FX Daily Strategy: Asia, March 28th

End of month and quarter may dominate ahead of the Easter weekend

GBP and MXN could be vulnerable on positioning, AUD could benefit

JPY and CHF may be favoured if risk is cut back

Data unlikely to have a major impact

End of month and quarter may dominate ahead of the Easter weekend

GBP and MXN could be vulnerable on positioning, AUD could benefit

JPY and CHF may be favoured if risk is cut back

Data unlikely to have a major impact

Thursday is the last day ahead of a long weekend in most of Europe, so is also effectively end of month and end of quarter. With the economic and events calendars fairly sparse, this could mean that FX movements are more determined by these calendar flows than any news.

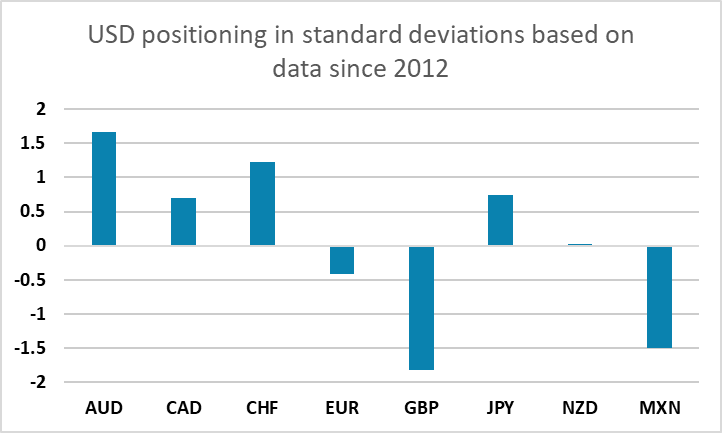

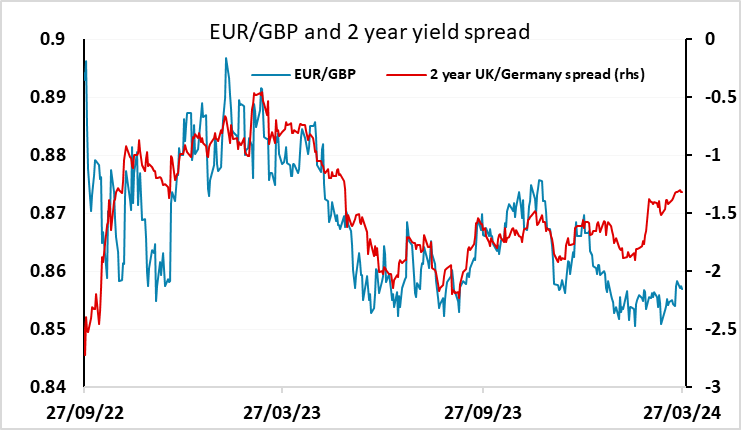

Inasmuch as there is a tendency to close positions at these times, the positioning data could be significant. CFTC data showed that as of last Thursday positioning was particularly long GBP and MXN and particularly short AUD, so there may be some risk of a correction to the GBP and MXN gains against the AUD we have seen in Q1. Revised UK national account data for Q4 is due at the beginning of the European session, and should still imply clear recession in H2 last year while data on the current account released alongside on Thursday may show a fresh deterioration back towards a gap of 4% of GDP. GBP may therefore be at risk, with yield spreads in any case suggesting scope for EUR/GBP gains to 0.86 and beyond.

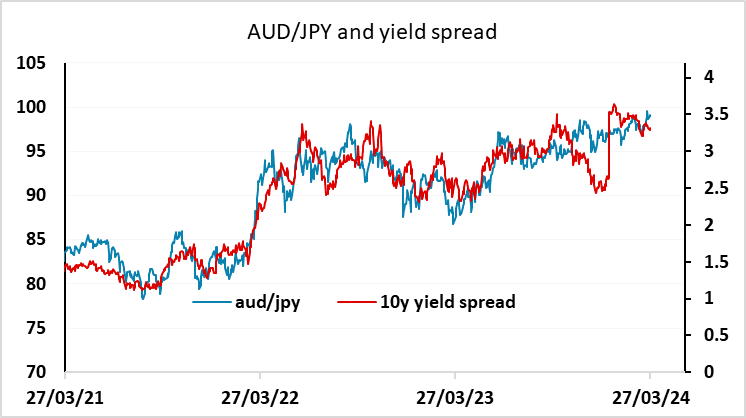

If the AUD is to gain it may require either some strength in the February retail sales data due early in the Asian session, or more likely some general regional strength spurred by a better performance in Chinese equities. Alternatively, JPY strength could also trigger AUD gains. While the JPY has underperformed yield spread moves against most currencies this year, AUD/PY has stuck fairly closely to the normal yield spread correlation, so the tow may move together in the absence of significant changes in yields.

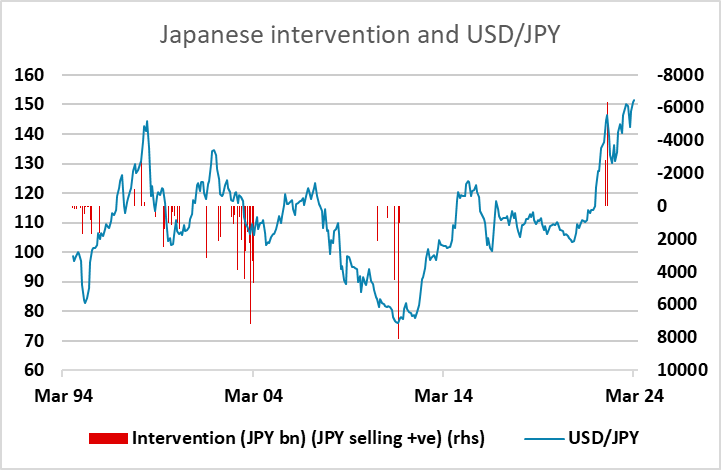

Ahead of a long holiday, there can also be a tendency to favour the safe haven currencies in case of some unexpected event leading to a big risk sell off over the long weekend (unexpected events typically have more potential to have negative than positive impact). The JPY, CHF and USD may therefore have potential to gain on Thursday. The CHF has been particularly weak since the SNB cut rates last week, so there may be some unwinding of short CHF positions into the weekend (CFTC net short CHF positioning also looks relatively extended). It is also likely that speculators will be warier of holding long USD/JPY positions over the weekend, with the Japanese authorities ramping up verbal intervention and USD/JPY still close to the 34 year highs reached on Wednesday morning.

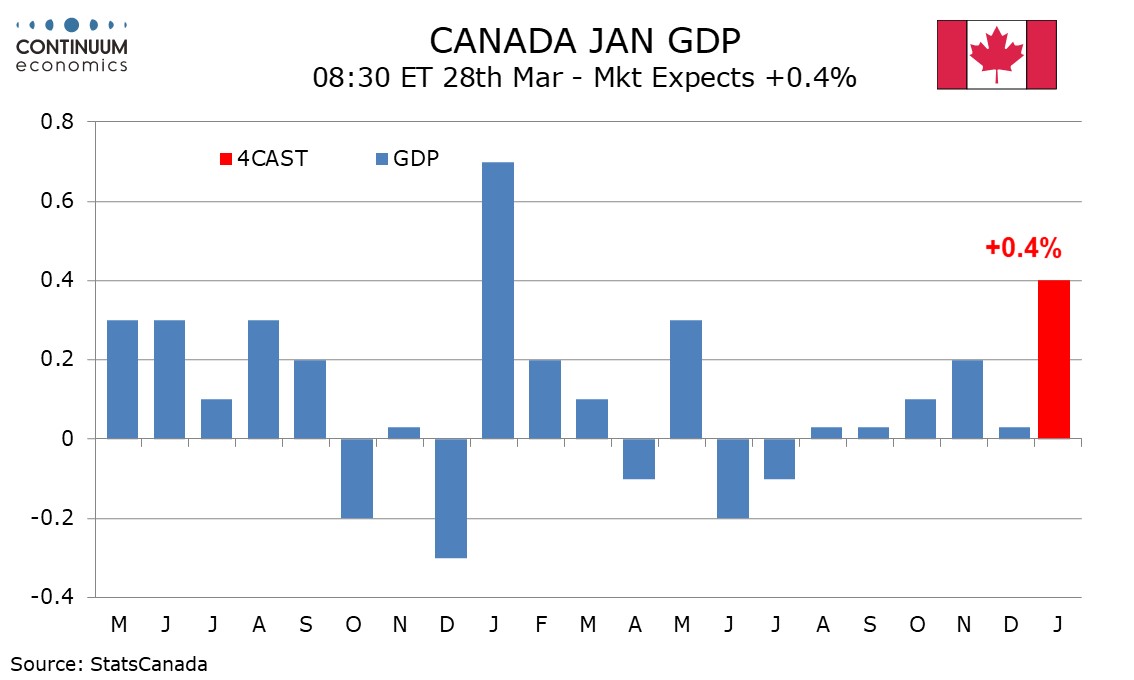

Datawise, there is Eurozone February money data, Canadian January GDP data, final US Q4 GDP data and the usual US jobless claims data, but we don’t anticipate these having a big impact. There may be some interest in the Eurozone money data after fresh weakness in lending was seen in the January numbers, but it is hard to see EUR/USD testing the established range without something more significant on policy. For the Canadian data we expect a 0.4% increase, in line with a preliminary estimate made with December’s data, assisted by the ending of strike activity, and this is also in line with market consensus. We expect a final US Q4 GDP increase of 3.1% versus a 3.2% preliminary.