FX Weekly Strategy: April 15th-19th

GBP in focus on labour market and CPI data

Scope for a more dovish tone to emerge if earnings data soften further

EUR/USD downside looks more restricted from here

JPY likely to have bottomed out on the crosses

Strategy for the week ahead

GBP in focus on labour market and CPI data

Scope for a more dovish tone to emerge if earnings data soften further

EUR/USD downside looks more restricted from here

JPY likely to have bottomed out on the crosses

After significant events in the US, in the form of the March CPI data, and the Eurozone, in the shape of the ECB meeting, this week sees the UK take centre stage with key labour market and CPI data. The labour market data may be the more important for the Bank of England’s thinking with the average earnings numbers in particular the main stumbling block for rate cuts from the perspective of the BoE hawks. There remains considerable doubt about the accuracy of the earnings data, but further declines in the HMRC version of earnings growth would provide more ammunition for the BoE doves. The CPI data looks likely to show further declines in the y/y rates due to base effects, but this is unlikely to be enough to change any MPC members minds about the need for near term rate cuts.

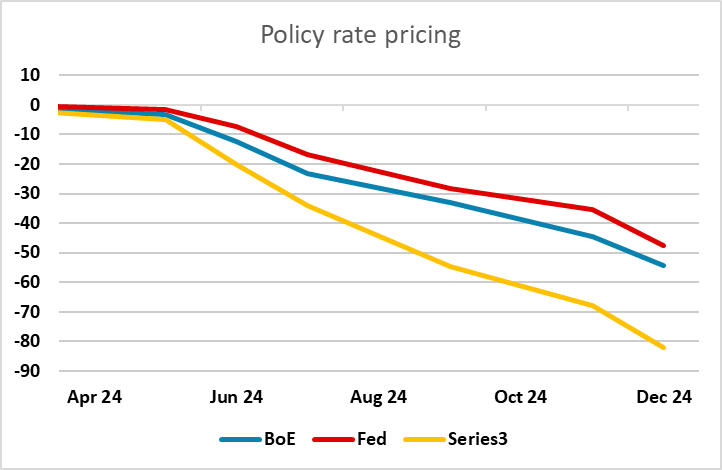

As it stands, the UK curve is only pricing a May rate cut as around a 13% chance, with June seen as around a 50-50 chance. We would estimate these probabilities as being rather higher, with the decline in rate expectations in the last week following the move in Fed expectations rather than working off any UK news. There were comments from MPC member Greene indicating that rate cuts were still a long way off, but she is a well established hawk, and the last meeting saw the hawks capitulate and an 8-1 vote with one vote (Dhingra) for no change. While it would need a significant decline in earnings growth and other evidence of weakness in the labour market and/or the CPI data to make a May cut a realistic possibility, it may not take much to move the market towards seeing a June cut as a probability.

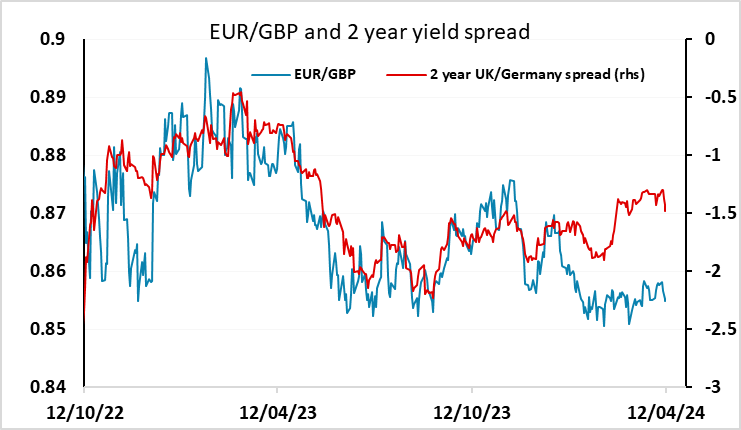

As it stands, EUR/GBP has continued to hold above 0.85, with the widening in yield spreads in GBP’s favour in the last week not sufficient to offset the narrowing seen since mid-February. Stronger than expected numbers could see 0.85 come under pressure, but we would expect the 0.85-0.86 range to hold if the data is broadly as expected.

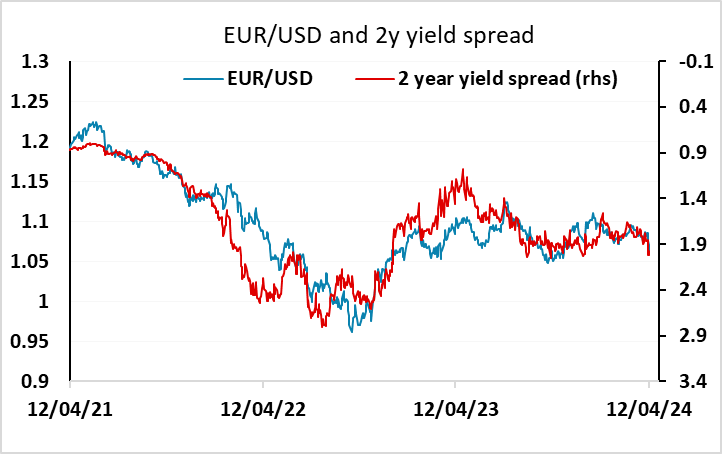

There may be some clarification of the ECB stance with speeches from various council members this week, starting with chief economist Lane on Monday. The market response to the meeting was quite uncertain, with an initial neutral read giving way to a more hawkish take by the end of the day but reverting to a neutral read by Friday. The market was pricing in an 80% chance of a rate hike in June by the end of the week, much as it was before the meeting. It will be hard to price in much more than this as it seems clear that the decision is still data dependent. The EUR saw fairly significant weakness in the aftermath of the meeting, but much of this related to the rise in US yields seen after the CPI data. This may see some modest correction this week, so the EUR’S decline may see a modest correction this week, although it will be hard for EUR/USD to get back above 1.07 unless we hear some quite aggressively dovish commentary from the Fed (which is unlikely).

Friday did see quite a sharp rise in the JPY on the crosses as yields fell in the US and Europe and equities also moved lower. It does now look to us that EUR/JPY has likely peaked for the medium term above 165, with rate spreads likely to move in the JPY’s favour over the year and starting from a place where the JPY is generally very cheap, both absolutely and relative to yield spreads. JPY strength would no doubt accelerate if there were some intervention from the Japanese authorities, but this looks unlikely unless we see a return to general JPY weakness (rather than just USD/JPY strength).

Data and events for the week ahead

USA

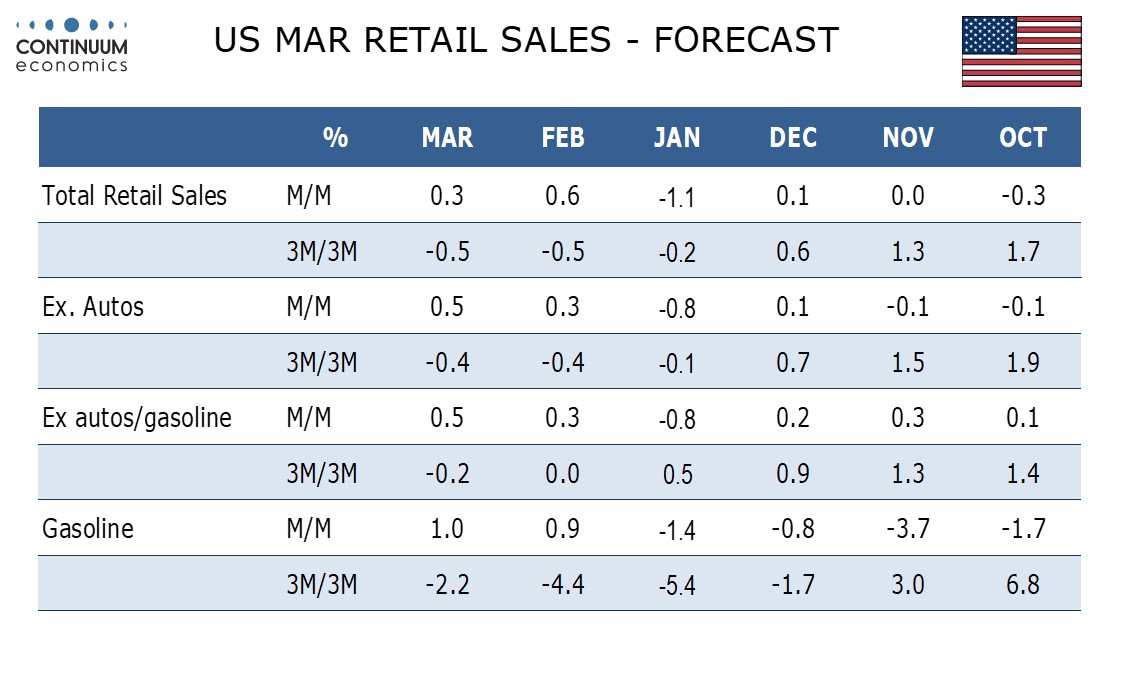

The most significant US data release of the week is probably Monday’s retail sales report for March. We expect a 0.3% increase, 0.5% ex autos, though this would still leave a negative Q1 weighed down by a weather-depressed January. April’s Empire State manufacturing survey is due at the same time while April’s NAHB homebuilders’ survey and February business inventories follow. Existing data implies a rise of 0.4% in the latter. Fed’s Logan speaks on Monday.

On Tuesday we expect March housing starts to correct lower by 2.7% to 1480k but permits to rise by 0.4% to 1530k. Later we expect a 0.6% increase in March industrial production, with manufacturing up by 0.3%. Fed’s Daly and Jefferson will speak on Tuesday. There is no significant data due on Wednesday though the Fed’s Beige Book will be released. Fed’s Mester and Bowman will speak.

Thursday sees weekly jobless claims and April’s Philly Fed manufacturing survey. We also expect March existing home sales to fall by 3.0% to 4.25m, correcting a 9.5% February increase. Fed’s Bowman will speak again, while Williams and Bostic are also scheduled. Friday sees no significant data but Fed’s Goolsbee is due to speak.

Canada

On Monday Canada sees March existing home sales, as well as February data for manufacturing shipments and wholesale sales, for which preliminary data saw gains of 0.7% and 0.8% respectively. Canada’s most significant release is March CPI on Tuesday, and here we expect a bounce to 3.0% yr/yr from 2.8% in a correction from two straight slower months. The Federal budget will also be delivered on Tuesday.

UK

Major data awaits. Tuesday sees the labour market update still presented amid continuing concerns over the accuracy of figures. The revised numbers may show a softer than thought jobless rate and higher inactivity, but there will be as much weight on HMRC numbers regarding job dynamics which have suggested clearer slowing in private sector employment. However, the average earnings figures will be the most closely watched and where we see only a modest slowing in both regular pay growth (3 mth mov avg) at just below 6% and the headline rate remaining down to 5.5%. Regardless, with even the BoE (belatedly) casting doubt on the validity of these numbers, more attention may be paid to the PAYE pay data where a clear(er) slowing has already been seen. Tuesday also sees the Treasury Select Committee review the appointment of Clare Lombardelli as BoE Deputy Governor for Monetary Policy, thereby giving her an opportunity to highlight any policy leanings before she formally takes up her role in July. BoE Governor Bailey also talks from the USA.

Wednesday sees the March CPI. Recently, there has been some rise in apparent core momentum as measured by adjusted m/m numbers, including still-solid service strength and this may be apparent in the March numbers too. Even so, base effects should pull the headline down to 3.2% and the core to 4.2%, a 28-month low, albeit the former a notch above BoE projections. The week ends with March retail sales, numbers again likely to be affected by unseasonable weather with the mild and wet condition leading to what we think ill will be a small m/m fall.

Eurozone

The ECB remains centre stage in the coming week. More clarification of the policy outlook may come with an array of Council member speeches, led by Chief Economist Lane on Monday. Data is sparse, with EZ industrial production (Mon) likely to show a clear m/m rise, but this anticipated February bounce would still imply a marked / drop on the cards for Q1. In addition construction data (Thu) is likely to remain weak while visible trade data may show some clearer recovery in imports. Finally EZ final HICP data (Wed) is likely to confirm the larger than expected fall in the flash numbers. Otherwise German ZEW survey data should show a more positive tone

Rest of Western Europe

There are key policy thinking updates in Sweden with nearly all Riksbank Board member scheduled to speak but with Governor Thedéen and Dep Gov Breman to participate in IMF spring meetings on Monday. Norway sees the Norges Bank bank lending survey and in Switzerland recent SNB recruit Martin speaks on policy (Thu).

Japan

National CPI would be the critical read for Japan next Friday. The pace of CPI would determine the next tightening from the BoJ. We are forecasting CPI to be lower than BoJ estimate and only one more hike in June. If headline CPI remains stubbornly high, we may see more tightening. Trade data on Wednesday would also be interesting to watch.

Australia

We only have the labor report for Australia next week on Thursday. The Feb jobs report has surprised to the upside after two consecutive weak report and remind the market Australian labor market, albeit peaked, is still solid. While we do not forecast another block buster report, any health report will be supportive for the Aussie in a knee-jerk reaction.

NZ

Q1 CPI on Wednesday would be the spotlight. RBNZ has previewed that Q1 CPI will likely spike higher for transitory factors in the last RBNZ meeting minutes and have already pre-emptive calm the market by suggesting rates will be high for longer. If CPI actually surprise to the downside, we could see some weakness in the Kiwi. There is also Business PMI on Monday.