is maintained. At the press conference Powell stated that achieving the necessary confidence will likely take longer than expected. This suggests that easing will start later than previously expected, and this implies that the Fed will ease by less than the 75bps projected for this year in the March dots (which was only one dot away from a median of only two eases). In the absence of further progress on inflation, the Fed would be likely to continue keeping rates steady.

However, Powell’s tone was not hawkish. He stated it was unlikely that the next move will be a hike, and also suggested an unexpected weakening in the labor market could warrant a cut, suggesting greater potential for the Fed to respond to softer than expected than stronger than expected data, and not only on inflation. We do believe that some of the recent inflation strength reflects residual seasonality at the start of the year and that by the summer inflation data is likely to be more subdued. We also expect the economy, and the labor market, to lose some momentum though not by enough to threaten recession. The Fed will need several pieces of softer data before it decides to ease, and is unlikely to have enough to do this in June or even July, but there is plenty of time for the tone of data to change by September’s meeting. Three rate cuts this year is probably more than the Fed now expects, but if data by Q4 has seen the tone significantly change, Powell’s latest tone suggests he would respond. We cautiously continue to project easing in both the November and December meetings, data permitting.