Outlook Overview

View:

April 03, 2024

March 27, 2024

March 25, 2024

January 11, 2024

Webinar Recording December Outlook: Rate Cuts Into 2024

January 11, 2024 8:22 AM UTC

You can now access the webinar for the December Outlook here.

To read the individual chapters please see the weblink below.

Outlook Overview: Rate Cuts Into 2024 (here)

U.S. Outlook: Slower Growth to Sustain Improved Inflation Picture (here)

LatAm Outlook: Diverging Paths in 2024 (here)

China Outloo

January 08, 2024

Charting our Views December Outlook

January 8, 2024 9:05 AM UTC

Outlook Overview: Rate Cuts Into 2024 (here)

Economic Scenarios

U.S. Outlook: Slower Growth to Sustain Improved Inflation Picture (here)

LatAm Outlook: Diverging Paths in 2024 (here)

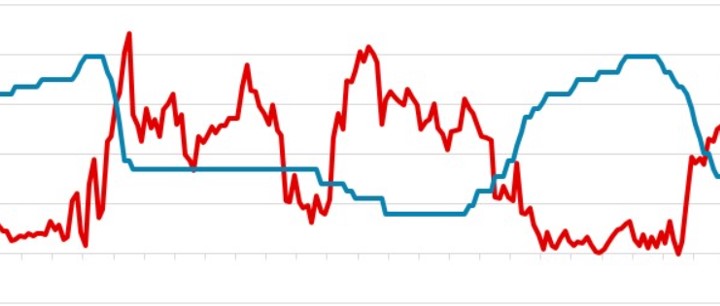

Brazil Policy Rate and CPI Inflation (YoY, %)

China Outlook: Headwinds To China Growth (here)

Japan Outlook: Normalizing

January 02, 2024

December Outlook: Rate Cuts Into 2024

January 2, 2024 9:53 AM UTC

Outlook Overview: Rate Cuts Into 2024 (here)

U.S. Outlook: Slower Growth to Sustain Improved Inflation Picture (here)

LatAm Outlook: Diverging Paths in 2024 (here)

China Outlook: Headwinds To China Growth (here)

Japan Outlook: Normalizing Monetary Policy Soon (here)

Asia/Pacific (ex-China/Japan) Outlook:

December 20, 2023

Outlook Forecasts to download in Excel

December 20, 2023 7:31 AM UTC

We forecast across 23 countries annual and quarterly. Our annual forecasts go out to 2028, while our quarterly forecasts are now updated out to Q4 2025. The forecasts are consistent with the December Global Outlook ‘Rate Cuts Into 2024’ published on 18th December 2023.

The file contains nine sh

December 19, 2023

December 18, 2023

Outlook Overview: Rate Cuts Into 2024

December 18, 2023 3:42 PM UTC

· Uncertainty still prevails around this central view. The impact of lagged monetary tightening could be greater than our estimates and deliver mild recessions in some DM countries. We also feel that the disinflationary process could be stronger and this would help bring inflation back

September 29, 2023

Outlook Forecasts to download in Excel

September 29, 2023 9:32 AM UTC

We forecast across 23 countries annual and quarterly. Our annual forecasts go out to 2027, while our quarterly forecasts are now updated out to Q4 2024. The forecasts are consistent with the September Global Outlook ‘Into 2024’ published on 29th September 2023.

The file contains nine sheets: a

September 28, 2023

Outlook Overview: Into 2024

September 28, 2023 10:04 AM UTC

Risks: DM countries could see stronger lagged effects on the economy from the 2022-23 monetary tightening that could prolong the EZ/UK recession or move the U.S. slowdown towards a mild recession. Separately, in China the impact of the residential construction decline could be stronger than expected

September 19, 2023

August 02, 2023

U.S. and EZ Government Bond Yields and Peaking Rates

August 2, 2023 7:52 AM UTC

Figure 1: 10-2yr U.S. Government Bond Curve (%)

Source: Datastream/Continuum Economics

Rate Hikes Ending But No Early Rate Cuts

Policy tightening is getting to a mature stage in DM economies, with the Fed and ECB now in restrictive territory and the lagged effects of previous tightening yet to fu

June 28, 2023

June 23, 2023

Outlook Forecasts to download in Excel

June 23, 2023 1:57 PM UTC

We forecast across 23 countries annual and quarterly. Our annual forecasts go out to 2027, while our quarterly forecasts are now updated out to Q4 2024. The forecasts are consistent with the Q3 2023 Global Outlook ‘Headline Inflation Slowing, Core Inflation and Policy Rates in Focus’ published o

Outlook Chapters Links

June 23, 2023 12:28 PM UTC

The chapters can be accessed by clicking on the relevant links.

U.S. Outlook: No Recession, but Subdued Growth Will Help to Reduce Inflation (here)

LatAm Outlook: Lower Inflation and Growth above Expectations (here)

China Outlook: Recovery To Fade Into 2024 (here)

Japan Outlook: Trend Inflation To

June 22, 2023

Outlook Overview: Headline Inflation Slowing, Core Inflation and Policy Rates in Focus

June 22, 2023 10:29 AM UTC

•We continue to feel that most central banks are underestimating the strength of tightening on credit/economy and then inflation and the effects of cumulative rate hikes since the start of 2021 (Figure 2). DM central banks are placing too much weight on current core inflation, rather than the

April 11, 2023

Too Much Debt Growth Since 2007: China, Japan and France

April 11, 2023 7:11 AM UTC

With a shift away from the ultra-low interest rate era, some debtors will face difficulties servicing debts. Will this be a headwind to growth and also pose financial stability risks?

Market Implications: In terms of financial stability, China’s ability to control debtors and creditors sugge