Fed: 2024 Easing To Reduce Degree of Restriction

The March FOMC leaves the impression that the Fed still feels that they will reduce the scale of restrictive monetary policy and the upward revision to 2024 GDP and core PCE medians are not significant. On balance, July is the most likely meeting, followed by two further cuts in Q4. We see a further 100bps of cuts in 2025, as our 2024 and 2025 GDP forecasts are below the Fed. Though the 2025 median dots is now for 75bps of cuts, FOMC members are skewed to the downside and the uncertainty impacts the 2025 and 2026 views more. Finally, Powell guidance that QT will slow fairly soon suggest a decision at the May or June meeting.

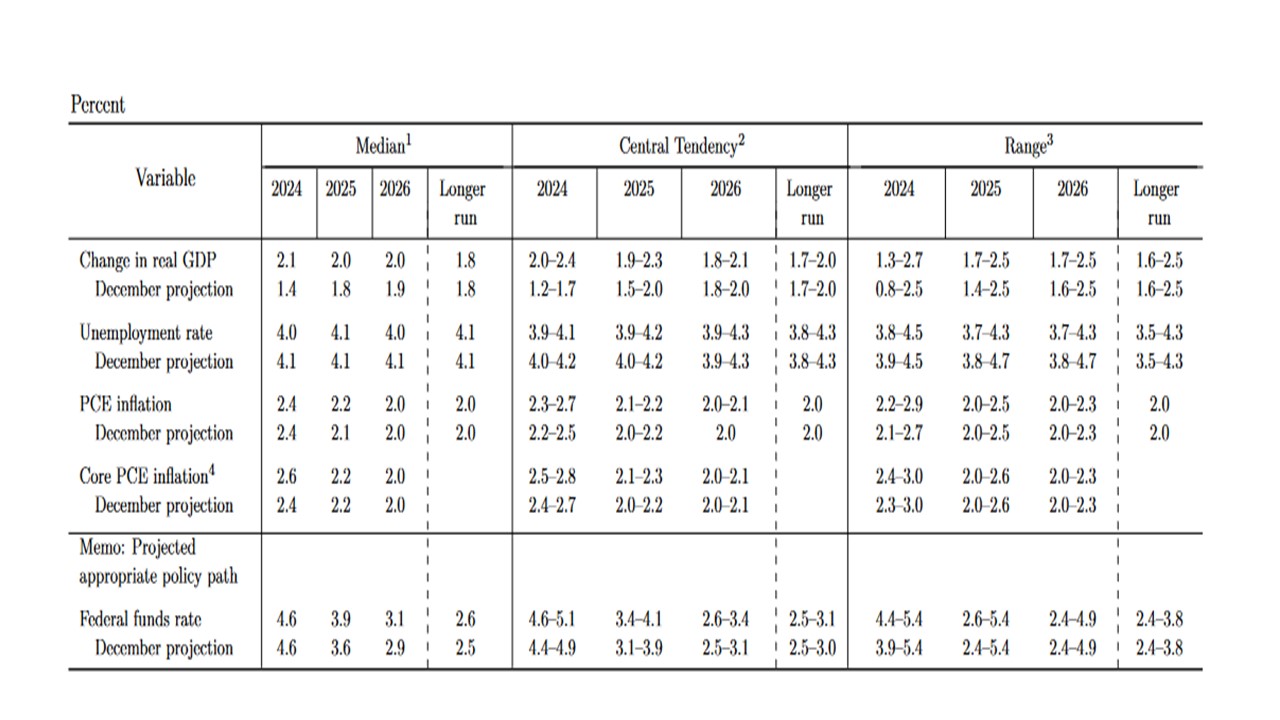

Figure 1: Fed March Summary of Economic Projections (SEP)

Source: Fed (March SEP)

2024 Rate Cuts

The March FOMC statement and Fed Chair Powell Q/A provide a number of clues on prospective policy. Key points include

· Inflation/Growth Revised Up. The median for 2024 GDP has been revised up more than expected to 2.1% (Figure 1), which reflects the resilience of the economy in H2 2023 and Q1. Additionally, the SEP median for core PCE in 2024 was also revised up more than anticipated to 2.6%. During the press conference, Powell left the impression that these change in medians reflect recent data and are not significant – he also hinted at a controlled Feb core PCE number. On the labor market, the Fed Chair once again noted that the labor market is tight but that demand and supply is coming into better balance – with labor supply being helped by higher participation in the 25-54yr age group and more immigrants.

· Guidance on Interest rates. The surprise was that the 2024 median dot was not revised up and remains for 75bps of cuts, though the breakdown shows it was close with only a slim majority at 4.6% or below. 2025 was scaled back from 100bps to 75bps. However, the dots for 2025 and 2026 were skewed to the downside, which shows that uncertainty is the key among Fed officials rather than a definitive rethink that the terminal policy rate will be higher than previously thought. The median for the long-term Fed Funds rate nudged up from 2.5% to 2.6%. The key in the FOMC statement was the continued use of the sentence that “it would not be appropriate to reduce the target range until it gained greater confidence that inflation was moving sustainably towards 2pct”.

· 2024 rate cuts. Powell noted that the January and February CPI and PCE had not materially impacted the assessment that inflation trend is slowing down, while also still anticipating that shelter inflation will be less of an issue in the future. However, Powell was cautious on providing hints for the May and June meetings, though noting that high inflation or weak labor market data could impact the timing of the 1 cut. Powell did not sound hawkish and this could mean that a June rate cut is possible, but our preference is for a 25bps cut in July followed by two 25bps cut in Q4. We have a softer H2 2024 GDP view than the Fed, as the lagged feedthrough of tightening feeds through and the household rundown of savings slows. Meanwhile, we stick with our view of a 100bps of cuts in 2025. Our 2025 GDP view of 2.1% Q4/Q4 is in line with the Fed’s 2.0% but with our 1.4% view for 2024 below the 2.1% seen by the Fed activity would then be at a lower level than seen by the Fed through 2025.

· QT. Powell guided that the committee view was it would be appropriate to slow the pace of QT fairly soon, which suggests that a decision could be made in May or June meeting for implementation the next month. Powell noted on a few occasions that they did not want a repeat of 2019 and with RRP falling quickly this could mean a May decision. However, Powell additionally noted that this did not mean that QT would end earlier, as the Fed were still focused on the scale of reduction rather than a specific timescale. It currently remains unclear how much the Fed will slowdown QT, but it would have to be meaningful without being dramatic. This could suggest USD40bln Treasury maximum rundown versus the current USD60bln cap.