Preview: Due May 2 - U.S. March Trade Balance - Deficit to increase on weaker goods exports

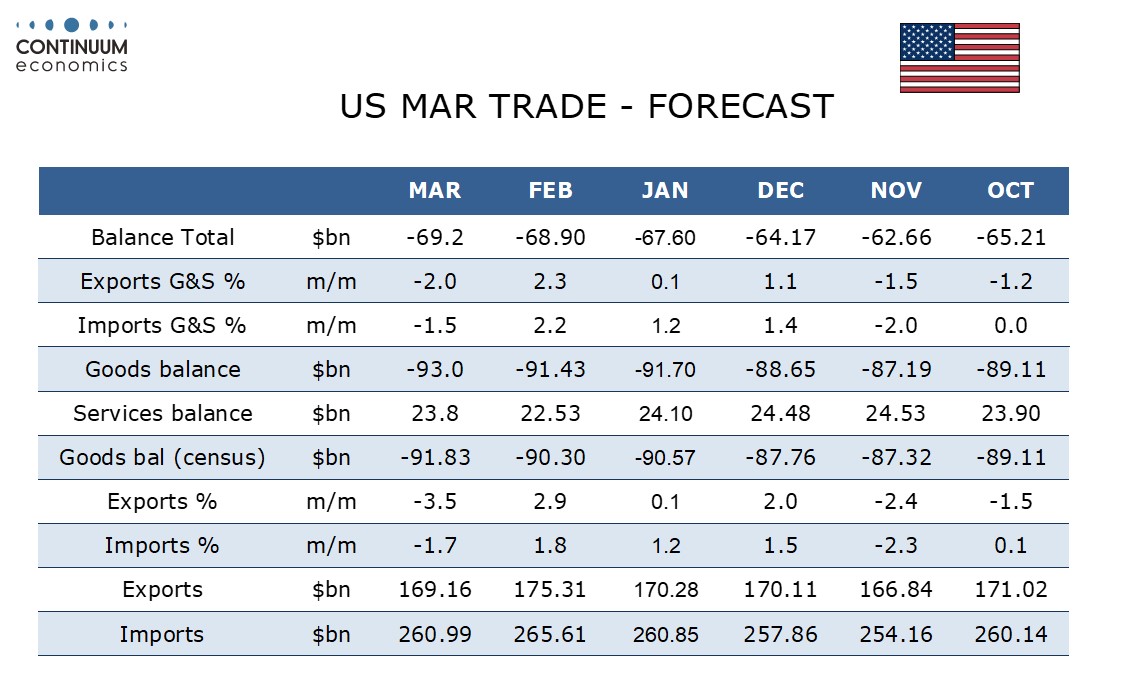

We expect March’s trade deficit to see a marginal increase to $69.2bn from $68.9bn, with a 2.0% decline in exports and a 1.5% decline in imports. This would be the fourth straight increase in the deficit to its highest level since April 2023.

Advance goods data showed a 3.5% decline in exports and a 1.7% decline in imports, and we expect similar outcomes, which would correct respective gains of 2.9% and 1.8% seen in February and lift the goods deficit to $93.0bn from $91.bn.

We expect service exports to see a second straight rise of 1.0% but service imports to fall by 0.7% after a rise of 3.9% in February. This would lift the service surplus to $23.8bn, up from $22.5bn in February but still below January’s $24.1bn. This is consistent with the assumptions for March services data in the Q1 GDP report.