FX Daily Strategy: N America, April 11th

ECB likely to signal June rate cut on the cards

Widening yield spreads suggest EUR/USD can test the year’s low below 1.07

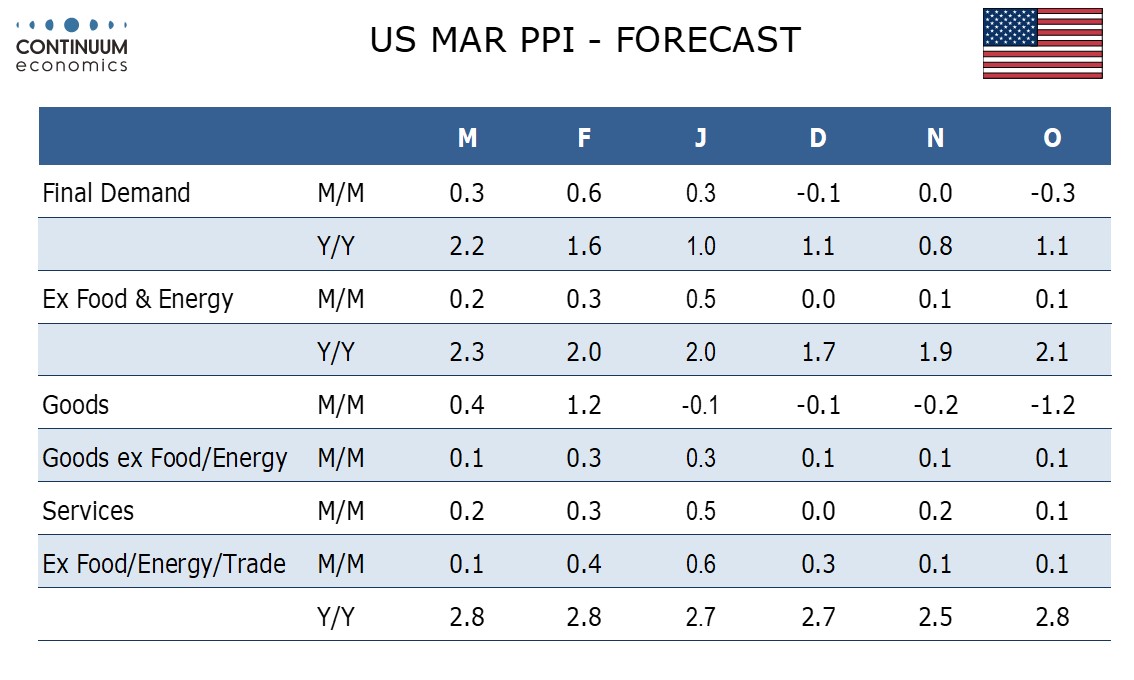

US PPI could impact post-CPI USD strength

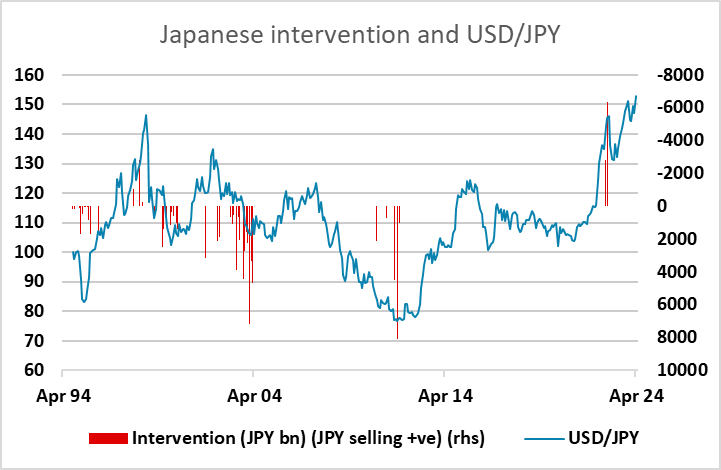

Japanese authorities likely to hold off on intervention as long as USD/JPY gains represent USD strength rather than JPY weakness.

ECB likely to signal June rate cut on the cards

Widening yield spreads suggest EUR/USD can test the year’s low below 1.07

US PPI could impact post-CPI USD strength

Japanese authorities likely to hold off on intervention as long as USD/JPY gains represent USD strength rather than JPY weakness.

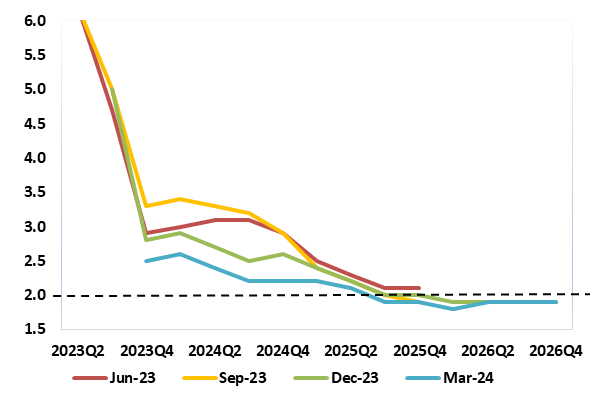

The ECB meeting will be the main focus on Tuesday. As has been the case for the last few meetings, this meeting will be notable not for what the Council does but rather what is said. A fifth successive stable policy decision is very much expected, albeit with some possible formal dissents from a minority in favor of actual cuts. While the ECB is insistent that it is, and will remain, ‘data dependent’ most notably on labor costs data, we expect the path to a rate cut at the June 6 Council meeting will be made clearer. But given existing projections now showing inflation below target by next year, the bar is higher for such data to forestall a 25 bp cut in June and the ECB may underscore a willingness to ease ahead of the Fed. But if the ECB remains focused on such quarterly labor costs updates then subsequent rate cuts may only arrive in September and December, hence our long-standing view that the ECB may cut only some 75 bp this year. However, by year-end more durable evidence of labour costs easing should convince the ECB to continue easing and we see 100 bp further easing through 2025!

ECB sees inflation durably below target

Source: ECB, last four forecast vintages

As it stands, the market is pricing a June rate cut from the ECB as a better than 80% chance. It was even higher than this before the US CPI data sent USD yields higher on Wednesday. EUR yields followed the rise in the US, but the rise was relatively muted, and may well be reversed if the ECB sound dovish. Even now, the widening in spreads in favour of the USD supports further EUR/USD losses to test the year’s lows just below 1.07. The 2 year US/German yield spread is now the highest since December, and with equities also softening the pressure should remain on the EUR downside unless Lagarde surprisingly discourages expectations of a June rate cut.

Otherwise we have the usual set of US Thursday data on jobless claims, as well as US PPI data. US PPI has triggered more market reaction than usual in recent months, sometimes even outdoing the moves on CPI. The 0.3% m/m (0.2% core) rise that is expected might calm the rise in US yields after the CPI data, but it would likely take a flat or negative monthly number to trigger any reversal of the USD gains on Wednesday.

The other focus on Thursday will be on whether there is any reaction from the Japanese authorities to USD/JPY reaching a new 34 year high after the US CPI data, gaining nearly a big figure on the day. The fact that the JPY gained slightly on the crosses is a reason to expect them to keep their powder dry for now. As long as the rise in USD/JPY is clearly a story of USD strength rather than JPY weakness, they will probably judge that intervention has limited chance of success. However, if an initial lack of action leads to renewed JPY weakness, including JPY declines on the crosses, we would expect intervention to ensue. JPY bulls like ourselves should consequently focus on crosses rather than USD/JPY.