Published: 2024-03-27T12:56:10.000Z

Preview: Due March 28 - U.S. Final (Third) Estimate Q4 GDP - Revision seen marginally lower but still strong

Senior Economist , North America

-

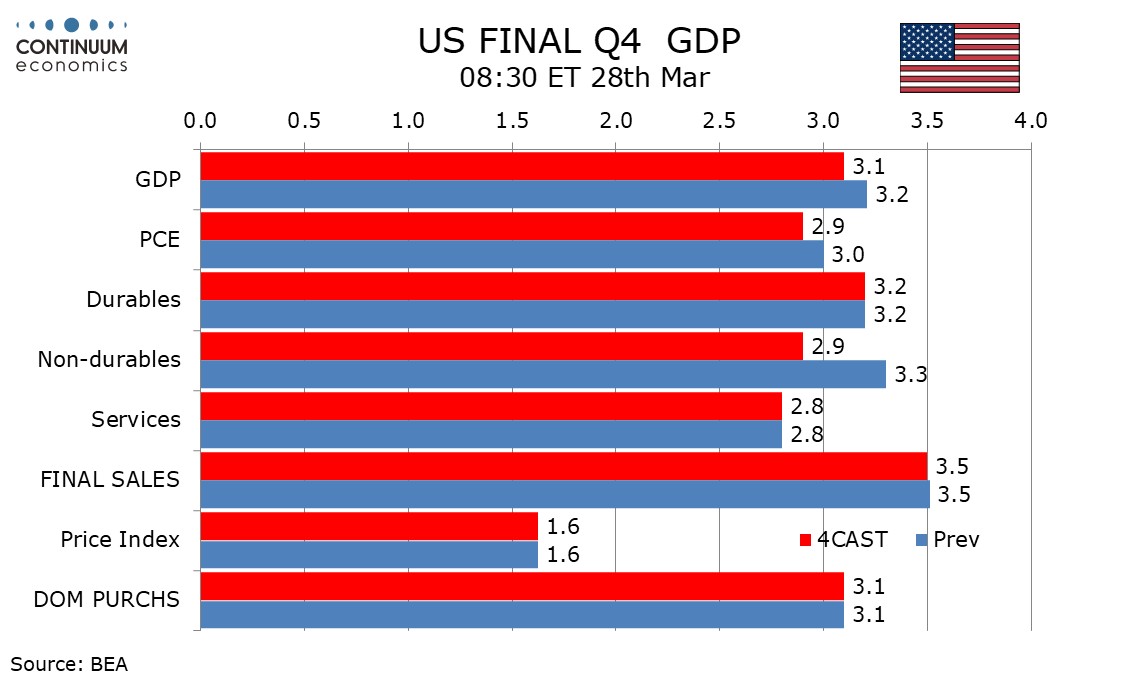

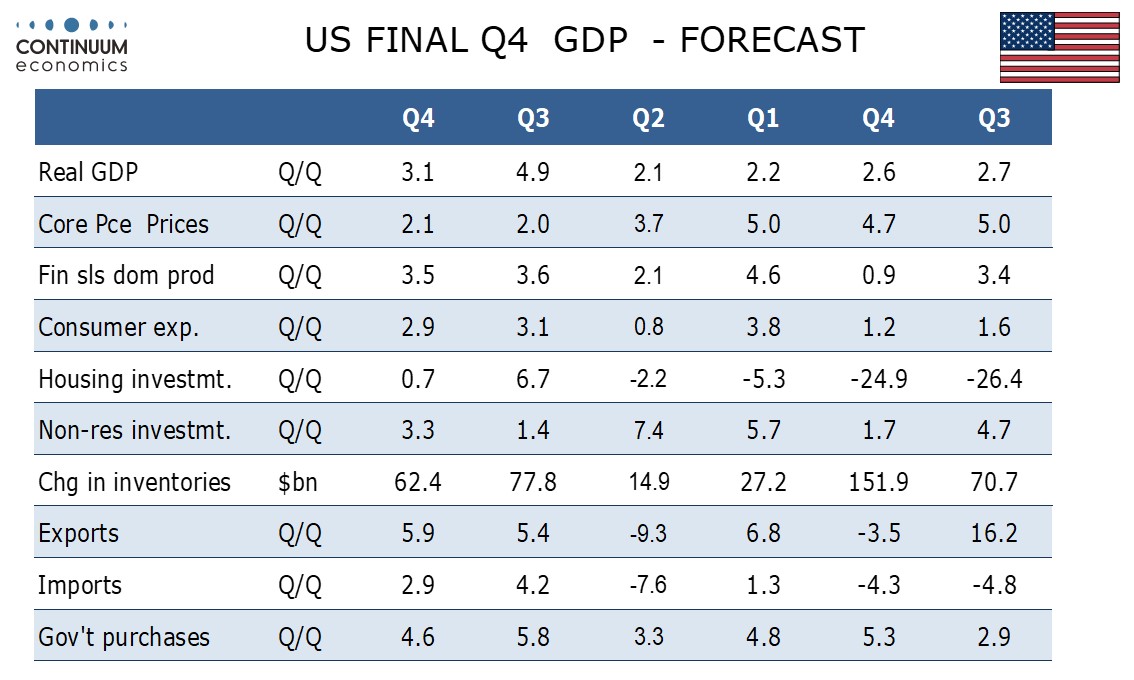

We expect the third (final) estimate for Q4 GDP to be revised marginally lower to a still strong 3.1% from second (preliminary) estimate of 3.2%.

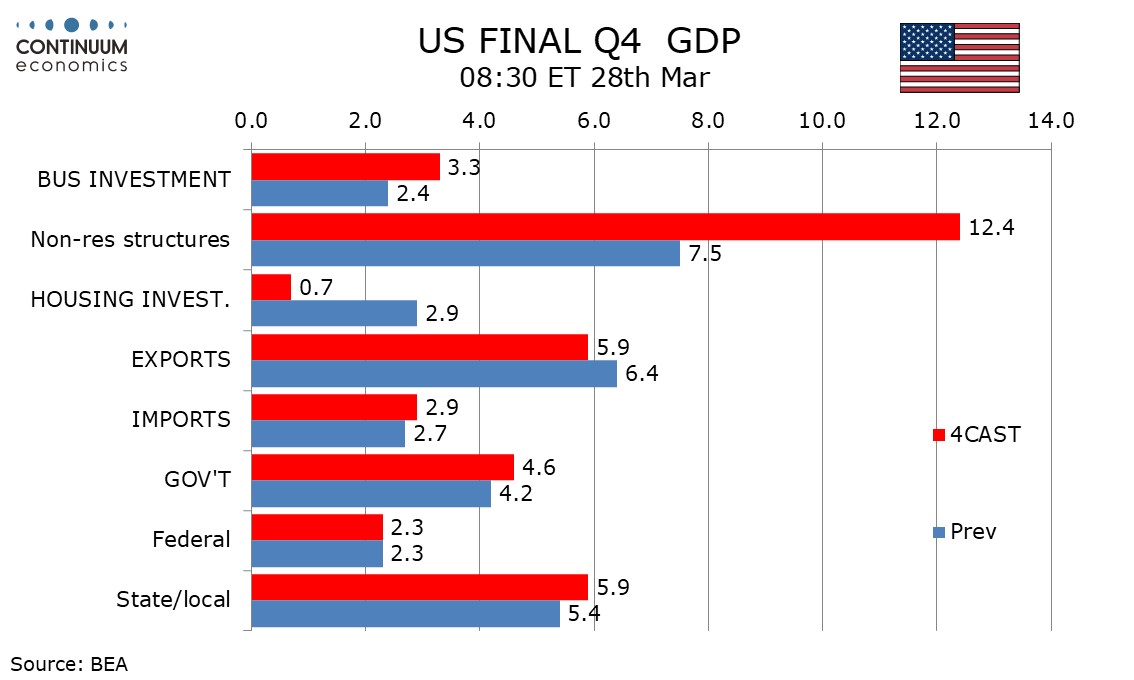

We expect downward revisions to retail sales, housing construction, inventories and net exports, the latter largely on a downward revision to the services surplus.

Upward revisions are likely to business investment, on private non-residential construction, and government, also on construction.

We expect final sales (GDP less inventories) to be unrevised at 3.5%, and final sales to domestic buyers (GDP less inventories and net exports) to be unrevised at 3.1%.

We do not expect any revisions to the price indices, from 1.6% for GDP, 1.8% for overall PCE and 2.1% for core PCE.