FX Daily Strategy: Asia, May 2nd

Europe returns to digest the FOMC impact

USD may start to suffer of market sees loss of economic momentum

JPY most favoured, but EUR also has upside potential

CHF decline depends more on European recovery than SNB

Europe returns to digest the FOMC impact

USD may start to suffer of market sees loss of economic momentum

JPY most favoured, but EUR also has upside potential

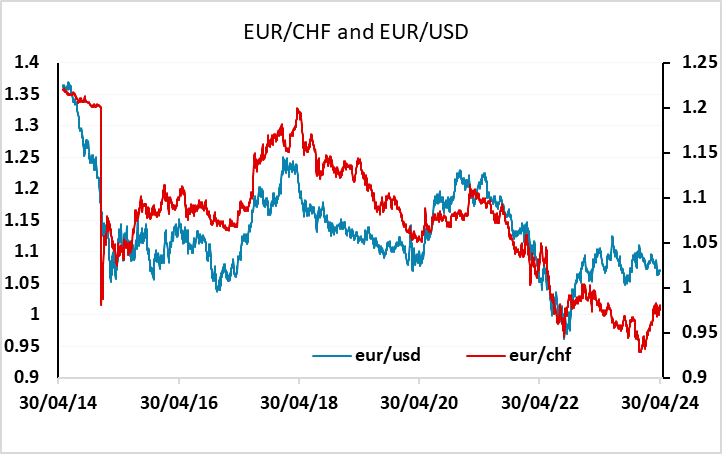

CHF decline depends more on European recovery than SNB

Thursday is likely to be a day for Europe to digest the details of the FOMC meeting after the May Day holiday and prepare for the US employment report and ISM services data on Friday.

The USD lost a little ground ahead of the FOMC meeting on Wednesday on the back of a weaker than expected ISM survey, which gave some support to the weaker PMI survey seen last week. While the immediate focus remains on the inflation picture and the likely Fed response, the evidence of some weakening in US economic momentum may spell the beginning of the end for the period of USD strength we have seen in recent years. Underpinning the strength of the USD has been the outperformance of the US economy and the confidence that the growth cycle will continue. This was maintained even through the pandemic and the inflation that followed. However, if we start to see the economy lose momentum, either US yields will decline as the Fed eases, or equities will decline if the Fed doesn’t feel able to ease because of elevated inflation. This would typically be supportive for the JPY, as it implies rising equity risk premia.

JPY strength continues to look like the most likely outcome in the coming months, with the BoJ resisting further JPY strength, yield spreads already suggesting scope for JPY gains, and the JPY stating from record levels of weakness. Timing may still be difficult, but risk/reward now dramatically favours a JPY recovery. However, there may also be a general USD decline if we see a reversion to the early year market expectation of substantial rate cuts. It should be remembered that although the USD is particularly strong against the JPY, the EUR is also exceptionally weak, and if we see lower US yields and some recovery in the Eurozone economy, this is also likely to be a trigger for EUR/USD gains.

There isn’t much data of interest in Thursday, with just trade data and the usual jobless claims numbers in the US. However, there is Swiss CPI data. This has surprised on the downside in recent months, and has in part been responsible for the SNB easing ahead of other central banks. The consensus has a small rise in the y/y rate in this month’s data to 1.1%, but this would still leave it at a level which would allow further SNB easing. Even so, purely by dint of the relatively low starting level of Swiss rates, there is unlikely to be much yield spread movement against the CHF from here. But yield spreads have not typically been the main driver of EUR/CHF, and if we see a Eurozone recovery ther eis scope for EUR/CHF to rise, especially if EUR/USD is rising.