FX Weekly Strategy: April 8th-12th

US CPI and ECB meeting may conform to expectations

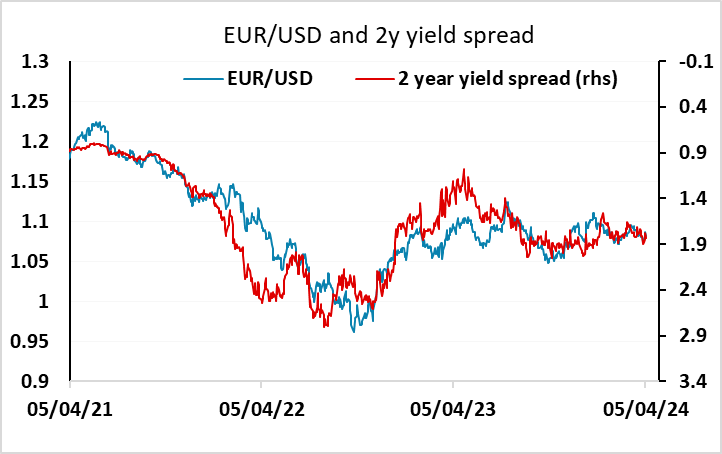

Ranges may therefore remain intact in EUR/USD and USD/JPY

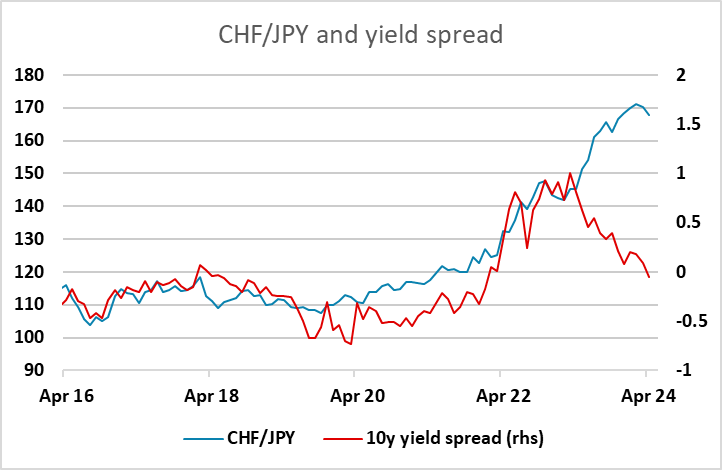

CHF may see renewed weakness if there is no significant risk negative event on the weekend

Strategy for the week ahead

US CPI and ECB meeting may conform to expectations

Ranges may therefore remain intact in EUR/USD and USD/JPY

CHF may see renewed weakness if there is no significant risk negative event on the weekend

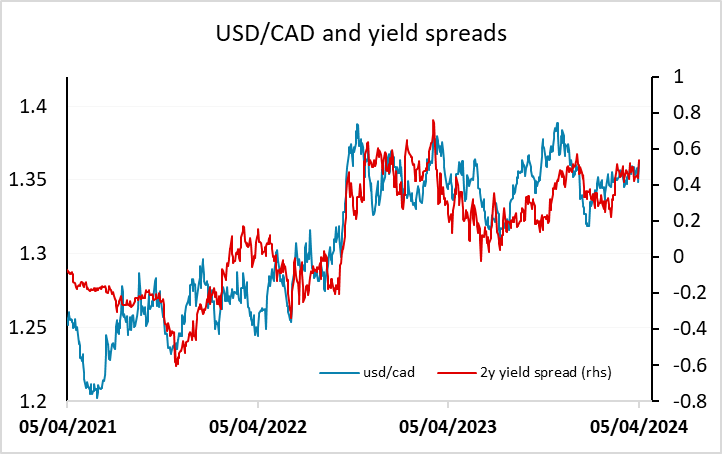

BoC meeting offers mild upside risk for the CAD

The two main events for the coming week are the US CPI data and the ECB meeting. However, on our reading both events may turn out to be damp squibs. We expect the US CPI data to be in line with consensus at 0.3% both headline and core, which should mean that the data doesn’t impact expectations of Fed policy in any meaningful way, and the USD should consequently be largely unaffected.

As for the ECB, they are unlikely to change policy this time around but are expected to set up a rate cut at the June 6 meeting. This is fully priced in, so if they fall short of this with Lagarde suggesting that it would, for instance, require more clear-cut evidence of further weakening of inflation pressures for the ECB to act, the EUR might manage a rally. But we doubt this will be the case.

If these two big events are in line with expectations, markets may be driven by other factors. At the end of last week, we saw some negative risk impact from concerns about the rising possibility of an Iranian attack on Israel. Coming into the weekend, there looks to have been some unwinding of short CHF positioning for fear of weekend developments on this front. If there is no action over the weekend, or action that is not seen to have any longer term big picture impact, we may see a more risk positive tone emerge on Monday morning.

Before these concerns emerged, there had been very much a risk positive tone to the FX market with carry trades being favoured and the CHF, JPY and USD on the back foot. We could see a return to this risk positive tone if the weekend doesn’t provide reasons to turn more negative. We continue to see the CHF as the most appropriate funding currency in current circumstances, taking over from the JPY. The SNB have already started cutting rates, and will be all the more inclined to cut further after the softer than expected Swiss CPI data last week. The CHF is also starting at very high levels. While some of the CHF strength has been justified because of the relatively low Swiss inflation rate in the last few years, so that the CHF is not clearly strong in real terms, this is not true compared to the JPY, where the inflation rate has been similarly low. CHF/JPY has risen dramatically in both real and nominal terms and looks way too high relative to fundamentals. There is also much more tolerance of a weaker currency from the SNB, while the Japanese authorities continue to warn against further significant weakening of the JPY.

This week sees important data from Japan in the form of the labour cash earnings data for February. While this is less significant for BoJ policy than the outcome of wage negotiations for next year, evidence of strength might revive some expectations of earlier BoJ tightening and support the JPY.

There is also the Bank of Canada meeting this week, and while this is not expected to produce a change in policy, it is, like the ECB meeting, expected to set up a rate cut in June, This is currently around 80% priced in, so there may be more upside than downside risk for the CAD as the statement is likely to leave some room for doubt.

Data and events for the week ahead

USA

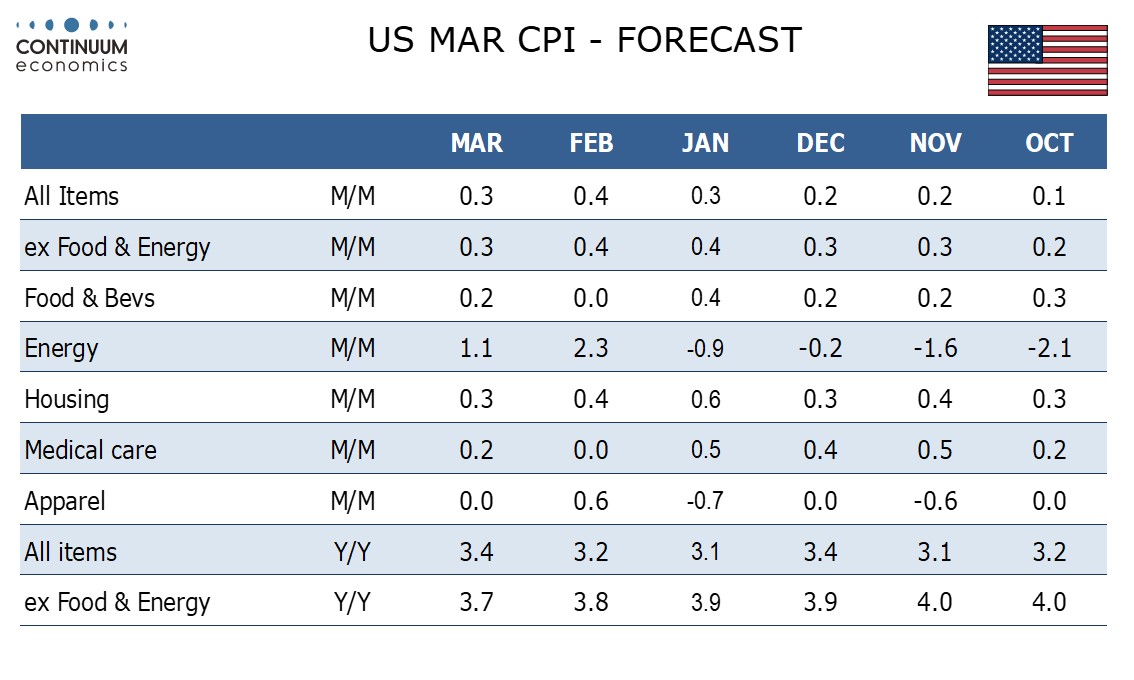

The highlight of the US data calendar is March’s CPI on Tuesday, where we expect gains of 0.3% both overall and ex food and energy. Before rounding we expect the overall pace to be a little stronger than 0.3% but the core rate to be a little below, the latter likely to come as a relief after two straight months which rounded up to 0.4%.

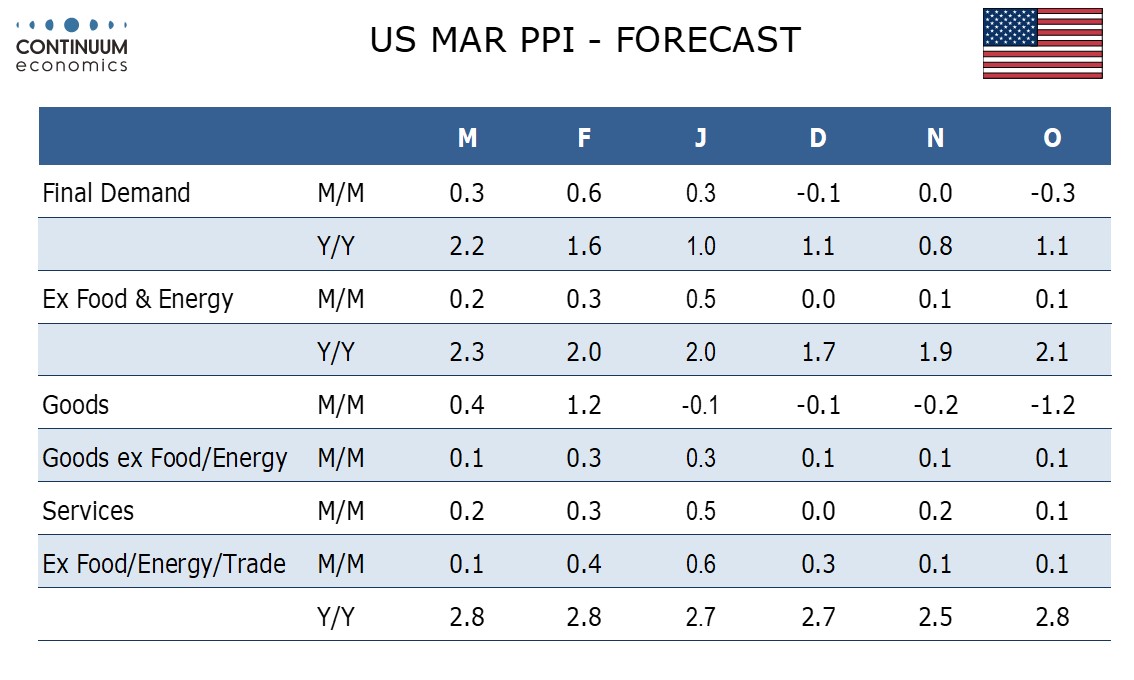

Thursday sees March PPI, and we expect a 0.3% increase overall with a slower 0.2% rise ex food and energy. Some of the week’s minor releases will also give insight on inflation. These include March’s NFIB small business survey on Tuesday, and on Friday March import prices and the preliminary April Michigan CSI. Weekly jobless claims on Thursday will show if the preceding rise was more than a one-week blip.

FOMC minutes from March 20 are due on Wednesday, and we suspect a hawkish tint will be seen, with a significant minority likely to be a little more concerned about recent strong inflationary data than Powell has shown in his recent comments, and agreement that softer inflation data will be needed before easing is seen. The week sees several Fed speakers, including Kashkari on Monday, Goolsbee on Wednesday, Williams and Collins on Thursday and Daly on Friday.

Canada

The Bank of Canada meets on Wednesday and rates look set to remain unchanged at 5.0%, though the BoC will reflect recent upside surprises on GDP and encouraging signs of progress in reducing inflation in its updated forecasts for the accompanying Monetary Policy Report. The statement is unlikely to give much away in terms of forward guidance, leaving the option of easing at forthcoming meetings should progress on inflation continue but making no hints as to when such a move can be expected. February building permits are also due on Wednesday with March existing home sales following on Friday.

UK

Amid low-tier survey data, such as the BRC sales figures Mon) several key update are due. Most notable will be monthly GDP figures (Fri). GDP rose by 0.2% m/m in January more than reversing the 0.1% drop in December data, a result that nevertheless is nothing more than a continuation of the monthly swings seen of late, which may result in fresh drop of 0.1% in these upcoming February data. Thursday sees the BoE Credit Condition Survey, a release that has not shown any appreciable sign of banks being unwilling, let alone unable to lend. A slightly perkier picture of the housing market may come with the latest RICS survey (Thu). There is also a long-awaited review of BoE forecasting techniques and goals with a report authored by ex-Fed Chair Bernanke due on Friday. It is set to offer alternatives to the way the MPC produces and communicates its outlook and has been prompted by recent forecast errors during and since the pandemic. There are also several MPC speeches, perhaps most notable being from recent recruit Sarah Breeden (Mon).

Eurozone

The ECB again takes centre stage. As has been the case for several times now, the ECB meeting verdict due next Thursday will be notable not for what the Council does but rather what is said. A fifth successive stable policy decision is very much expected, albeit with some possible formal dissents from a minority in favor of actual cuts at this juncture. Even without such vocal opposition, the path to a rate cut at the June 6 Council meeting will be made clearer, albeit with the ECB reluctant to pan out any particular path beyond then, insistent it is, and will remain, ‘data dependent’ most notably on labor costs data due in the interim. But the bar is higher for such data to forestall a 25 bp in June and the ECB may underscore a willingness to ease ahead of the Fed and will use updated projections to justify such a move.

A survey if professional forecasters (Fri) may add to the case for easing as may the Bank Lending Survey (Tue) for further insights into the extent to which its policies (conventional and balance sheet) may be meaning that the ECB has presided over both a rise in the cost of credit and a reduction in its effective supply.

Data is short in supply with German industrial production likely to see fresh and perhaps clear m/m falls

Rest of Western Europe

There are key events in Sweden, with the focus on the CPI figures (Fri) which have been volatile of late. We see the key CPIF measures edging up notch from the 2.5% previous reading, this March projection chiming with current Riksbank thinking. Monthly GDP data (Wed) may remain volatile, but with a clear and possible weather-induced correction back in m/m terms.

In Norway, CPI data (Mon) should see a softer CPI-ATE reading, at 4.5%, this being a notch below Norges Bank projections. Monthly GDP data (Thu) may see a clear and possible weather-induced correction back in m/m terms, this being weaker than the flat picture envisaged by the Norges Bank last month.

Japan

Labor cash earning heads the Japanese calendar next week on Monday. While the data would only reflect wage growth in Feb, before the all important wage negotiation, it remains critical to see wage growth sustainably. PPI on Wednesday would be more important to forecast than market as it helps assess the changes in input prices and thus the push in CPI.

Australia

Business condition and confidence on Tuesday and Consumer inflation expectation on Thursday are the only releases for Australia next week. Neither will be market moving.

NZ

RBNZ interest rate decision will be on Wednesday. We forecast there will be no change to the OCR path nor inflation forecast. There is a chance for downward revision for inflation but the magnitude will be small.